How preferred is preferred senior?

Potential revisions to the CMDI framework in the longer term and the CRR amendments effective from 1 January 2025 are generally negative for preferred senior unsecured bonds. However, the bulk of the impact has already been priced in, at least in the short term

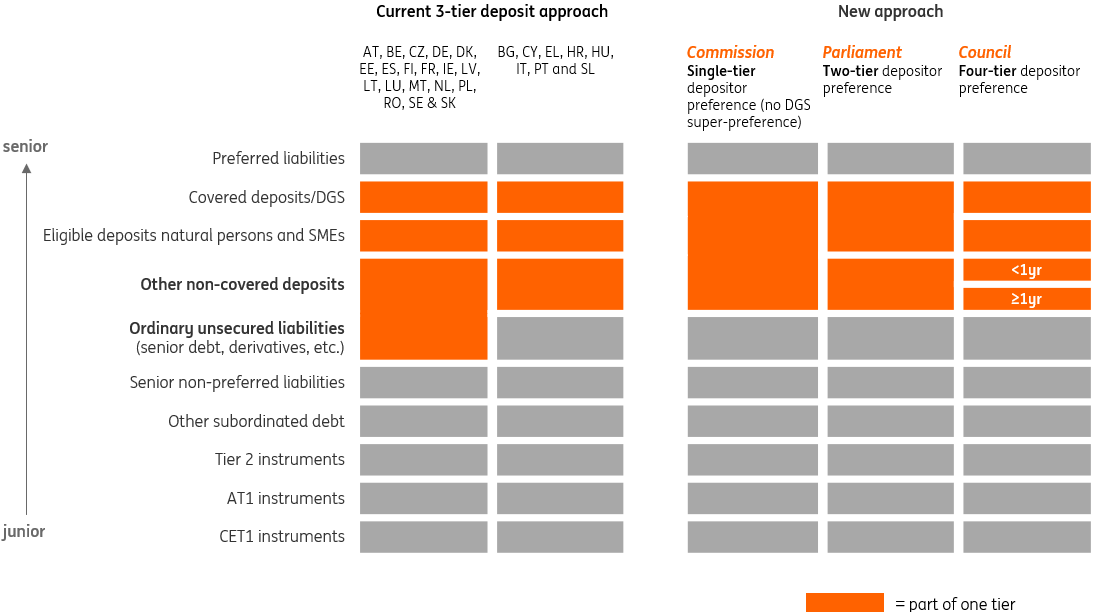

European bank liability hierarchies set to change

The European Bank Crisis Management and Deposit Insurance (CMDI) update might introduce not only minor adjustments to the bank resolution framework but also significant changes to the bank liability hierarchy, which could have major implications for the banking sector, in our view. However, there is still considerable uncertainty regarding the final format and timing of the package.

The European Commission released its proposals to reform the CMDI framework in the EU in April 2023. In April 2024, the European Parliament published its version of the text. Finally, in June 2024, the Council of the European Union presented its proposal for the CMDI framework. Negotiations are ongoing, and no agreement on the final text has been reached yet. Therefore, no changes are expected in the short term, and the package may potentially become applicable closer to 2028 at the earliest, in our opinion.

The changes were motivated by the need to enhance the resolution framework for small and medium-sized banks, as previous solutions were often found outside the existing harmonised resolution framework, relying on government funds rather than private sector or industry-funded safety nets.

The package includes three legislative proposals amending the Bank Recovery and Resolution Directive (2014/59/EU), the Single Resolution Mechanism Regulation (806/2014) and the Deposit Guarantee Schemes Directive (2014/49/EU).

According to the Commission, the focus of the CMDI update is on:

- Preserving financial stability and protecting taxpayer money, by facilitating the use of privately funded deposit guarantee schemes in crisis situations to shield depositors from losses, where necessary, to avoid contagion to other banks and negative spillovers to the economy.

- Shielding the real economy from the impact of bank failures as a resolution that preserves critical functions is thought to be less disruptive for the economy and local communities than liquidation.

- Enhancing depositor protection by extending the deposit guarantee to public entities and certain types of client funds, while maintaining the coverage level at €100,000 per depositor per bank. For temporary higher balances during specific life events, the protection will be more harmonised with a higher limit.

Some of the key focus/debated points in the package include:

- The introduction of a general depositor preference.

- The number of deposit tiers in the liability hierarchy.

- Extending resolution into mid-sized banks by widening the public interest assessment.

- Usage of DGS funds outside payout of covered depositors to finance resolution.

- Access to resolution funding by using DGS funds.

- Existence and consequences of the DGS super-preference.

While the European Commission, the European Parliament, and the Council of the European Union each have their own ideas on structuring, they all share a common overarching view. All three support the notion that all depositors in the EU should benefit from a general depositor preference in the future, ranking ahead of ordinary unsecured claims. Under the current BRRD, the ranking of some depositors is not clearly defined compared to other ordinary unsecured claims, leading to inconsistencies between EU countries.

All three proposals recommend altering the current three-tier deposit ranking system, but they differ in the number of deposit layers suggested: one (Commission), two (Parliament), and four (Council). The most significant difference is the Council’s proposal to create an additional, more junior deposit layer for a four-tiered approach, compared to the Commission’s single-tier approach.

While the approach to bank deposits differs between the three proposals, all share a general depositor preference

The general depositor preference has been suggested to facilitate bank resolution. A risk of breaching the no-creditor-worse-off principle is seen to be more limited when bailing in ordinary senior unsecured claims if all depositors rank with a priority to these claims. As a depositor preference could allow for access to resolution funds without bailing in deposits, this could provide some stability to deposits in times of stress, with a more limited risk of a bank run.

The ranking of deposits is only one part of the debate. Other things under close watch include the broadening of the usage of DGS funds to other uses than the payout of covered depositors. The DGS funds could be used for banks to reach the required 8% bail-in to allow for accessing common resolution funds, like the SRF in the Banking Union, subject to certain conditions.

Widening the uses of DGS would probably extend the number of banks that could access the SRF, but it would also mean that some banks could access it with more limited loss sharing than others. This could arguably harm the level playing field. The wider usage of DGS funds may also come with a heavier cost burden for the sector as a whole, although the impact could be at least partly offset by the possibility of taking action earlier in the bank trouble process.

Implications for bank bond ratings

The introduction of a full depositor preference would have clear negative consequences for bank senior unsecured debtholders in the 19 EU member states in our view. Instead of the ordinary senior unsecured claims ranking alongside (and sharing losses with) the non-covered deposits, in the suggested hierarchy the senior layer would bear losses before all deposits. The change would also likely make bailing in of senior creditors easier in a resolution, assuming the other excluded liabilities are low enough to limit the chance of a legal challenge. The final impact would depend on the final wording of the texts and the following actions from banks. The other eight EU member states already have some kind of a depositor preference in place and the implications of the change would therefore be more limited.

The introduction of an overall depositor preference would have varying implications for bank debt ratings, with a more positive impact on deposit ratings and a more negative impact on senior debt ratings.

Moody’s, for example, has indicated that a full depositor preference could result in a one-notch downgrade for 60% of banks in its sample of 89, while a smaller 6% could face a two-notch downgrade. However, 35% of ratings would remain unaffected by the change. These adjustments are due to a more limited uplift in the assigned loss given default notching.

Indicative share of banks with a potential senior rating downgrade at Moody’s from an application of an overall depositor preference

At some rating agencies, potential downgrades in preferred senior debt ratings may be less widespread and concentrated on a few, mainly small, banks that are not subject to MREL buffer requirements and that do not issue much senior debt of any type. Deposit ratings may see some upgrades for some banks that are using preferred senior in their MREL buffers.

At other rating agencies, the creation of a general depositor preference does not in itself imply rating changes as they reflect the likelihood of default and not loss given default. The depositor preference would be therefore unlikely to affect ratings directly assuming the banks’ ability and willingness to service preferred senior debt would not meaningfully change, although the recovery prospects may decline.

That being said, it is good to note that banks that currently benefit the least from larger subordinated buffers in their senior ratings include banks in countries that have a depositor preference in place, such as Italy, Greece and Portugal. Banks with senior ratings that benefit from larger subordinated debt buffers are instead in countries such as Belgium, Finland, France, Germany, Ireland, the Netherlands, Denmark or Sweden, all systems that do not have a depositor preference currently in place.

All in all, while we think the potential rating changes across the board for preferred senior unsecured debt would largely depend on the final outcome of the framework and on the banks’ reaction to the changes, on balance the impact is likely to be negative.

Reduced risk of a no-creditor-worse-off breach in the event of a preferred senior bail-in could facilitate this debt layer sharing losses during a resolution, potentially affecting the composition of MREL requirements. Banks might respond by decreasing their subordinated MREL buffers and relying more on preferred senior debt. This could lead to slightly less supply pressure on non-preferred senior debt and slightly more on preferred senior debt in the longer term.

The combination of increased supply, along with a potentially higher probability of default and loss given default in some cases, and pressure on debt ratings, could result in wider spreads on the product.

That being said, we consider that most larger banks will continue to support their loss absorption layers with non-preferred senior debt, which would likely continue to support their preferred senior debt ratings.

Deposits would face an even lower risk of a bail-in than before. Overall, a reduced risk of bank runs should be viewed positively for the system. Deposits as a funding option for banks would likely become more attractive due to potentially lower costs compared to preferred senior debt. The most junior deposits, especially for large banks, may benefit the most from these changes, depending on the final wording of the texts. However, junior deposits of smaller banks with limited subordinated buffers could be more at risk under the four-tier approach.

Potential CMDI implementation may take time

Following the proposals, the CMDI process is entering the final stage of negotiations. It seems unlikely that an agreement will be reached this year. Substantial differences and considerable uncertainty about the final outcome suggest that serious talks will likely begin in 2025. Once the final format is agreed upon, Member States will have two years to implement the directive from its entry into force. This implies that the package could become applicable around 2028 at the earliest. There is also a risk that it may take even longer, meaning potential market impacts should not be considered imminent.

Potential impacts from the CMDI on banks

- Smaller risk of deposit burden sharing in most cases.

- Less limited risk of a bank run, a positive for stability.

- Preferred senior to become easier to bail in outside large layers of excluded liabilities.

- Preferred senior to share losses with a thinner layer.

- Potentially some issuance to move from non-preferred to preferred senior debt.

- Deposits to become more attractive in the bank funding mix.

What’s in store for preferred senior under the CRR?

There are also other regulatory changes ahead that may impact preferred senior debt.

After the Banking Reform Package of 2019 introduced a distinct layer of non-preferred senior unsecured bonds to facilitate banks in meeting their bail-in buffer requirements, banks have felt a bit in the dark regarding the risk weight treatment of senior unsecured bonds used to meet banks’ total loss-absorbing capacity (TLAC) and/or their minimum requirements for eligible liabilities (MREL).

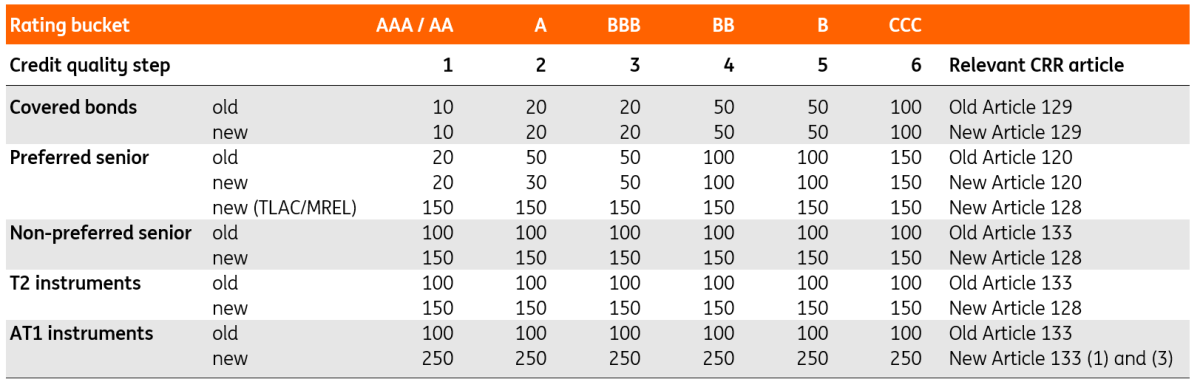

The Capital Requirements Regulation (CRR II) lacked guidance on whether these bonds should be treated as exposures to institutions (CRR Articles 120-121), with risk weights under the standardised approach based on the second-best rating of the bond (varying from 20% [AA] to 150% [CCC]), or as equity exposures (CRR Article 133) subject to a risk weight of in principle 100%.

In 2022, the European Banking Authority (EBA) refused to give an opinion on this for non-preferred senior bonds, arguing that a revision of the legal framework would be required to address the question.

Now CRR III provides that clarity, at least for non-preferred senior unsecured bonds. However, when it comes to the treatment of preferred senior unsecured instruments some questions remain.

Risk weight treatment

The amended CRR gives clearer guidance on the risk weight treatment under the standardised approach for bonds that are used for TLAC/MREL purposes. At the same time, it provides for a more granular and, on balance, more penalising risk weight treatment for bonds further down the creditor hierarchy.

Under the amended CRR Article 128, the following exposures will be treated as subordinated exposures subject to a 150% risk weight treatment.

- Debt exposures, subordinated to the claim of ordinary unsecured creditors (eg non-preferred senior bonds).

- Own funds instruments to the extent that those instruments are not considered to be equity exposure per Article 133(1) (eg T2 subordinated bonds).

- Exposures arising from the institution’s holding of eligible liability instruments that meet the conditions of Article 72b (eg certain preferred senior bonds).

Risk weight treatment bank bond instruments (%)

So, while preferred senior unsecured bonds that are not used for TLAC/MREL purposes may benefit from the slightly more granular rating-based risk weight treatment under the amended CRR Article 120 if they are credit quality step (CQS) 2 rated, preferred senior unsecured bonds that are used as eligible liabilities are classified in the same 150% risk weight bucket as non-preferred senior and T2 bonds. That is if they meet the CRR Article 72b conditions for eligible liability instruments, which were already introduced in CRR II for TLAC.

Now, here is the thing. CRR Article 72b(2) point (d) requires that the claim on the principal amount of eligible liabilities is entirely subordinated to claims arising from liabilities that are excluded from the eligible liabilities, such as covered deposits, covered bonds or liabilities related to derivatives. In the case of preferred senior unsecured bonds, this requirement is often not met as the bonds rank in most countries pari passu to, for instance, liabilities arising from derivatives.

For that reason, CRR Article 72b(3) allows the resolution authority to permit additional liabilities (eg preferred senior unsecured bonds) to qualify as eligible liabilities instruments up to 3.5% of the total risk exposure amount for TLAC purposes, provided that all the other conditions of Article 72b(2), except for point (d), are met.

The other conditions prohibit, for instance, the inclusion of any incentives to call or redeem the notes before maturity, or to amend the level of interest or dividend payments based on the credit standing of the resolution entity or its parent. Instruments issued after 28 June 2021 (CRR II application date) should also explicitly refer to the possible exercise of write-down and conversion in the contractual documentation.

These additional liabilities must, in principle, rank pari passu with the lowest ranking excluded liabilities, and their inclusion should not give rise to a material risk of no-creditor-worse-off challenges or claims, where a creditor can validly argue to be worse off in resolution than in normal insolvency proceedings.

Even when a bank is not permitted to include Article 72b(3) items, resolution authorities can still agree to the use of additional eligible liability instruments under CRR Article 72b(4). These liabilities should also meet all conditions of 72b(2) except for point (d), and the aforementioned requirements on pari passu ranking with excluded liabilities and no-creditor-worse-off risks. On top of that, the amount of the excluded liabilities that rank pari-passu or below those liabilities in insolvency, should not exceed 5% of the own funds and eligible liabilities.

Article 45b of the Bank Recovery and Resolution Directive (BRRD) also refers to CRR Article 72b, except for point (2)(d), as part of the conditions for inclusion of a liability in MREL. While MREL is not subject to the subordination requirement of CRR Article 72b(2)(d), it is in principle subject to a subordination requirement of 8% of total liabilities and own funds that is set by the resolution authorities.

Not all preferred senior unsecured bonds are marketed for MREL purposes

European banks make abundant use of preferred senior bonds for MREL purposes. The graphic below shows, for a sample of 35 EU banks, that many of these credit institutions do not fully meet their MREL requirements with subordinated liabilities, such as capital instruments and senior non-preferred bonds. Most of them partially use preferred senior unsecured instruments to meet their MREL requirements.

Many banks use preferred senior bonds to meet their MREL

When it comes to the risk weight treatment of these instruments, the first uncertainty arises in the interpretation of the new Article 128(1)(c). Does the 150% risk weight apply to preferred senior bonds issued for MREL purposes, or only to preferred senior bonds issued for TLAC purposes? In other words, are senior bonds used for TLAC always subject to a 150% risk weight regardless of their preferred or non-preferred status, while in the case of MREL, only non-preferred senior bonds that are in the subordinated buffers have a 150% risk weight?

The practice among European banks regarding the use of preferred senior unsecured instruments for MREL purposes and their communication on it is also quite diverse. This leaves banks holding these preferred senior unsecured notes with even more questions than answers on what risk weights to assign, if the 150% would indeed apply to preferred senior notes used for MREL.

For example, some banks make a clear distinction in their prospectus and term sheets between the issuance of senior preferred notes used for ordinary funding purposes and senior preferred notes used for MREL purposes. Both types rank exactly at the same level in the creditor hierarchy. Hence, the no-creditor-worse-off principle would render it impossible to solely apply the bail-in tool to the bonds that are explicitly marketed for MREL purposes, while leaving the other senior preferred bonds untouched. This also applies to preferred senior unsecured bonds issued before banks began officially stating in the prospectus or final terms that the bonds would be used for MREL purposes.

So what risk weights should be assigned to these bonds? 150% if the bonds are distinctly marketed to the MREL requirements, and a risk weight based upon their ratings if they are not marketed as such? Or should in both cases a weighted approach apply: only 150% for the share of use for MREL purposes and a rating-based risk weight for the rest of the bond’s notional amount?

There are also cases where preferred senior unsecured bonds can in principle be used for MREL purposes, but the institution has stated that, at this point in time, it has no intention of using the preferred senior unsecured bonds for MREL purposes. The MREL requirements of these banks are fully met with subordinated liabilities. However, the preferred senior notes are often still part of the total MREL buffer, for instance to have sufficient cushion against any potential maximum distributable amount (M-MDA) constraints on dividend payments or share buybacks.

What does this mean for the risk weight treatment of the bonds? Can these bonds be risk-weighted based on the instrument ratings, or should they be risk-weighted 150% as, in the end, they are still part of the total MREL stack of the bank? The most logical take on this is that the 150% risk weight should indeed solely apply to that part of the bonds that are used to meet the MREL requirements.

Limited performance implications from a risk weight angle

The performance implications of the CRR III risk weight treatment of preferred senior unsecured bonds should probably not be that massive anyway. Banks are typically not the largest investors in the preferred senior unsecured bonds of other banks. Primary distribution statistics show that banks purchase only 24% on average of the preferred senior unsecured notes issued in the primary market. This is much lower than the 48% bought by banks in newly issued, and more favourably risk-weighted, covered bonds.

Distribution of bank bond deals to other bank investors

For bonds issued in 2023 and 2024 YTD

Unlike covered bonds, preferred senior unsecured bonds are also not eligible as high-quality liquid assets for Liquidity Coverage Ratio (LCR) purposes. Preferred senior unsecured bonds issued by eurozone banks are eligible for ECB collateral purposes though up to 2.5%. This explains why they are still more often bought by banks than bail-in senior unsecured or T2 debt instruments.

The use for MREL purposes is relevant for preferred senior spreads

Regardless of the risk weight treatment of preferred senior unsecured bonds, the expected losses, as assessed by investors or reflected in bond ratings, will remain the primary driver of these bonds’ performance and their relative trading levels. The graphic below illustrates this for the non-preferred and preferred senior unsecured bonds outstanding in the 2027 maturity bucket for the banks in our sample with both instruments outstanding in this tenor. Banks that do not use preferred senior unsecured bonds to meet their MREL requirements have tighter preferred senior unsecured spread levels at given non-preferred senior unsecured spread levels. Or to put it another way: they have wider non-preferred senior unsecured spreads at given preferred senior unsecured spreads.

Banks that use preferred senior for MREL tend to have wider non-preferred vs. preferred senior spreads

The higher the share of the preferred senior unsecured layer that is used to meet the MREL requirements, the more negligible the spread differential between the non-preferred senior and the preferred senior unsecured bonds becomes.

The higher the share of preferred senior used, the closer spreads are to non-preferred

Any implications are already broadly priced in

Market participants have arguably had ample time to prepare for the upcoming CRR revisions, with the CRR III proposals published in 2021. Indeed, the spread differential between non-preferred and preferred senior bonds has become smaller in the past few years, with the difference quite tight at 20bp considering where absolute spread levels are.

We believe, however, that the proposed revisions to the CMDI have had a stronger impact here than the changes to the CRR. For the very simple reason that these ultimately affect a much broader investor base.

Spreads between non-preferred and preferred senior bonds have become tighter

Over the past year, the spread difference between senior non-preferred and preferred senior bonds has remained tight, despite the net supply dynamics being more favorable for preferred senior unsecured bonds compared to non-preferred senior unsecured instruments.

This trend is likely to continue in 2025, with an increase in fixed coupon preferred senior redemptions and a decline in fixed coupon non-preferred senior unsecured redemptions. However, we also expect a slight increase in preferred senior supply next year, while non-preferred senior supply is anticipated to be lower in 2025.

Fixed coupon senior supply and redemptions

Should we worry about the regulatory impact on preferred senior spreads in 2025?

At current spread levels, we don’t expect preferred senior bonds to become cheaper in 2025 versus non-preferred senior unsecured bonds. While we do acknowledge that the CRR revisions are negative for preferred senior instruments from a risk weight perspective, we think that spread levels are already broadly pricing in these risks for now.

In addition, there remains some uncertainty regarding the final shape and form of the CMDI package. The final implementation, once – and if – a compromise is reached, is likely to still take several years. The directive would need to be transposed into national law first. The potential negative implications, such as from a bail-in risk perspective and also from a ratings perspective, therefore may also take some time to reflect in more earnest on preferred senior unsecured bond spreads.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

BanksDownload

Download article

13 November 2024

Bank Outlook 2025: Clearing the fog – bank risks and market shifts This bundle contains 6 Articles