Bank of England: Two data points that will make or break a March rate hike

In their hunt for signs of 'inflation persistence', policymakers will be paying particular attention to the service sector. They will also want to see further changes in wage and price-setting behaviour in the Bank's own survey of businesses. One final 25 basis point rate hike in March still looks likely

'Inflation persistence' - what does it actually mean?

The Bank of England might be done with rate hikes – or at least that was one possible interpretation of the abrupt change in the Bank’s forward guidance last week. Officials said they would now closely monitor indicators of inflation “persistence” to judge whether further tightening is needed. Our own view is that the Bank has one more 25bp hike to come in March.

The choice of the word 'persistence' is interesting. It implies policymakers aren’t going to be as beholden to month-to-month swings in headline, or perhaps even overall core, inflation. Instead, the Bank is trying to isolate trends in prices – or price-setting behaviour – that will still be relevant for inflation over a two- or three-year horizon.

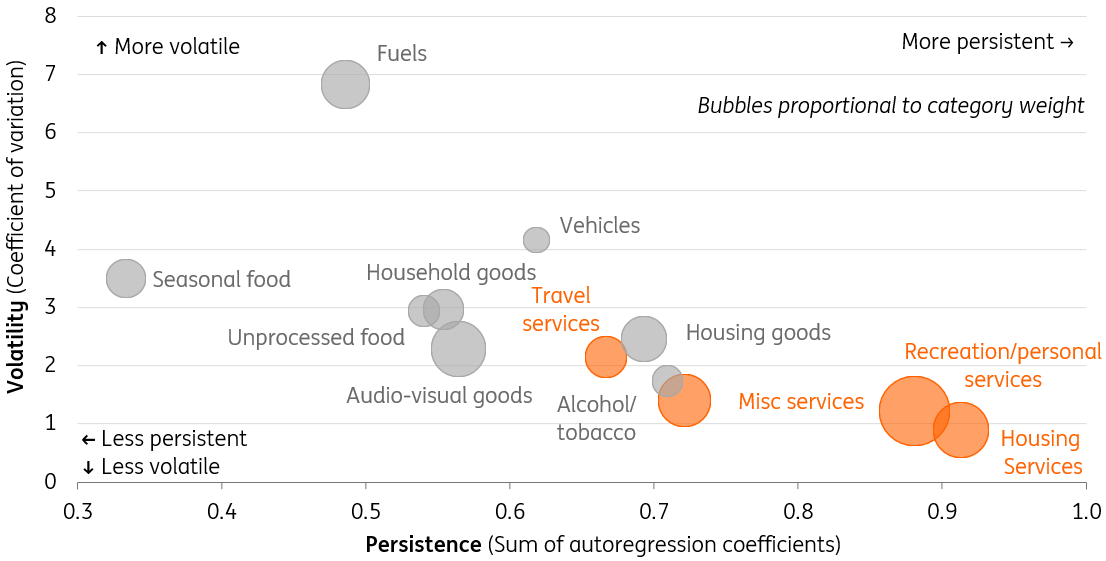

Our analysis shown in the chart below shows that, unsurprisingly, it is the service-sector components of the inflation basket which are typically less volatile and tend to experience more persistent trends. It's these price categories that policymakers are going to be most focused on. And if we strip out the main exception to that rule, ‘travel services’ (which fluctuate because of airfares), then we end up with a measure of ‘core services’ – something we know the Bank of England closely watches.

Service-sector inflation is less volatile and more persistent than goods categories

Indeed, the fact that core services inflation outpaced the Bank of England’s November forecasts – and indeed is showing little sign of peaking – was probably a major factor in the decision to hike rates by another 50bp this month, rather than following the Federal Reserve into a more modest 25bp move. The Bank's most recent forecasts see core services inflation climbing from 6.5% to 7%, where it’s expected to linger for some time.

Core services inflation has continued to edge higher

Bank's own Decision Maker Panel will be a key dataset to watch

We’ll have a couple more inflation readings before the Bank’s March meeting, and any further upside surprises in core services would almost certainly unlock another 25bp rate hike in March (even if the choice of language at last week’s meeting suggests the bar is high for another 50bp move). But ultimately, this is a backward-looking measure – or at least, it doesn’t tell us a great deal about the likely trajectory over coming months.

For that, the Bank will be closely monitoring its Decision Maker Panel, a survey of businesses - something we know policymakers appear to place a lot of weight on, much more so than investors perhaps realise. We’ll get the next instalment on 2 March.

This is arguably a more forward-looking gauge of pricing behaviour, and at the margin, the most recent data contains hints that the inflation story may be turning. Expected rates of wage growth and three-year-ahead inflation expectations both came down in January, while the proportion of firms experiencing “much harder” recruitment conditions has also tumbled over recent months.

The proportion of firms saying it's 'much harder' to recruit has been falling

We think these are trends that are likely to continue. Admittedly, the structural issues in the jobs market – worker illness and lower inward EU migration through Covid – are unlikely to reverse imminently, and that suggests employee availability will remain an issue, even as hiring demand cools. Wage growth, though probably at a peak, is unlikely to cool rapidly.

But wages aren’t the only driver of core inflation, and in fact, energy prices are a more commonly cited factor than labour costs as a reason for raising prices in the service sector, according to successive ONS business insight surveys. That suggests the recent collapse in wholesale gas prices should alleviate a key source of pressure on firms and their pricing decisions. The caveat is that some corporates will have locked into electricity/gas hedges at elevated levels, though an ONS survey from the autumn suggested firms with expiring energy fixes before April 2023 were in the minority.

The lesson here is that we shouldn’t ignore the impact of falling gas prices on the outlook for medium-term service-sector inflation, even if ordinarily we’d strip out the impact of electricity/gas along with petrol prices when looking at core CPI. Together with the widely-anticipated fall in goods-price inflation, overall core inflation should ease gradually as the year wears on.

Energy prices are a common factor in service-sector decisions to raise prices

Data points to one final 25bp rate hike in March

What does this mean for the near-term policy outlook? The Bank will want to see more evidence that the trends in pricing behaviour are persisting, and in reality, it’s unlikely to have enough concrete information by the time of the March meeting. Policymakers are clear that the burden of proof is on inflation showing signs of easing, not the other way around.

That suggests we should still expect a 25bp rate hike next month, though we think the Bank will become more relaxed about inflation by the time of the May meeting. However assuming the downtrend in core services inflation is a gradual one, we suspect a rate cut will be less forthcoming in the UK than in the US, where we think policy easing will arrive by year-end. We don’t expect the first BoE rate cut for at least a year.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article