Bank of England: Six answers on negative interest rates

- 16 October 2020

- FX Rates United Kingdom

It's not currently our base case but negative rates are possible in the UK next year if Brexit goes badly or if Covid-19 gets worse. This would take out the 0% floor on 10-year gilt yields. For sterling, what matters more is the reason behind rates cuts, such as a no-deal Brexit, rather than the rate cut itself

The case of more stimulus is building

With three weeks to go until the Bank of England’s November meeting, there can be little doubt that the case for additional stimulus is building.

The resurgence of Covid-19 across the UK and the resulting restrictions mean the recovery is set to stall. But is all of this enough to move the needle closer to negative rates, and if it does, what would be the impact?

How likely are negative rates in November?

In short, not very.

While the Bank of England has made it crystal clear now that negative rates are ‘in the toolkit’, they’ve opted to take time collecting and analysing data from banks on the potential impact. This operational planning phase is unlikely to be complete before the November meeting when the Bank will publish its next Monetary Policy Report.

We wouldn’t totally rule out a move to zero interest rates (10bp cut) - although this is perhaps unlikely before the review is concluded. We also might see the BoE adjust the interest rate on the Term Funding Scheme, the programme that offers banks cheap funding if they increase lending to SMEs.

But clearly, the major focus will be on QE, and it now looks fairly inevitable that the MPC will top-up its asset purchase programme, perhaps by another £100bn. We think that would give policymakers scope to continue making purchases until early summer next year if the pace of purchases stays broadly similar.

How likely are negative rates in 2021?

Our base case is that the Bank will veer away from lowering rates further, although that relies on there being a Brexit trade deal, and the outlook for Covid-19 looking a little brighter from the spring - neither of which is guaranteed.

But even if the economic outlook does deteriorate further, the Bank will need to be convinced that negative rates will make a difference. And interestingly, recent MPC commentary suggests there’s far from a consensus on how useful the policy would be.

In our opinion, there is so only so much lower interest rates can achieve in the current environment. Instead, the best monetary policy can do at the moment is to facilitate the conditions necessary for fiscal policy to do the heavy lifting.

That said, negative rates could gift the BoE with a greater ability to shape markets via forward guidance in future crises. So far, the Bank has successfully managed to talk market rates below the zero lower bound without so far having to implement the policy. But to achieve a similar result in the future policymakers may find they need to have made the jump below negative for a period of time if markets are to act as an ‘automatic stabiliser’ (that is to price in sub-zero rates) in future times of market stress.

If the BoE were to implement negative rates in 2021, then we suspect it would be reluctant to go significantly below zero (perhaps 20-30bp). We also imagine the MPC would be keen to exit the policy fairly quickly, even if economic circumstances don’t necessarily justify meaningful tightening. This would be similar to what Sweden's Riksbank did at the end of 2019.

What would negative rates mean for the GBP curve?

Negative rates would not come as a great surprise to GBP rates. Indeed 1Y forward 1Y OIS has been below 0% since June of this year, showing persistent negative rate expectations.

This implies that various corners of rates (and probably other) markets already reflect negative rates. This also reduces the potential impact of the announcement. This being said, Sonia forwards are currently consistent with a Bank rate cut to -0.15% (from 0.1% currently). If and when the BOE decides to cut rates, we find it probable that Sonia forward would drop another 10bp, consistent with a trough in the Bank rate of -0.25%.

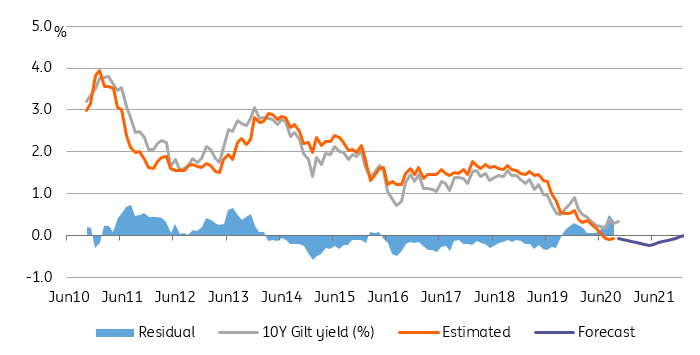

A combination of more QE and negative rates would push gilt yields below zero

What about gilt yields?

A combination of £100bn more QE (our expectation for November) combined with negative rates bottoming at -0.25% would push our 10Y gilt fair value below 0%. We expect any drop in the Bank rate would be reflected roughly equally into repo rates; that would remove the current floor under gilt yields. In addition, further removal of government debt from the market through QE would push yields closer to the repo rate. As a result, we see a trough around -0.20% for 10Y gilt fair value around the middle of next year.

There are wide confidence bands around this central tendency, however. Firstly, you've got to acknowledge that if the Bank rate reaches -0.25%, the BOE would have a hard time convincing markets that rates are at their lower bound, taking the ECB and SNB policy rates of -0.50% and -0.75% as examples. This would suggest 10Y gilt dropping temporarily below the bank rate in anticipation of more cuts. This however would depend on the pace of the recovery in 2021.

At the other end of the risk spectrum, a combination of robust recovery and credible inflation-boosting credentials could result in a materially steeper curve if the BOE implements a negative interest rate policy (NIRP). This would see gilt yields recover quickly and rise above zero faster than our fair value estimate suggests.

Are we likely to see tiering to support bank profitability?

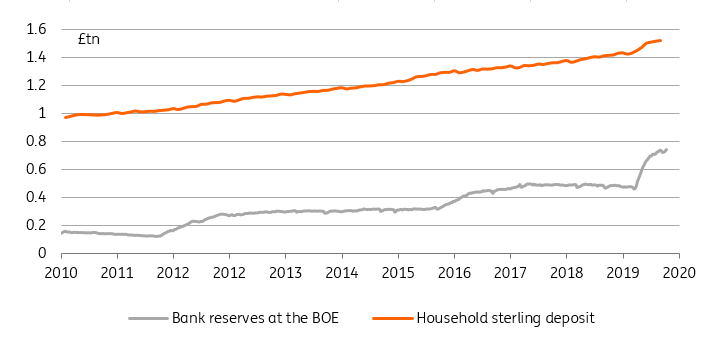

The August Monetary Policy Report noted tiering as a key measure taken by the ECB and other central banks to mitigate the detrimental impact NIRP would have on bank margins. To keep a long story short, the difficulty in charging negative rates to retail deposits while lending rates drop could put pressure on their profitability. To remedy this, the ECB and other central bank exempt a portion (a tier) of bank reserves from negative interest rates.

The ramification of tiering are manyfold. Starting with the impact for banks, we find it unlikely that exempting even a large portion of bank reserves (and don’t forget that the larger the exemption, the less potent the rate cut, see below) would fail to completely offset the drop in profitability for banks at the aggregate level. It is easy to see why: household sterling deposits amount to £1.5tn whilst bank reserves at the BOE are ‘only’ £0.75tn.

Reserves tiering is only a partial offset for the cost of negative rates

The impact on short-dated interest rates markets is not straightforward either. The experience of other jurisdictions suggests that a cut in the Bank rate accompanied by a tiered reserve system would be translated almost entirely to Sonia swap rates. However, the larger the reserve exemption, the less sensitive we expect Sonia would become to a fall in the BOE Bank rate. Similarly, a more generous tiering regime could also affect demand for safe short-dated bonds, such as gilts.

So what we have here is just an overview of the ramifications of negatives rates and a tiering system but it should help demonstrate that the policy amounts to mixed messages for financial markets. On the one hand tiering can be seen as allowing the BOE to cut rates even deeper below zero by easing the pressure on banks. This would allow Sonia forwards to drop significantly below spot as they have done since June. On the other, it may be understood as less of an easing step if not all GBP rates reflect the drop in the Bank rate. This would be for example the case of bond yields not dropping as far as swap rates.

What would be the impact on sterling?

While BoE negative rates would be, unsurprisingly, negative for GBP, what will matter more are the circumstances under which they come about. As we've already mentioned, a 'no deal' Brexit could be a trigger for negative rates. But in this scenario, we'd expect the Brexit factor to be more negative for GBP than the direct effect of negative rates.

Negative rates a negative for GBP, but…

Negative rates are already being partly priced in by the market, meaning that such BoE action would not come as a complete surprise. In addition, there are question marks about how low the BoE would go and to what extent the level of tiering (see above) would reduce the impact of rates cuts on the GBP swap market, and thus on sterling.

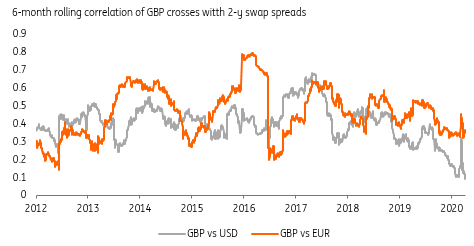

As EUR/GBP is more sensitive to interest rate differentials than GBP/USD (in the chart below, note the GBP/USD sensitivity is at multi-year low), all things being equal, BoE rate cuts would be more detrimental for GBP vs EUR than vs USD. Our EUR/GBP financial fair value model suggests that an unexpected BoE rate cut (ie, a rate cut which is not priced in, with its effect not being reduced by tiering) of 25bp would push EUR/GBP higher by around 1.5%-2.0%.

GBP/USD more sensitive to interest rate differential than EUR/GBP

The trigger behind rate cuts matters more for the currency

Under a 'no deal' Brexit, the subsequent confidence shock, the de-rating of the medium-term UK growth and trade outlooks, as well as question marks about future UK productivity growth, would all weigh on the medium-to-long term sterling fair values and lead to a sharply lower GBP.

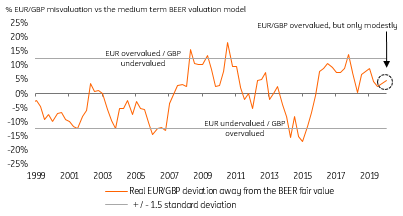

As you can see in the chart below, EUR/GBP does not trade meaningfully above its medium-term BEER fair value, suggesting further scope for a decline

We expect EUR/GBP to test the parity in the case of no-deal Brexit, which would represent a depreciation in excess of 10% versus current levels. Clearly, that would far outweigh the impact of an unexpected 25bp rate cut, which as we said earlier we think would see a1.5-2.0% GBP fall vs EUR.

In other words, the negative rate effect would be of secondary importance for GBP than the shock of Brexit

GBP does not look stretched vs EUR

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

US hero, rates moving to zero

- This bundle contains 6 Articles