Bank of England preview: Better inflation news allows for a smaller 25bp rate hike

August’s meeting is another close call, but a surprise fall in services inflation should allow the Bank to revert to a slower pace of hikes after June’s 50bp move

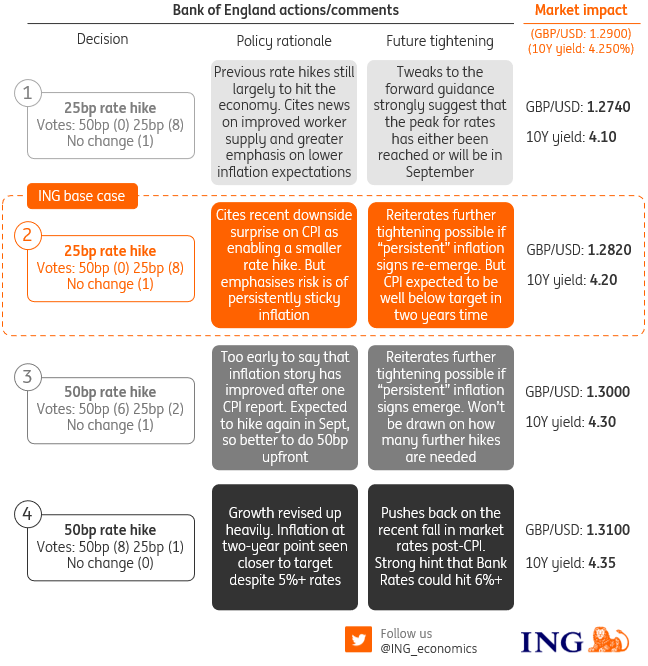

A 25bp hike looks likely in August

Welcome news on UK inflation has taken a fair amount of pressure off the Bank of England to repeat the 50 basis point rate hike it implemented in June. Services inflation, a key metric for the Bank, dipped back in June’s data, against BoE expectations for it to remain unchanged. That was complimented by better news in other areas, including food. Admittedly this improved story on inflation was tempered by a recent upside surprise to pay growth, but that too was offset by further signs of cooling in the jobs market and an ongoing return of workers. This latter point was acknowledged in a recent press conference by BoE Governor Andrew Bailey.

In short, there’s just enough in the latest data flow for the Bank to be comfortable reverting back to a 25bp hike in August. While you could reasonably argue that the latest inflation number is just one data point, you could have made a similar argument about the previous month’s data, which the Bank said had contained “significant news”. We shouldn’t rule out a 50bp hike though, especially if the committee concludes they think they’ll hike again in September. At the ECB’s recent Sintra conference, Bailey explained that this logic partly drove the Bank to enforce a 50bp hike last month.

Beyond the hike itself, there are three other things to watch:

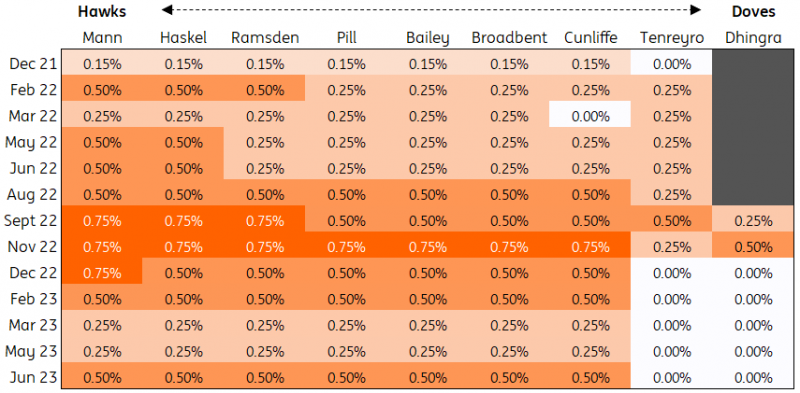

Vote split

Firstly, the vote split. So far this year it has always been 7-2 in favour of raising rates, and on each occasion it has been two of the three external members (Swati Dhingra and Silvana Tenreyro) who dissented, opting instead for no change. The latter of those two doves has now left the committee, replaced by Megan Greene. Early indications suggest she’ll be more hawkish than her predecessor, and the base case is that she’ll vote with the crowd at this meeting.

But we wouldn’t rule out a three-way vote split, whereby Dhingra votes for no change, the majority vote for a 25bp hike, but a couple of members vote for another 50bp move. Given the external Monetary Policy Committee members tend to sit more at the extremes of the hawk-dove spectrum on the committee (including Catherine Mann, who is probably the most hawkish member), it’ll be interesting to see where Greene slots in if we were to get a three-way divide.

The vote split has always been 7-2 so far this year

Forward guidance on interest rates

The second thing to watch is, as always, what the Bank has to say on the future path of rates – but don't hold your breath. With the exception of November last year during the fallout from the "mini-budget" crisis, the BoE has largely strayed away from offering explicit hints on future policy. Expect the Bank to simply reiterate that future hikes are likely if “persistent” inflation signs emerge.

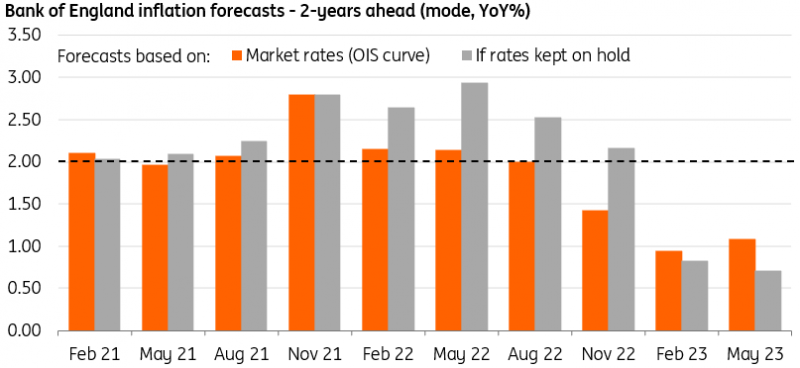

The new forecasts are also unlikely to be a reliable guide. For several months now, the Bank’s models have forecasted headline inflation below target in two years’ time. Both February and May’s modal forecasts saw inflation at roughly 1% over that time period, based on market predictions for interest rates. And since then interest rate expectations among investors have gone up further. You’d imagine August’s inflation projections will therefore show something similar, but it's clear policymakers are not putting a huge amount of faith in these projections right now. The details of the past forecasts reveal a sizable upside skew.

May's forecasts show inflation well below target in two years' time

Quantitative tightening

The final thing to watch – and something that’s more likely to be a story for September – is quantitative tightening (QT). A recent speech by the BoE’s Ramsden indicated that the Bank could increase the overall amount of gilt holdings it sheds over the next 12 months. Currently, the Bank is reducing holdings by roughly £80bn/year, with a mix of gilt sales, as well as simply allowing maturing bonds to roll off the balance sheet. The amount of gilt redemptions ramps up to roughly £50bn in the 12 months from September, from about £40bn in the 12 months prior. Despite that, Ramsden suggests sales volumes could be kept broadly unchanged.

That implies a new target for annual QT of £90bn, or perhaps £100bn. We’re expecting a more formal announcement in September.

The outlook: at least one more 25bp hike to come

The market-implied path for rates looks much more reasonable than it did just a couple of weeks ago. At the peak, investors thought rates could go as high as 6.5%. Now, it’s a little more than 5.75%, which implies three more 25bp rate hikes from the current 5% level. That seems fair, and while our formal forecast peaks a little below that at 5.5%, we acknowledge this is wholly dependent on further progress on services inflation and wages. That’ll determine whether we get a final 25bp hike in November, to follow the one we’re pencilling in for September.

Market reaction

The release of the soft June CPI print earlier this month knocked trade-weighted sterling some 1.5% off its highs – losses which sterling is now trying to recover. Given that the market is now pricing just over 25bp of BoE tightening on 3 August, a 25bp rate hike could see the short-end of the GBP swap curve drop around 8-10bp – which has been customary recently – and marginally weigh on sterling. Depending on where GBP/USD is trading on 3 August, the FX options market prices the risk of perhaps an 80 USD pip drop on the baseline scenario. Equally, a 50bp rate hike would be a surprise and could briefly see GBP/USD rise 80 pips, although there may be little follow-through given the BoE would probably downplay the scope for any further 50bp increases in this cycle.

Expect 10-year UK Gilt yields to lag developments at the short end of the curve, but presumably, any announcements on QT would be a surprise and have the potential to nudge Gilt yields a little higher. Looking at the bigger picture, we target Gilt yields down at 3.80% at the end of this year. Equally, by year-end we have EUR/GBP at 0.88 and GBP/USD at 1.31, where further signs of disinflation see BoE tightening expectations pared back further, but a dollar bear trend dominating.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article