Bank of Canada preview: another cut as tariffs cloud outlook

We expect a 25bp rate cut by the Bank of Canada on 12 March, taking the policy rate to 2.75%, in line with market pricing. Despite strong fourth-quarter GDP growth, the US-Canada trade spat is fuelling recession concerns and we currently forecast another cut in the second quarter. We also expect the Canadian dollar to face more downside risks this spring

Recession fears rising

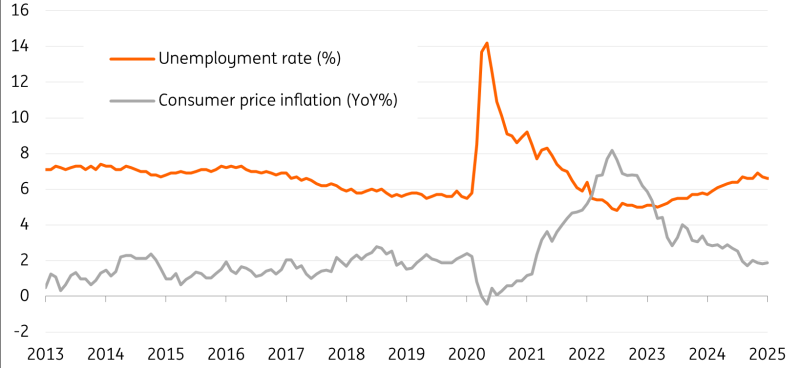

In the wake of weak growth, rising unemployment and subdued inflation, the Bank of Canada has cut its policy interest rate by 200bp over the past 10 months and is expected to follow up with another 25bp cut on Wednesday. This is despite surprisingly strong fourth-quarter annualised GDP growth of 2.6%, which was boosted by a temporary sales tax holiday that incentivised consumers to bring forward spending. Evidence from January suggests a return to the previous trend, and with the US in the process of implementing tariffs on imports from Canada, there are intensifying concerns about recession.

In a recent speech, Governor Tiff Macklem stated that “the economic consequences of a protracted trade conflict would be severe" with BoC models suggesting that the economy contracts as exports fall by around 8.5% before steadying and then returning to growth “but on a path that is about 2½% lower” than it assumed in January. After all, 76% of Canadian exports go to the US, equivalent to 20% of Canadian GDP.

Another insurance cut looks warranted

For now, Canada is in a state of reprieve with US President Donald Trump signing executive actions that delay the implementation of tariffs on products covered by the North American USMCA free trade treaty. However, with President Trump claiming he believes that trade tariffs can help reinvigorate the US economy whilst also raising much-needed tax revenues, the probability remains high that there will be a negative impact from trade protectionism.

Canada has already introduced tariffs on CAD$30bn of imported US products, and this will lift prices for items such as orange juice, appliances and motorcycles, but given that unemployment is 6.6% and inflation is broadly in line with the target, we believe the BoC has scope to implement another insurance rate cut.

Markets are fully pricing in a 25bp cut, but economists are more split, with 17 out of 25 economists expecting a 25bp cut and eight expecting no change to the overnight rate. We think the pace of cuts will slow after next week’s move and forecast just one further rate cut coming in the second quarter.

Canada's inflation and unemployment

CAD: Downside risks still dominate

USD/CAD has been settling around 1.43-1.44 after Trump’s second postponement of 25% tariffs. Current trading levels embed around 2% of risk premium into CAD. That is only half of the peak risk premium in early February (4%), and USD/CAD is now also embedding a markedly more dovish view on Fed cuts.

Our view for the coming months is that downside risks for CAD remain in place. Even without a flat 25% tariff, Canadian goods are being selectively targeted by the US, and once the “reciprocal tariff” phase kicks off in April, Canada should be disproportionately affected due to its high export volumes to the US.

As we expect the US dollar to appreciate into the summer on the back of US tariffs, USD/CAD can find support beyond the 1.45 level before easing back towards the low 1.40s in late 2025, when US protectionism may start to be scaled back.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article