Bank of Canada on track to end QE by year-end

The BoC reduced weekly bond purchases by another C$1bn, to C$2bn, as it delivered a broadly upbeat message on the recovery and left its forward guidance for 2H22 unchanged. We think the Bank will end asset purchases by the end of 2021, allowing markets to speculate on an earlier than projected hike, and providing more support to CAD

Another round of tapering, warranted by a stronger outlook

As widely expected, the Bank of Canada reduced its weekly bond purchases by another C$1bn today, from C$3bn to C$2bn. After all, the signals coming from the jobs market had been clear: Canada is on a solid economic recovery path. The Bank broadly endorsed this view, as it justified this round of tapering by stating: “This adjustment reflects continued progress towards recovery and the Bank’s increased confidence in the strength of the Canadian economic outlook”.

Aside from noting that the virus dynamics remain a key element of uncertainty and revising the 2021 growth forecast marginally lower (by 0.5%), policymakers see a stronger growth in 2022 (4.2%, about 1% higher than in April). Inflation projections for 2021 were inevitably revised higher (3.5% for 4Q21), but remained unchanged for 2022 (2.0%) and 2023 (2.4%), in line with the Bank’s view that recent spikes in inflation have a transitory nature.

In light of this, the BoC left its forwards guidance for the next rate hike for “some time in 2H22”. On asset purchases, it left the door open for further adjustments, which will depend on the state of the recovery.

Our view remains that considering the resilience of the Canadian economy, high vaccination rates, concerns about a booming housing market and government bonds that have dropped quite sharply since mid-May, the BoC remains well on track to end its QE programme by the end of the year. We are pencilling in the first rate hike in 2H22, but the risks are increasingly skewed towards an earlier move.

CAD: BoC to support gradual strengthening to sub-1.20 levels

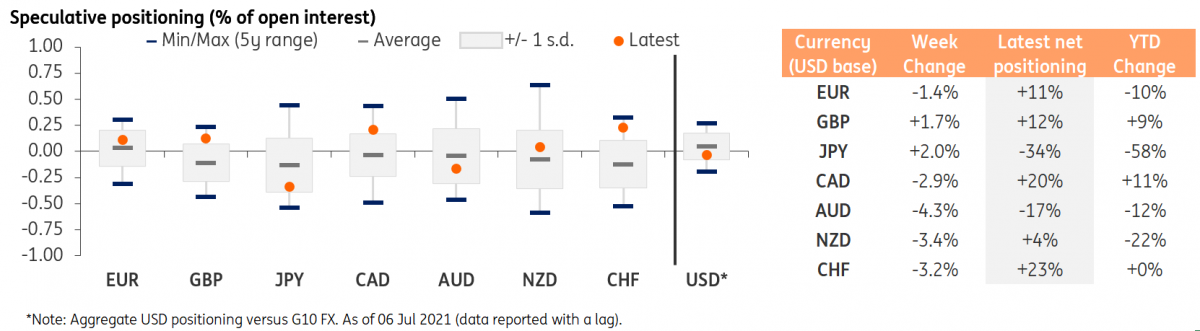

The Canadian dollar reacted to the policy announcement with a drop, as USD/CAD moved back above 1.2500 after having trended lower in the hours before the BoC meeting. Part of it might be due to some market participants expecting a larger reduction to asset purchases and/or a hawkish shift in the forward guidance or inflation outlook. However, we think the post-meeting jump in USD/CAD was predominantly a profit-taking event. After all, latest CFTC data showed that speculative positioning on CAD remained – even after the recent USD strength - considerably skewed towards the net-long area (+20% of open interest), and above its 1-standard-deviation band.

Following what might have been a long-squeezing event, we think the market will remain attracted by CAD’s set of fundamentals: a) one of the most hawkish central banks in the developed space; b) a strong economic recovery and the highest share (70%) of people with at least one vaccine dose among major economies; and c) resilient oil prices even after the turbulent OPEC+ meeting.

On the first point, we think that if our expectations that the BoC will end its asset-purchase programme by year-end proves correct, markets will be inclined to price in an earlier start of the hiking cycle in Canada. This should add to the already appealing carry profile of the loonie, which may prove a key factor driving some outperformance if, as we expect, the global recovery story consolidates and markets look to re-enter carry trades.

We remain of the view that USD/CAD will trade below 1.20 by the end of 2021.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article