Bank of Canada in holding pattern ahead of summer easing

There is a risk that the BoC turns a notch more dovish at the March meeting, given the lower-than-expected inflation figures. However, we only expect rate cuts to start in June, and take the policy rate 100bp lower by year-end. Conservative expectations on easing and the correlation with US rates bear risks for the Canadian dollar

Canada’s macro picture remains mixed

The key story from the last Bank of Canada's policy meeting in January was the removal of the line, the Bank “remains prepared to raise the policy rate further if needed” from the accompanying statement. Nonetheless, there was little inclination to back the growing market expectations of interest rate cuts. The statement reiterated that “the Council is still concerned about risks to the outlook for inflation, particularly the persistence in underlying inflation” with the annual rate of CPI expected to slow only “gradually… returning to the 2% target in 2025”.

The data since then has shown GDP coming in hotter for 4Q, retail sales being more robust and the jobs market remaining firmer than the market had been expecting. However, inflation undershot expectations with headline CPI now down to 2.9% from 3.4% in December (consensus was 3.3%) with core inflation rates slowing to 3.3% for the median and 3.4% for the trimmed versus the 3.6% rates that were expected.

But markets have scaled back cut bets

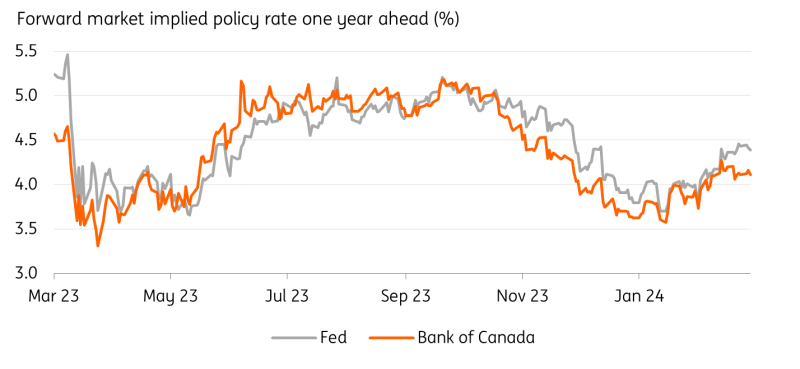

10Y government bond yields and the Canadian dollar are little changed since the January meeting, but we have seen the market scale back its expectations for rate cuts this year. Just after the 24 January decision, overnight index swaps were pricing around 105bp of BoC cuts for this year versus around 75bp today.

We believe this is more a reflection of the global repricing of interest rate moves with the Federal Reserve expected to be far more cautious on policy easing, rather than a meaningful re-evaluation of the prospects for the Canadian economy.

BoC rate expectations are strictly tied to the Fed

BoC to stay put, but rate cuts should start in June

While there is little prospect of any rate cut at the 6 March meeting and we doubt the BoC will be comfortable enough to loosen policy at the following meeting on 10 April, we do expect interest rate cuts to start coming through from the 5 June meeting onwards.

We look for 100bp of rate cuts in 2024 with a further 75bp in 2025

The effects of previous rate hikes continue to feed through since Canadian mortgage rates will continue to ratchet higher for an increasing number of borrowers as their mortgage rates reset after their fixed period ends. This will intensify the financial pressure on households, dampening both consumer spending and inflation. Unemployment is also expected to rise given the slowdown in job creation (and rising job lay-off announcements) with high immigration and population growth rates adding to the slack in the labour market.

Consequently, we expect inflation to drop back to 2% in the second half of this year rather than in 2025 as the BoC expect, which will give the BoC the opportunity to move policy to a more neutral level before anything painfully breaks in the Canadian economy. We look for 100bp of rate cuts in 2024 with a further 75bp in 2025.

Market implications

Markets are pricing in a 70% implied probability of a rate cut in June, and with three total cuts expected by year-end, we think investors are underestimating the size of BoC easing. Accordingly, we do expect soft economic data to give Canadian bonds relief at some point before the summer: as discussed above, that can come both from the Canadian side or from the US side.

In the shorter run, we suspect this meeting will not change the picture dramatically for CAD assets. Indeed, softer CPI could prompt the BoC to sound more optimistic on disinflation and start hinting at monetary easing more explicitly at the March meeting. Given the rather conservative market pricing on BoC rate cuts, we think the balance of risks is tilted to the downside for front-end CAD rates and the Canadian dollar next week.

Our core view remains, however, that the US dollar could enjoy more pockets of support as US data shows more signs of resilience in the near term, and the Canadian dollar should benefit in the crosses (especially against other commodity currencies).

CAD to lag NOK, AUD and NZD beyond the near term

Beyond the short-term, we are not as excited for the Canadian dollar as we are for the likes of Norway's krone, and the Australian and New Zealand dollars into a summer of monetary easing. First, because of our view of large easing by the BoC (unlike Norges Bank, and the Reserve Banks of Australia and New Zealand), and second because CAD shows some strong correlation with US data sentiment. Our bearish forecast for USD/CAD into year-end is primarily a mirror of USD weakness. We see 1.30 being tested this summer.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Bank of CanadaDownload

Download article