Bank of Canada cuts rates by 25bp

The Bank of Canada has clearly concluded that diminishing inflation worries and excess supply in the economy mean its monetary policy doesn’t need to be quite so restrictive. This 25bp move is likely to be followed by a further 75bp of cuts in the second half of the year. The Canadian dollar is likely to remain under pressure

25bp rate cut with more easing to come

The Bank of Canada has cut its policy rate by 25 basis points to 4.75%, as we thought it would. Around 20bp of the 25bp cut were priced ahead of time, with around 21 out of 30 economists polled by Bloomberg expecting the move.

The statement acknowledges that "indicators of the breadth of price increases across components of the CPI have moved down further and are near their historical average” while "recent data has increased our confidence that inflation will continue to move towards the 2% target.” As a result, the BoC took the view that “monetary policy no longer needs to be as restrictive”.

In the accompanying press conference, Governor Tiff Macklen went further to say that there is “sustained evidence” inflation is easing and it is “reasonable to expect” further interest rate cuts should inflation continue to slow. Nonetheless, it will be a meeting by meeting process with Macklem noting the risk of cutting rates too quickly and widening the spread further between the US and Canadian policy rates, which could have FX implications.

Weak growth, falling inflation and rising unemployment point to a further 75bp of cuts

There was also a note of caution in the press release whereby the BoC accepts that “risks to the inflation outlook remain”. Nonetheless, the activity story in Canada is a little disappointing, with 1Q GDP coming in below expectations at just 1.7%, with output flat in March. Unemployment is already above 6% and is expected to rise further in Friday’s report, with wages cooling as the slack in the labour market builds. Moreover, the effects of tight monetary policy are becoming increasingly apparent with the household debt service ratio at a record high at 15% versus 9.8% in the US.

The risk of rising loan delinquencies is very real, with unemployment on the rise, which would heighten the chances of a potential recession. Note that in this regard, three consecutive monthly falls in retail sales are not a good look at a time when immigration growth has been so strong.

Given this situation we do indeed expect further rate cuts, but we are doubtful on back-to-back moves at the July meeting. Instead we are forecasting 75bp of further cuts this year with the policy rate hitting 3.5% in Q1 2025.

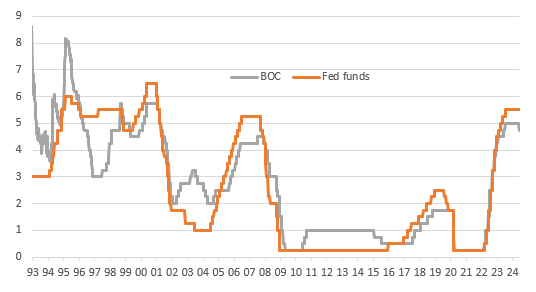

BoC - Federal Reserve policy rate differentials (%)

CAD remains unattractive after “cautious” cut

We have been calling for CAD’s weakness in the crosses for the past 1-2 months ahead of this June BoC meeting. As markets gradually increased bets on a cut, CAD showed the kind of underperformance versus other pro-cyclical currencies we were expecting. At the time of writing, the loonie is trading around 0.3% weaker against the dollar.

The post-BoC price action got mixed up with stronger-than-expected US ISM numbers, but CAD only dropped moderately after the rate cut. This is not only because markets were pricing in 20bp into the meeting, but also as the statement did not really give any strong hint on the path for future rate cuts. The pledge to move “one meeting at a time” and the expectation for more rate cuts were partly offset by concerns about the “uneven” disinflationary path and the acknowledgement that cutting too fast is dangerous. From a market perspective, this looks like a “cautious” cut, a nudge more dovish than a “hawkish” cut, which would have probably required stronger wording on a pause after the June move.

With the BoC moving in line with our forecasts, and our expectations of an additional 75bp of easing this year (around 47bp priced in), we still think CAD looks less attractive than other high-beta currencies such as NOK, AUD and NZD, where domestic central banks should wait until at least the last quarter of the year before starting to cut rates. USD/CAD short-term risks are moderately skewed to the upside, but in line with our call for US data to start pointing to a September Fed cut, the pair can still find its way into 1.35 in the second half of the year.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article