Australia - trial by fire

Australia's economy may be at a gentle turning point, but it remains vulnerable with very little stimulus on offer to provide a boost. An improving external environment remains the most positive development from 2019

What does 2020 hold?

Australia's central bank governor, Philip Lowe last year said he believed Australia was at a gentle turning point. But the evidence for this is less than clear and recent bushfires make this optimistic thesis even more questionable.

Even if it is unlikely to do all that much good, the pressure is mounting for a February rate cut by the central bank. Any further easing thereafter is likely to require some hard thinking as a cash rate of 0.25% takes rates down to the RBA’s effective lower bound. From there, unless the economy shows more signs of growth, the only options are a worrisome foray into unorthodox monetary policy.

The outbreak of the coronavirus in China also leaves a big question mark on the Australian economic outlook, given the country's high dependence on Chinese demand. At such an early stage, we are unable to assess the impact on Chinese activity so, for now, we acknowledge that the views expressed in this article are contingent on how the coronavirus story develops.

Gentle turning point?

If the Australian economy is at a gentle turning point, as Governor Lowe has suggested, then the RBA can probably sit back, relax, and watch the economy, safe in the knowledge that it will be some time before they have to step on the brakes and pull things back to order again. That is not going to be a 2020 story. It may not even be a 2021 story, but instead, that depends on a lot of factors outside the control of the RBA - the US-China trade war, US Federal Reserve policy, China’s macroeconomy, Australian fiscal policy and more recently, the weather and associated bushfires.

Even before Sydney, Melbourne and other cities and rural areas became bathed in smoke, the evidence for a continuation of the downturn seemed an easier argument to make. The 3Q19 GDP release showed quarterly growth slowing from 0.6% to 0.4%, and the upturn in the four-quarter moving average of the annualised quarter on quarter growth looks very fragile.

The 2Q19 figure was revised higher to 0.6% from 0.5%. But if anything, this faster historical growth earlier in the year makes the momentum of the economy look even more negative than if there had been no upgrade.

GDP growth

Worrying drivers of growth

The pattern of contributions to that weak 3Q19 figure doesn’t make the story look any better either. Public spending provided one of the largest contributions to the total growth figure. That can’t be expected to continue given the budgetary rigidity of the current government. If anything, with the prime minister and finance minister remaining resolutely committed to returning the budget to surplus next year, we might expect this part of the growth story to turn from a boost to a drag.

Contributions to YoY GDP growth

How do the bushfires change the arithmetic?

Governor Lowe has put a good deal of weight on the health of household spending. But here, the news remains mixed. The 3Q19 contribution of consumer spending to the GDP QoQ total was only 0.1pp. Retail sales data in November bounced strongly (0.9%MoM), but only after a very weak October reading (0.1%MoM). Since then, the widespread bushfires may have weighed further on seasonal sales volumes in December and we could see private consumer spending disappoint again in 4Q19.

Some commentators have likened the bushfires to other natural disasters like earthquakes – arguing that the negative balance sheet impacts (damage to property and so on…) may have a relatively muted impact on the national profit and loss account (GDP).

We think this is wildly misguided. While there is clearly a considerable amount of balance sheet damage, lives lost, property destroyed, businesses lost, environmental degradation and so forth, there is clearly also a lingering hit to economic activity too that makes the impact of these fires on GDP more closely resemble something like the SARS epidemic in Hong Kong in 2003 than an earthquake such as the one in Christchurch in 2011. For that reason, we are pencilling in a bigger hit to activity in 4Q19 and 1Q20, before recovery later in the year. Only then, will the repair and replacement activity begin to provide a partial offset to the preceding weakness.

Natural disasters and GDP

Labour market sluggish

One of the key underpinnings for household spending will be the state of the labour market. Here, wage growth remains very sluggish, as it is in most developed economies. This global phenomenon has multiple causes – globalisation, automation, and substitution of labour for capital. But it doesn’t seem likely to go away soon, whatever its cause.

The latest available hourly wage growth is for 3Q19 and was recorded as 2.8%YoY with bonuses, but only 2.2% without. That basic/bonus split can be important as bonus related payments are more likely to be saved than spent. Non-bonus wages are also lifted by the public sector, which is currently providing more generous pay growth of 2.5%YoY than the private sector (2.2%). The government’s zeal for budget progress makes future public wage settlement generosity seem unlikely. In other words, wage growth could fall just as easily as they could rise in the year ahead.

Wages, inflation and unemployment

Unemployment can't fall enough to boost wages

Meanwhile, the unemployment rate, although low at 5.1%, remains higher than the RBA’s latest thoughts on what constitutes full employment (4.3%), and therefore a rate at which wages will begin to accelerate. With only 50bp of conventional monetary policy ammunition left in the RBA’s arsenal, this seems altogether inadequate on its own for driving unemployment down sufficiently to drive wages meaningfully higher.

Employment growth comes in fits and starts, with erratic switches between part-time and full-time labour. The recent news has suggested that on a full-time equivalent basis, employment growth has slowed, especially for full-time jobs. That said, it is hard to be sure this is a trend that will persist. As a result, it seems very hard to imagine a scenario where unemployment falls sufficiently to make much of a difference to the unemployment rate. And with that backdrop, we aren’t anticipating much of an improvement in wages growth in 2020.

Cumulative employment growth

Housing looking stronger

While monetary policy looks to have lost some of its ability to stimulate the economy, the housing sector is one part of the economy that remains sensitive to interest rates and has benefited from RBA easing.

Most regional property markets are now seeing prices rise rather than fall - so much so that there is mounting concern that the RBA’s actions may have unleashed the next property price bubble. At this stage, we don’t think the evidence supports this concern. And price increases remain in low single-digit ranges, consistent with nominal GDP growth, even if a bit faster than nominal wages growth. Unless we see some acceleration in the quarterly annualised growth rates, then there should be no need for this to present any constraint to further RBA easing, though it will be worth watching, and could require some action from APRA in terms of bank lending restrictions for property purchases.

Although strictly speaking, it is a part of the investment complex of Australia’s national accounts, the outlook for housing is relevant for household confidence and balance sheet effects on consumer spending. A faster churning housing market also drives demand for furnishings and DIY equipment and is generally supportive for household spending. Meanwhile, a positive asset effect on household balance sheets enables direct cash flow improvements through equity withdrawal as well as indirect feel-good-factor spending.

Businesses not investing

Despite the low yield environment, business investment remains lacklustre. This is also a common global theme, and trade war uncertainty has likely played an important role. It is also a good argument for not cutting rates further, as this does not seem to be an effective remedy and is hard to reverse.

Again, the most likely cure for this feeble investment demand would be a more positive global environment driven by the rollback of tariffs and increased global trade. The phase one deal between the US and China may deliver some improvement. But we are cautious as the scale of tariff rollbacks it contains are really very small, and the bigger benefit was the avoidance of additional tariffs, not the removal of existing ones.

Talk of a phase two deal seems unrealistic in our view, and even US President Trump is downplaying thoughts of this happening this side of the Presidential election.

Despite little genuine progress on trade, China continues to grow, albeit at a rate that trends slowly lower. Infrastructure spending is providing most of the new momentum for Chinese growth and that does require raw materials, which can be provided by Australia.

Gross fixed capital formation

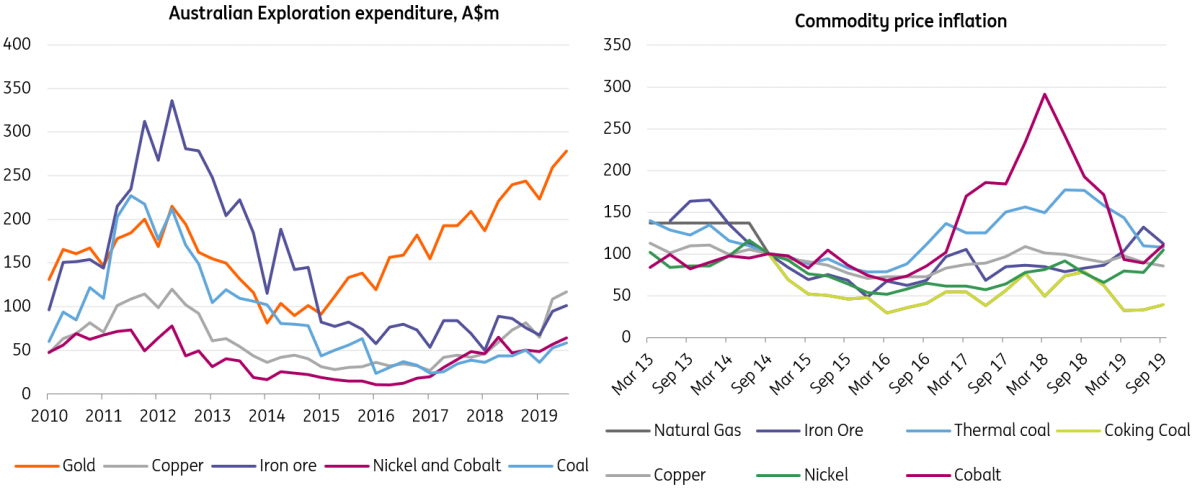

Extraction industries clawing their way to growth

There is some slightly more promising news from the extraction industries, which, following the boom years of 2011-2013 has been deeply uninspiring. Investment in mining capacity could turn more positive in 2020. But so far, the bulk of the expenditure in this industry has followed commodity prices. That has meant that investment in gold extraction has increased steadily, as the yellow metal has been lifted by cuts to Fed funds and a return to quantitative easing by the European central bank.

Extraction exploration expenditure and commodity prices

Terms of trade and the AUD

But investment in extraction of other commodities, iron ore, nickel and cobalt have improved only slightly, reflecting prices that remain soft.

Coal prices have been stronger, but the world of finance is turning on dirty industries like coal, so any investment there is likely to have to come from retained profits. And as the world slowly becomes greener, such investments may not appear sufficiently attractive in the long run by incumbents to be considered worthwhile.

In concert with the modest pickup in commodities production, Australia’s net export sector has been a further provider of support to the economy, with export growth improving by around AUD 8bn per month over the last two years, whilst imports have grown less than half this amount. Helping this trend along, the real broad effective exchange rate has been in almost permanent decline since mid-2017 adding to Australia’s competitiveness. Further RBA easing will almost certainly provide further motivation for additional declines in both the real effective exchange rate as indeed it will to the nominal spot rate. The main danger from this is that Australia, one of the US’ closest allies, will fall under the radar of the US Treasury FX manipulator team.

The net result of this has been a fairly dramatic turnaround in the Australian trade balance. Bearing in mind that Australia has been a small, but fairly persistent trade deficit country for most of the twenty-first century, and before that basically ran a trade balance, the recent swing to a surplus is quite a significant development. It would likely need substantial improvements in domestic demand to put a dent into this surplus, and that doesn’t look imminent at the moment.

Trade balance is positive

The exchange rate is not an impediment to growth

So, the balance for inflation and growth seems tipped to further RBA easing, but with the better balance on the trade account, and the fact that then AUD is not simply a relative rates play, but also a litmus for the US-China Trade War, there is scope for some support for the AUD in 2020.

While these offsetting factors will tend to keep AUD/USD trading in a range in 2020, with many of the same drivers in 2020, but a less dovish central bank outlook, one way to express a downbeat view on the AUD would be best expressed through AUD/NZD, favouring the NZD.

Real and nominal effective exchange rates

Market outlook

The outlook for inflation from all of this is very benign. If you still believe that inflation derives from pushing output or employment above its potential, then you probably also have to accept that the trade-offs between capacity and higher prices are now much flatter than in previous business cycles and that any inflation recovery is likely to be modest.

We do forecast some recovery in inflation in 2020. It would be hard not to as the first quarter of 2019 inflation was so weak, that barring a repeat of that, inflation is likely to increase even with only a modest increase of the price level over the quarter. Inflation in the first quarter of 2020 should register something like 2.2%YoY, with inflation over the remainder of the year fluctuating between 2.0 and 2.2%. But the underlying trend still looks very weak, with non-tradeable inflation running at only a little over 1%, so most of the inflation in Australia is imported.

Current inflation and target

Inflation to rise, but remain in the lower half of the RBA's target band

An inflation out-turn like the one described above would still be in the lower part of the RBA’s 2%-3% inflation target - a target which does not look like it is going to be changed any time soon - but which remains high by international standards, against an average target rate of 2%. That 2% average rate itself looks like an anachronistically high level, set when inflation typically came in between 3 and 4%.

In any case, low but greater than 2% inflation should be enough to stop the RBA moving beyond the one cut we have pencilled in and will keep policy confined to conventional measures (see later section). But it should see the 3m Bank bill rate decline to about 0.65% (around a 15bp spread over the official cash rate) by 2Q20.

Bond yields in Australia are substantially lower than comparable US Treasuries. The 10-year benchmark Australian government bond currently trades at about 60bp through 10Y US Treasuries at 1.10%. With inflation expected to rise very slightly during 1H20, and inflation expectations likely to follow it higher, the 10Y Australian government benchmark probably only has a further 20-30bp to decline, taking it to a low of 0.85%. That view remains hugely dependent on the global yield environment, and a more positive trade environment could well see global government bonds sell-off as risk aversion dissipates, lifting yields 20bp or more above today's yields, even with RBA cuts.

So these are forecasts we provide with a very large health warning.

What might unorthodox monetary policy look like in Australia?

Given the likelihood of some further RBA easing, one question that is worth considering is what would lead the RBA to take the leap to unorthodox monetary policy (UMP), and what might that look like?

First, it’s worth noting that RBA Governor Lowe is no “inflation nut”. He has talked very sensibly also about the potentially counterintuitive influences of very low nominal interest rates on household and business expenditure and seems (correctly in our view) to have ruled out using negative interest rates to try to boost the economy.

He still talks about the use of “forward guidance” as an alternative, when, in our view, unless there really is something that a central bank is telling you about their intentions, strong hints to the effect that “rates may be on hold for a long time” should be so blindingly obvious from the data and prevailing conditions that any central bank's public expression of this will be totally redundant. A good example of redundant "forward guidance" would be the Bank of Japan's commitment to a 2% inflation target. No one believes it, probably not even the BoJ, yet they resolutely stick to it.

Given the likelihood of some further RBA easing, one question that is worth considering is what would lead the RBA to take the leap to unorthodox monetary policy (UMP), and what might that look like

The alternative is that the central bank deliberately overstates the case for an extension of low rates to generate a greater short-term influence. There are a number of things wrong with this. On the one hand, no-one, including the central bank has perfect foresight, so making a strong statement about the future when the future is extremely uncertain will have little market credibility. Alternatively, if conditions do turn out to be better than was originally suggested, requiring revised guidance, then this will result in an abrupt market correction. In short, it is not clear to us that forward guidance has any credible part to play in a central banks arsenal when they hit the lower effective policy bound, although they all seem intent on trying to use it.

In the end, this really only leaves quantitative easing. The outstanding stock of Australian central government bonds was about AUD630bn at the end of 2Q19. That equates to around 45% of nominal GDP. That isn’t much compared to many other central banks that have undertaken QE and this probably means that the RBA would be quite tentative about the pace at which such a programme was undertaken. Adding in state and local government bonds doesn't help too much either as amounts are again small.

Central government's outstanding debt

Australia isn't well suited to QE type policies

An alternative might be to buy the bonds and commercial paper issued by the banking sector which is essentially the cost of capital at which banks fund themselves, given that this sector is heavily reliant on wholesale funding.

There are roughly equal amounts of bank bonds and commercial (one-name) paper equivalent to around 25% of GDP. The RBA could make a meaningful dent in bank borrowing costs, and in turn, bank lending costs by buying this paper.

A monthly target of AUD5bn purchase of this paper could equate to an annual amount of roughly 6% of the outstanding bank paper issued in Australia. This would be comparable in scale to the ECB’s current (and also non-emergency) buying of government bonds (EUR20bn per month of a stock of about EUR4trillion government debt).

Currently, Australian banks fund long-term (5Y) at around 90bp over the equivalent benchmark 5Y government bond (0.77% at the time of writing). That seems a lot for say a AA- bank even against AAA-rated government paper, so this would be one way of lowering term-lending rates for the corporate sector and households.

Bank paper outstanding

Main problem might be public approval

Squeezing down banks’ borrowing costs and consequently lending costs could also be achieved through an extended repo facility with lending contingent on pass-through to corporates and households (the former probably more than the latter). This would resemble the Bank of England’s funding for lending scheme.

The main impediment to any scheme of this sort would seem to us to be the political backdrop, with the banking sector not exactly flavour of the month, purchasing bank paper might need a contingent agreement to extend certain types of lending and not using it to fatten net interest margins, which might go down badly with a sceptical public and hostile media.

AUD: Grim short-term outlook, valuation to prevail in the long run

The Australian dollar has recently erased all year-end gains (which were partly linked to a globally weaker US dollar), as market sentiment deteriorated and the rate outlook remained unattractive due to prospective RBA easing this year.

The futures market is currently pricing in one full cut (25 bps) by 1H20 and approximately 10bp of extra easing in 2H. Expectations about the rate path have been fiercely repriced lately after a marginal decrease in the December unemployment rate and inflation creeping up to 1.8% – the implied probability of a cut in February is now below 10%.

We highlight the risk of the RBA cutting earlier than market expectations, which represents one of the key downside factors for the AUD in the short term. In particular – even though we see a second cut as unlikely – markets may price in more easing after the cut unless the central bank clearly states the one-and-out nature of their move.

The AUD is a quintessential proxy currency (more than the NZD) for China-related sentiment, so any rise in virus-related fears are likely to be channelled via AUD weakness in the G10 space

The cooling down of US-China trade tension appeared to have set market risk-sentiment on a recovery path, but geopolitical risk including Iran and now the outbreak of the coronavirus have dented risk appetite since the beginning of the year. Predicting developments as the virus spreads is beyond our expertise, but it is important to note how the AUD is a quintessential proxy currency (more than the NZD) for China-related sentiment, so any rise in virus-related fears are likely to be channelled via AUD weakness in the G10 space.

The bushfire situation is also curbing AUD upside as there is still a high degree of uncertainty about how long the environmental emergency will last and what the economic consequences will be.

On the commodity side, the outlook for mainstream Australian exports doesn't look very bright. Despite the negative implications of the coronavirus outbreak on most commodities, our commodities team highlights a significant idiosyncratic downside risk for iron ore prices – due to the probable recommencement of supply from Brazil – and coal prices – this mostly relates to a shift towards natural gas. On the flip side, gold and copper present a more constructive outlook, but unlikely to offset the generally unsupportive commodity backdrop.

All these factors lead us to conclude that the Aussie dollar is facing a bigger downside risk when compared to its pro-cyclical peers. For this reason, we suspect investor appetite for the currency will remain broadly subdued in the first half of 2020.

However, over the long-term, the outlook appears less grim. The AUD is the most undervalued currency in the medium term within the G10 space: approximately 10% according to our BEER model (chart below). In the second half of the year, global stabilising risk sentiment, paired with our view of AU rates bottoming, as the central bank ends its easing cycle, the convergence of inflation to the RBA target lower-bound and the start of a weakening in the USD should all play in favour of a recovery in AUD/USD.

The Aussie dollar is the most undervalued G10 currency

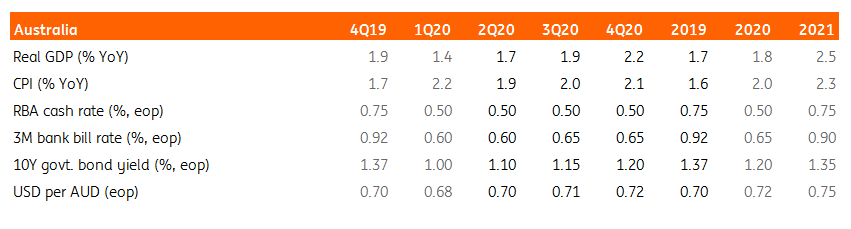

Forecast summary

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

29 January 2020

Good MornING Asia - 30 January 2020 This bundle contains 3 Articles