Australia: GDP growth to remain below 2% this year

- 9 January 2023

- Australia

While parts of the Australian economy, in particular the labour market, remain robust, there are already clear signs that the economy is slowing, and it should slow further in 2023. That at least will provide some scope for a relaxation of monetary policy as inflation is also showing signs of peaking out

Australia: At a glance

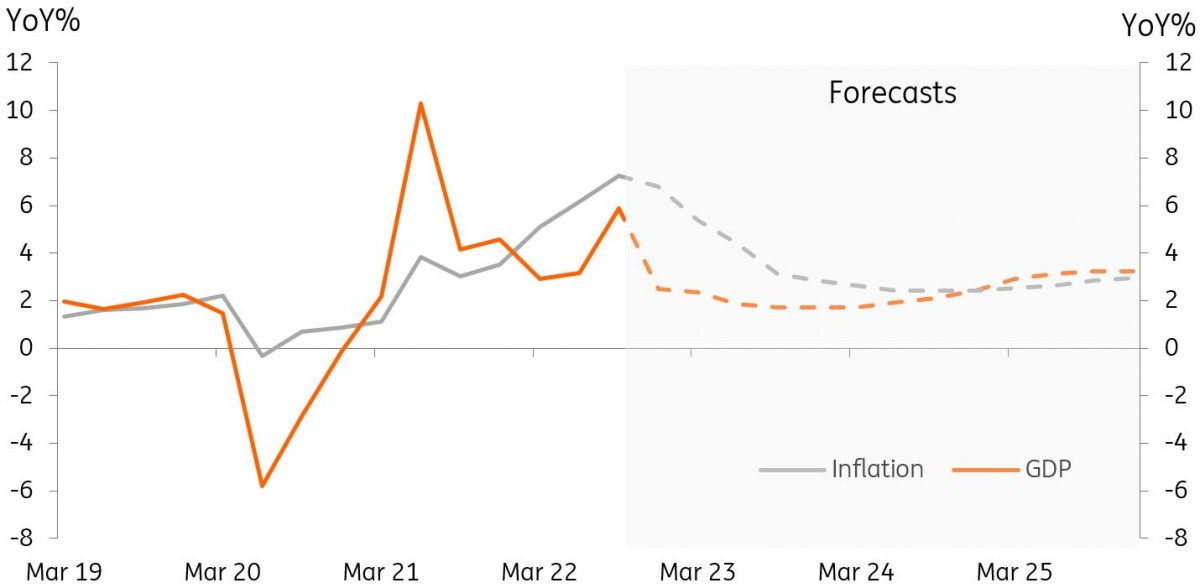

The Australian economy is slowing down. In the third quarter of 2022, the GDP growth rate dropped to 0.6% quarter-on-quarter. And even though that still leaves the year-on-year growth rate looking very robust at 5.9%, most of that is due to base effects, and that growth rate will drop sharply in the fourth quarter of 2022. Inflation also appears to have peaked, with the new monthly CPI series showing inflation dropping below 7%. House prices too have been falling rapidly in the last quarter as the Reserve Bank of Australia has increased the cash rate to squeeze out inflation. Business investment remains depressed thanks to the higher rate environment and weak external backdrop, and while the trade surplus remains impressive, it is no longer adding to growth. The Australian dollar (AUD) has been moving in line with broader US dollar (USD) trends and is showing signs of strengthening again.

GDP and inflation outlooks

3 calls for 2023

GDP growth to be less than 2% in 2023

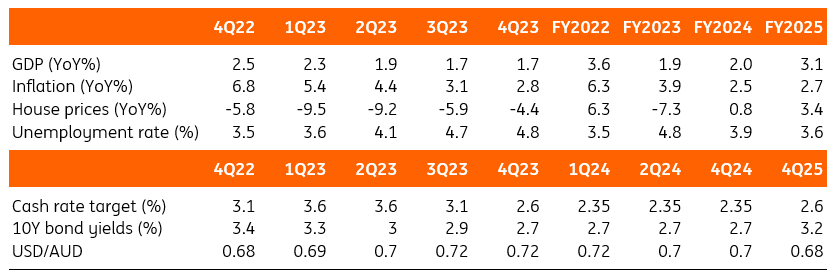

GDP growth should fall below 2% for the full year. After projected growth of around 3.6% for 2022, GDP growth is expected to slow to a sub-2% pace in 2023. The household sector is running out of room to keep spending growing in the face of higher inflation and much more subdued nominal wage growth. Households are also running out of room to smooth spending by reducing savings, as savings rates have already fallen sharply from their pandemic peaks and the falling values of real assets (property) will also weigh on their balance sheets. Large discrete mortgage re-sets will probably not do too much damage, as many households are already making overpayments, but this will cause problems for some.

House prices will fall from their 2022 peaks

House price growth should drop to nearly -10% YoY. In year-on-year terms, median Australian house price growth has already fallen from its pandemic stimulus-induced peak rate of 25.0% YoY, to just 1.1% YoY in 3Q22. Further small quarterly declines in the first and second quarters of 2023 will all but ensure that the annual rate of house price growth falls to close to -10% YoY at its most negative, delivering a full-year decline of just over 7%. Prices should stabilise by the end of 2023, but it may be closer to the end of 2024 before house prices are recording positive year-over-year growth rates again.

Cash rates close to peak and could fall

Cash rates will peak at only 3.6% and will start to be reduced before the end of the year, in our view. The cash rate target was raised a further 25bp in December and now stands at 3.1%. We are calling for a peak rate of only 3.6%, in other words, after only another two rate hikes of 25bp each. This forecast derives from our assumptions of more slowdowns in GDP growth, further declines in consumer price inflation, worsening negative house price growth, and the discrete impacts of rate hikes on mortgage payments. Rates ending the year lower than their forecast peak will lessen the subsequent re-set impact in early 2024 and sow the seeds for a broader recovery.

Australia forecast summary table

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Asia Outlook 2023: Darkest before the dawn

- This bundle contains 11 Articles