Reserve Bank of Australia’s big decision: to hike by 25bp or 50bp?

- 1 July 2022

- FX Australia

The Reserve Bank of Australia (RBA) faces a dilemma at its forthcoming meeting. To hike by 25bp or 50bp? We feel the odds are stacking up firmly for 50bp. Even in the event of a hawkish surprise, expect very limited benefits for AUD in the near term

| 25bp / 50bp? |

Cash rate target hike |

What's the real question here?

Most central bank meetings come down to a fairly binary choice: hike or don't hike; cut or don't cut. For the RBA's July meeting, the choice is to hike by either 25bp or 50bp. Why? Well, RBA Governor Philip Lowe told us so a little over a week ago. On 21 July in the Q&A after a speech to the American Chambers of Commerce in Australia (AMCHAM), Governor Lowe said: "We’re going to look at the data we have each month and the level of interest rates and the inflation. But I expect that next month we’ll be having the same discussion at our board meeting: 25 or 50."

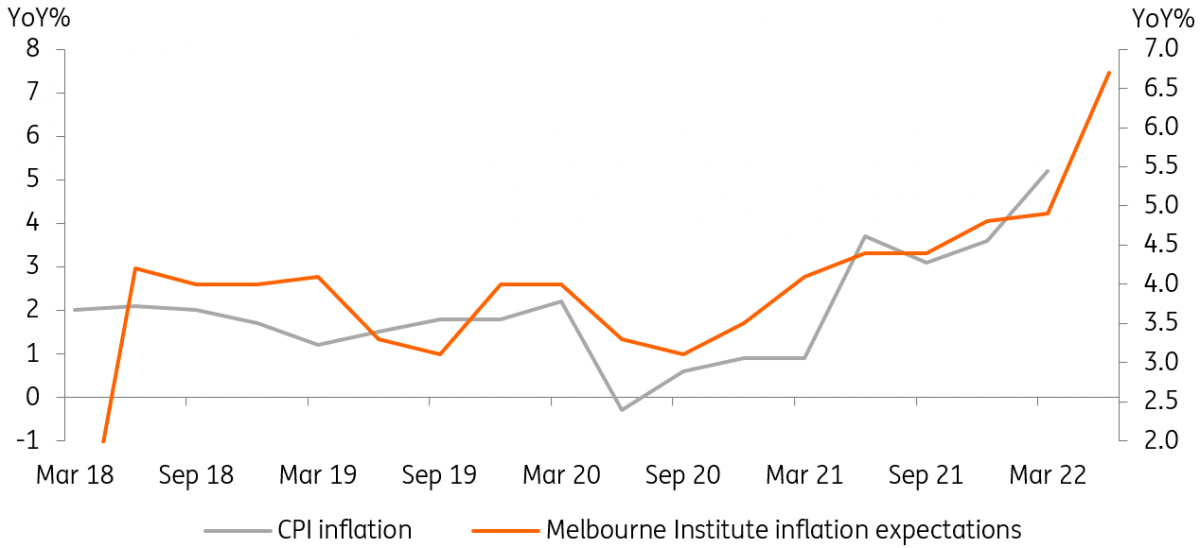

Inflation and inflation expectations

Not much to go on

The RBA has told us that their decisions are going to be data-dependent, but there has been very little data released since the last RBA meeting on 7 June. We have had some slightly soft business and consumer sentiment surveys, a decent labour market report (no wages data though), and importantly no inflation data, as this is of course released only quarterly.

What we have had though is some inflation expectations data from the Melbourne Institute. Central banks get very agitated by evidence that inflation expectations are becoming unanchored. So the 6.7% print in the latest release from this institution should have banished any thoughts of a lesser hike or even no hike at all.

The other factor to consider is that with the latest inflation rate at 5.2%, and probably higher when we get the 2Q figure on 27 July, at 0.85% the RBA cash rate target is well off where it needs to be to even remove stimulus from the economy, and even further away from actually starting to restrict growth and bring inflation down. So it has to be at least 50bp.

Why not 75bp?

There is an argument for a bigger hike, but it sounds as if the decision has already been made not to consider a 75bp or larger hike, despite the considerable ground that the RBA needs to make up.

One factor taking pressure off the RBA to hike even more aggressively at this meeting is that it meets to discuss monetary policy monthly, not every six to eight weeks like the US Federal Reserve.

This means that it can cover a similar amount of ground over a quarter with smaller incremental rate increases than the Fed can. Also, it gives the central bank a little more flexibility next month, when it will have got new hard data on inflation to consider. There may well be a case for a larger hike at the August meeting, or in September after the wage-price data on 17 August. So holding a little tightening flexibility in reserve at this next meeting leaves more dry powder to potentially respond later this quarter.

Medium-term outlook for rates

With the cash rate target now 0.85%, and likely to get to 1.35% at this coming meeting, where do we expect rates to finish the year? We are assuming that the inflation data for 2Q rise, but don't necessarily require a larger 75bp hike response. That would take rates to 1.85%. The wage price data will most likely also provide an excuse for a further 50bp hike in September, taking rates to 2.35% by the end of 3Q22. At this point, rates will probably be approximately neutral with respect to inflation and the economy, so the RBA should be able to slow the pace of further increases. We are assuming a further 75bp by year-end taking rates to 3.1%. In contrast, our house US view has the upper bound for the Fed funds rate at 3.75% by the year-end.

It's not obvious that this will mark the end of the RBA's tightening, but we think the US might well be coming close to the end of its tightening cycle by then. And with the RBA traditionally loathe to appear more hawkish than the Fed, this could indeed be the top, or close to it for this rate cycle. For now, we have rates peaking at 3.6% by 1Q23 and moving lower by the end of the year, though the 2023 forecasts are subject to considerable uncertainty and do not represent a high conviction view.

Cash rate and Fed funds (upper bound) forecasts

FX: Major headwinds for AUD to persist

The Aussie dollar slipped around 9% in the second quarter, in line with widespread losses among most pro-cyclical currencies. At the end of this week, we have seen some intensified pressure on AUD, which largely boils down to markets re-entering defensive FX trades after some quarter-end rebalancing flows got in the way, as well as the soft environment for commodities. Australia’s main export, iron ore, is facing exacerbated vulnerability on the back of resurfaced fears that the Chinese government will levy steel curbs, at a time when stockpiles data already start to suggest a somewhat weaker demand.

All this means that the Aussie dollar approaches the July RBA meeting with mostly headwinds, and a significantly weakened link between domestic monetary policy dynamics and AUD/USD suggests that a rebound towards the 0.7000 mark is unlikely to materialise soon even in the event of a hawkish surprise by the RBA (markets are not fully pricing in a 50bp hike).

The size of RBA tightening likely has implications for FX only beyond the short-term, and in an environment where markets feel more comfortable with their pricing of a global slowdown and see the peak in rates, which could fuel a stabilisation in global risk sentiment and re-connection between short-term rate dynamics and FX. From this perspective, a more aggressive RBA tightening can suggest a wider room for AUD/USD recovery towards the end of this year and the start of next year (assuming that’s when market sentiment begins to recover), but a number of other factors – especially related to China’s demand and the USD outlook – will continue to be playing a big role too. All this makes any consideration about the AUD outlook purely based on rates dynamics still reductive.

Our baseline scenario for now is a gradual return to above-0.7000 levels in AUD/USD for the remainder of the year, with most gains likely concentrated in 4Q, when the USD could start giving up some gains.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more