Asia week ahead: Where is the inflation?

Asian central banks will try to make sense of inflation data as lots of it is lined up next week. Bank Indonesia policy meeting will be an interesting watch in all of this

A raft of March inflation figures

Aside from India and the Philippines, there is literally no inflation in the region - and a raft of March price data should make this point.

Japan, Hong Kong, Malaysia, Singapore, and New Zealand report CPI inflation figures next week, while Korea’s PPI data also is due.

The hike in fuel prices and the low base effects are working together to pressure inflation upwards in some countries like Malaysia and Singapore. But this is likely to be transitory given that demand-side pulls on prices continue to be muted and should remain so for some time to come.

Inflation in Japan continues to be in the negative territory; in Hong Kong, it’s close to zero, while Korea and New Zealand are seeing some upward momentum.

Indonesia central bank meeting

Inflation isn’t a major issue for Asian central banks at the moment, but the transmission of higher US Treasury yields to local government bonds has frustrated their accommodative policy.

Bank Indonesia (BI) has been among the leading Asian central banks to suffer the onslaught of the recent US Treasury sell-off. Despite Indonesia’s low inflation in decades (1.4% YoY in March) and the central bank holding its main policy rate at a record low of 3.50% - local government bonds were among the hardest hit in Asia with almost 70 basis points year-to-date spike in 10-year US Treasury yields passed on to the Indonesian counterpart.

The key question this might pose for BI policymakers as they meet next week (20 April) is whether they should limit the upside in bond yields with a further rate cut while low inflation still allows. However, they are also worried about rate cuts intensifying depreciation pressure on the Indonesian rupiah. The currency has been an Asian underperformer to date with a 3.5% depreciation against the USD, and this could be potentially inflationary.

Such a dilemma suggests policy status-quo likely to be the central bank's best course of action - and our house forecast of rates on hold aligns with market consensus.

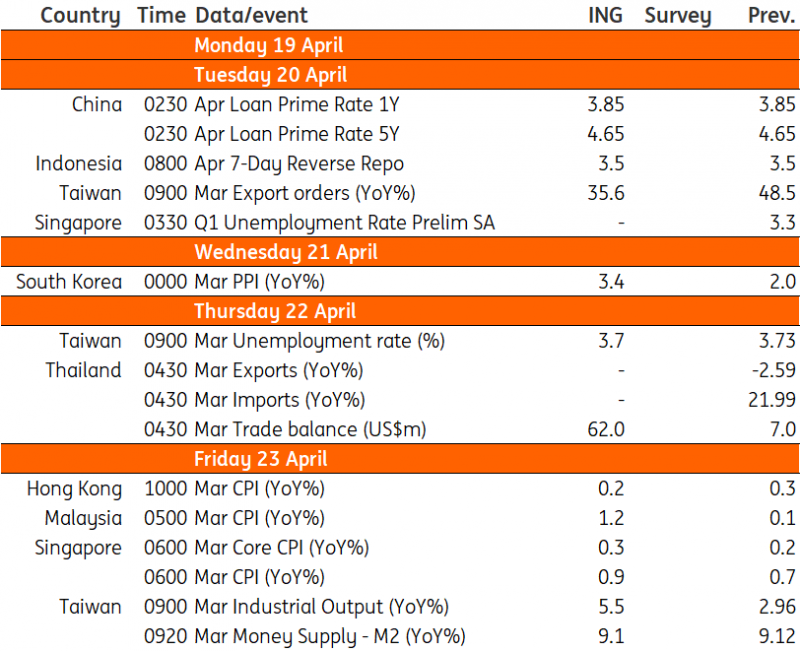

Asia Economic Calendar

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

16 April 2021

Good MornING Asia - 19 April 2021 This bundle contains 5 Articles