Asia week ahead: Two key central bank meetings

Next week's Asia calendar features key central bank meetings in Australia and India. Meanwhile, Korea reports trade figures, China will release PMI, and we will also get a look at inflation readings from the region

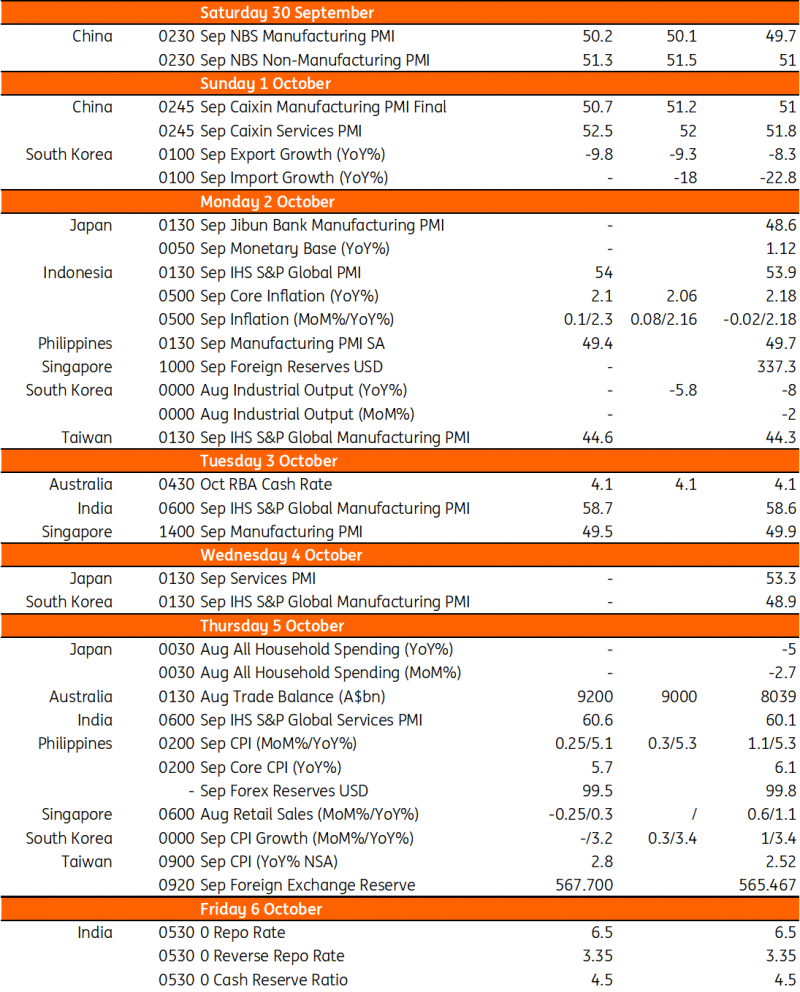

China’s official PMI likely to show expansion

China’s official PMI shows that manufacturing activity contracted for five consecutive months between March and August.

Recently released data on Chinese industrial profits showed a rise after five consecutive contractions, which might signal that the economy has stabilised to a certain extent.

We believe that the official manufacturing PMI for September will show a slight expansion reading of 50.2. With the improvement in recent activity data including retail sales, the non-manufacturing PMI may also increase slightly to 51.3.

Central bank meetings in Australia and India

The Reserve Bank of Australia (RBA) will have its monthly meeting next week to decide on the key cash rate. The latest CPI figure for August stands at 5.2% year-on-year, the first increase since April and still way above the RBA’s target of 2-3%. However, it should not be too much of a concern as the rise in inflation was largely due to base effects and soaring oil prices. While we believe that the latest inflation figures bolster the case for the central bank to further increase rates at some point, we don’t think that it will choose this meeting to tighten.

The Reserve Bank of India (RBI) is likely to keep its repo rate unchanged as India’s inflation is trending down after a surge in vegetable prices in July. Seasonal food prices have reduced since then as supply conditions have improved following erratic monsoon weather. Currently, the RBI’s third-quarter inflation forecast is above 5%. As such, rates may remain unchanged through the year-end.

Inflation numbers from Indonesia, Philippines and Korea

We’ll be getting inflation numbers from Indonesia, the Philippines and Korea next week. Soaring global energy prices has led to higher transport and energy price levels in these countries, raising the expectation of inflation.

For Indonesia, we expect inflation to inch higher due to food as well. Rice prices recently touched a multi-year high on tight supply of the grain. Despite the projected pickup, headline inflation remains well within target and should settle at 2.3%YoY.

Meanwhile, for the Philippines, we expect inflation to stay elevated and above target for another month. Rice prices could still edge higher despite a presidential order capping rice prices on select varieties of the all-important staple. We could see Philippine inflation settle at 5.1%YoY, well above target and the main reason why the Bangko Sentral ng Pilipinas (BSP) has suddenly turned extremely hawkish.

It's a similar situation in Korea, with the main drivers of inflation also food and fuel prices. Headline inflation is expected to rise to 3.2% YoY for September. This will likely strengthen the government’s efforts to curb inflation by offering shopping vouchers, extending the fuel tax cut programme, and holding utility fees for the fourth quarter.

Singapore retail sales

Next week also features retail sales from Singapore. August retail sales will likely manage to expand modestly, although still-elevated inflation and overall subdued economic activity could cap any gains. Soft retail sales amid falling industrial output will likely drag on overall third-quarter GDP.

Korea trade data

Preliminary data on Korean exports in early September pointed to a gain of 9.8% YoY, largely due to favourable calendar effects. We believe that full-month data however could record a contraction as data suggest poor semiconductor exports and softer shipments to China continue to drag on overall exports.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

28 September 2023

Our view on next week’s key events This bundle contains 3 Articles