Asia week ahead: Singapore budget steals limelight

A hike in Singapore’s good and services tax (GST) seems to be a done deal but it bodes ill given already weak domestic spending

| 1.5-3.5% |

Singapore growth in 2018Official forecast |

Higher consumption tax in Singapore

An annual rite of spring, Singapore’s Finance Minister Heng Swee Keat unveils the Budget for 2018 on Monday, February 19. The budget is likely to reaffirm official 1.5-3.5% growth and 0-1% inflation forecasts for 2018. Over the last two years, Singapore’s economic growth has recovered close to the top end of the government’s estimate of potential growth of 2-4% (3.5% in 2016 and 3.6% in 2017). However, firmer headline growth masks underlying weakness, reflected in domestic demand and stubbornly low consumer price inflation. With the end of last year’s export surge, sustaining the current rate of GDP growth in coming years will entail continued fiscal pump-priming.

Higher GST could depress consumer spending

The government has flagged a rapid rise in public expenditure in the coming years, though this will also be accompanied by a drive to raise tax revenue. A well-publicized tax initiative in the 2018 budget is a hike in the Goods and Services Tax (GST). It looks like a done deal with a 2 percentage point hike to 9% to be phased in over two years, while bringing e-commerce under the GST net is also under consideration. The move may be some help in the recovery of inflation from its current low level (0.6% in 2017). But the risk is that a tax hike could potentially backfire by depressing consumer spending further.

Some inflation relief in Malaysia

Hong Kong and Malaysia report consumer price inflation data for January. Inflation in Hong Kong has hovered around 2% since April 2017, which is where we expect it to remain in January and in most of 2018. In Malaysia, the high base effect from administered fuel price hikes in early 2017 should push year-over-year CPI inflation lower; The ING forecast is 2.7%, down from 3.5% in December. The high base and appreciating Malaysian ringgit (MYR) are expected to moderate inflation this year, possibly keeping it closer to the low end of the government’s 2.5-3.5% forecast.

Growth slowdown in Thailand

Thailand’s GDP data for the fourth quarter of 2017 is also due. The majority of Asian economies posted a GDP slowdown in the last quarter. We expect Thailand to join in. This is another Asian economy plagued by weak domestic demand and persistently low inflation. Most of the uplift in GDP growth in 2017 to our estimated 3.8% from 3.2% in the previous year was from exports and inventory accumulation. The strong Thai baht will be a threat to the export-led recovery and the Bank of Thailand will not want to complicate matters by joining the global tightening cycle.

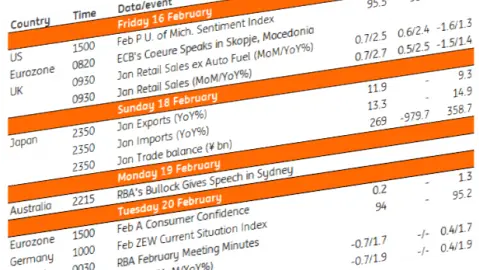

Asia and Latin America Economic Calendar

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

14 February 2018

Our view on next week’s key events This bundle contains 3 Articles