Asia week ahead: Reserve Bank of Australia to decide on rates

Next week's data calendar features a rate decision by the Reserve Bank of Australia, plus we'll get August inflation readings from the region

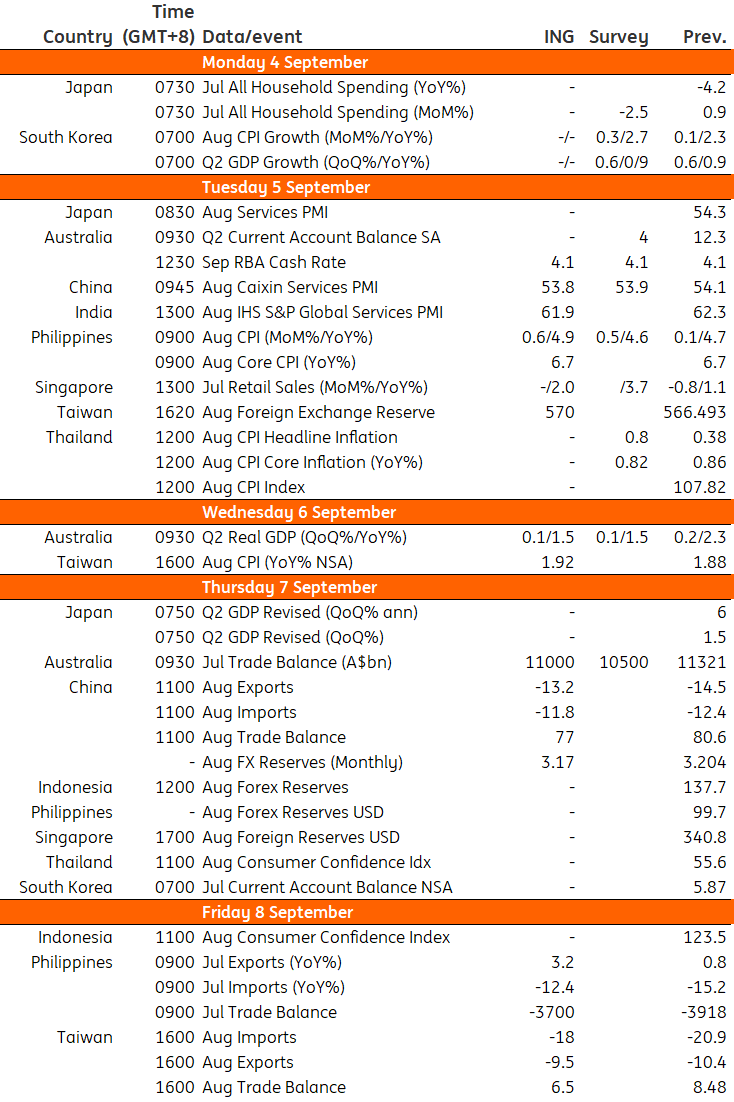

RBA to continue rate pause

The Reserve Bank of Australia (RBA) will meet next week to decide if the current rate pause will continue. July’s CPI came in at 4.9% year-on-year, lower than June’s 5.4% and below the survey consensus of 5.2%. This is the lowest pace of inflation since it peaked last December at 8.4%.

On top of cooling price growth, the latest unemployment rate also increased from 3.5% in June to 3.7% in July. As such, we expect the RBA to hold rates while looking for more signs that inflation is under control.

Caixin Services PMI to show slower expansion

Caixin will release its service PMI for China next Tuesday. Taking our cues from the official non-manufacturing PMI released earlier this week, we should see a slower expansion of the service sector with the PMI falling to around 53.8.

Trade data in the region remain weak

China’s imports and exports faced an unexpected plunge last month, with imports falling to 12.4% YoY and exports falling to 14.5% YoY. Both figures are lower than the consensus forecast. For the export side, weakness in global demand is likely to continue to weigh heavily. For imports, domestic demand has not shown any meaningful signs of improvement, so they are also likely to remain weak.

Taiwan’s trade data might show some signs that the semiconductor cycle is troughing. Taiwan’s exports fell less than expected last month and we expect this slight improvement to carry on. For the Philippines, trade data will also be reported with exports posting another month of modest gains, but the overall trade balance will still likely settle at -$3.7bn.

High energy prices to affect region’s CPI inflation

Taiwan’s CPI inflation rate has been below the target range of 2% for two consecutive months, with the July inflation rate at 1.88% and core inflation at 2.73%. August inflation is likely to remain subdued, helped by high ongoing base effects for energy and food prices.

Meanwhile, inflation in South Korea is facing upward pressure once again after falling to 2.3% last month. It is expected to rise to 2.6% in August with the main contributors being rises in transportation fees, pump prices and fresh food prices. The first two are associated with strong oil prices after recent supply cuts from OPEC+, while fresh food prices have been affected by Typhoon Khaun destroying agriculture yields.

Lastly, Philippine inflation could pick up to 5.0% YoY from 4.7% in July. The recent uptick in energy and rice prices could offset slower inflation for select food items.

Singapore retail sales to extend gains

The sustained increase in visitor arrivals to Singapore appears to be helping to support retail sales, in particular department store sales and services related to tourism activities. We expect retail sales to post a modest 2.0% YoY gain for the month.

Key events next week

Download

Download article

31 August 2023

Our view on next week’s key events This bundle contains 3 ArticlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more