Asia week ahead: Australian central bank likely to keep rates on hold

The Reserve Bank of Australia (RBA) is likely to keep rates untouched at 4.1%, while inflation reports from the region are likely to show moderating readings

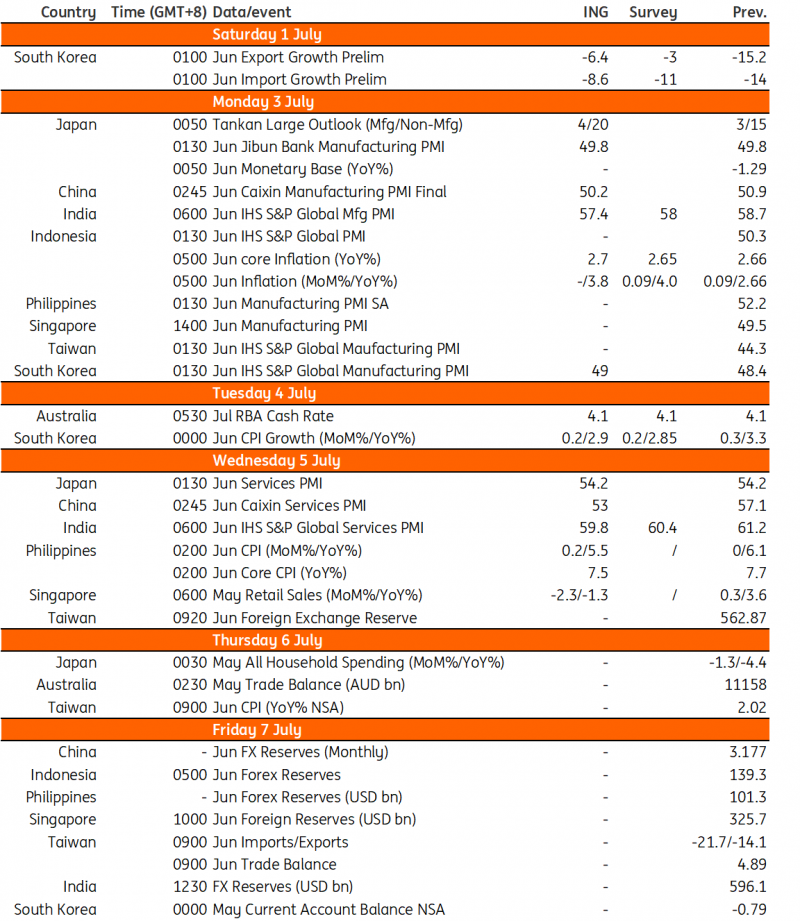

RBA likely to keep rates untouched at 4.1%

Following the surprisingly large fall in May headline CPI inflation to 5.6% year-on-year from 6.8% in April, there seems little prospect of the RBA hiking rates again following what, by its own admission, was a finely balanced decision in June. That hike only got over the line because of the large upward spike in April inflation, so it would seem extremely odd to hike again if inflation surprises on the downside.

We are keeping an open mind on one final hike this cycle, and the September meeting looks like the most likely candidate to us. July CPI will have to absorb a large electricity tariff spike of 20% YoY, or more by some estimates, and the base effects are less helpful over the third quarter too. But that will probably be it for the RBA, in our view.

China Caixin PMI numbers to show struggling sector

Caixin PMI data will take their cue from the official PMI numbers due out on 30 June. These are likely to show that the manufacturing sector is still struggling, but may also show service sector strength waning, as re-opening pent-up demand starts to normalise again.

India’s strong PMI reading points to strong growth

Both India’s manufacturing and service sector PMIs are running at extremely strong levels. The manufacturing sector, in particular, has shown an acceleration in recent months, but may now be due a slight correction lower. Not being very exposed to either China or the global semiconductor slowdown is helping India.

Korea trade and inflation data set for release

Exports in Korea are expected to contract again in June. But due to strong auto and vessels exports, the contraction (-6.4%) should be quite a bit lower than the previous month of -15.2% YoY. We think vessel exports should be strong this year due to the imminent delivery of pre-order ships, considering that the shipbuilding period is at least two-to-three years. But since this does not reflect the current global demand cycle, it is necessary to focus more on exports excluding ship data to understand global demand conditions better.

Meanwhile, we expect consumer inflation to decelerate quite sharply in June and reach the 2% range mainly due to the high base last year. The gains from utility fees should be partially offset by the decline in gasoline, fuel and rent prices.

Japan's Tankan survey to show economic recovery

Business survey data will be released in Japan next week. Both Tankan and PMI surveys will show that the country’s economy is on the path to recovery, led by solid service activity in particular.

Inflation to moderate further in Indonesia and the Philippines

Headline inflation is set to moderate further for both Indonesia and the Philippines. Inflation should remain within target in Indonesia, settling at 3.8%YoY, while core inflation could be flat at 2.7%YoY. Meanwhile, Philippine inflation should sustain its downtrend, with May inflation possibly slipping to 5.5%YoY from 6.1% previously. Slowing inflation should give both Bank Indonesia and the Bangko Sentral ng Pilipinas space to keep rates untouched in the near term.

Key events in Asia this week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

29 June 2023

Our view on next week’s key events This bundle contains 2 Articles