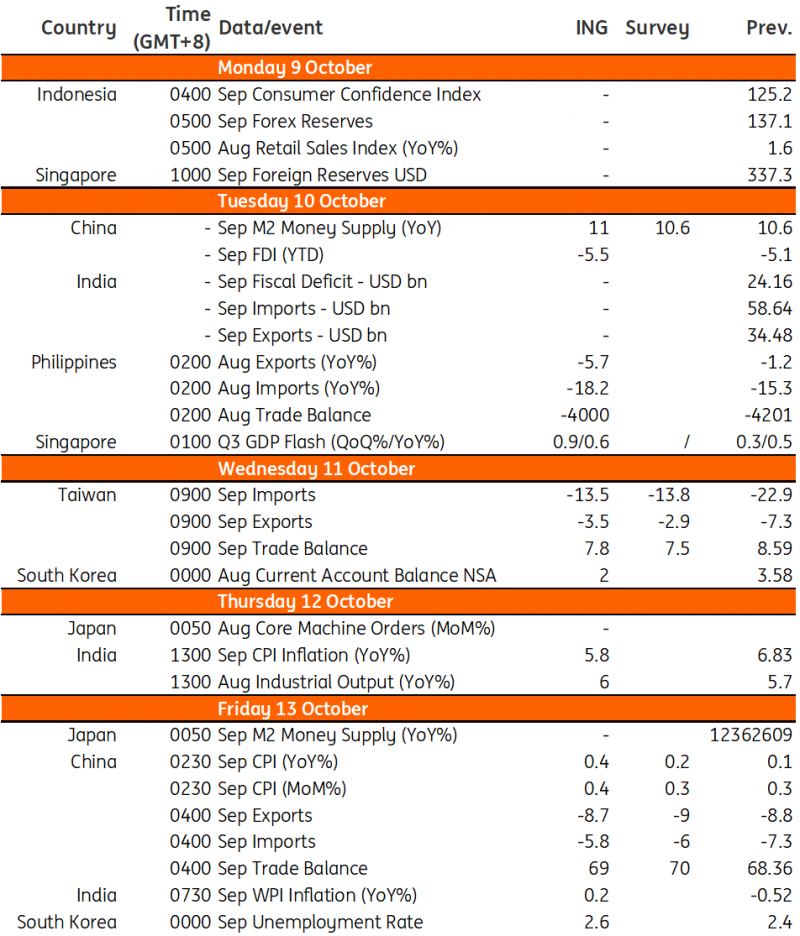

Asia week ahead: Regional inflation readings and an MAS decision

The coming week features inflation readings from China and India, plus a meeting for the Monetary Authority of Singapore (MAS), where policy settings are likely to remain untouched

China inflation in the positive territory

China’s CPI inflation has returned to positive territory last month after it briefly slipped to -0.3% year-on-year in July. We expect the inflation to edge slightly to 0.4% YoY as the recent data suggests that the government’s efforts to boost the economy have had some impact.

On top of that, surging oil prices are likely to increase transport and energy costs for the period.

India inflation to settle within RBI’s target range

With supply concerns easing for key vegetables like tomatoes and onions, prices for these important commodities should moderate. As food items account for the bulk of the overall inflation basket, this should help bring India’s inflation down to 5.8% YoY, just within the 2-6% target range set by the Reserve Bank of India.

MAS expected to keep setting untouched

The Monetary Authority of Singapore (MAS) is likely to retain its current policy setting next week. The MAS looks to balance slower growth alongside still elevated inflation and will opt to keep settings untouched. Growth has struggled as of late, with exports dragged down by soft global demand. Meanwhile, inflation has been on the downtrend but could flare back up given a renewed rise in global energy prices.

Singapore GDP expected to remain subdued

Singapore’s third-quarter GDP figures will be reported next week. We expect growth to settle at 0.6% YoY, rising 0.8% from the previous quarter. Retail sales were the lone bright spot for Singapore, managing to post modest growth for the quarter.

The return of visitors to Singapore could be one factor helping support retail sales. On the other hand, contracting industrial production and falling non-oil domestic exports will be the main elements pulling down growth.

Key events in Asia next week

Download

Download article

6 October 2023

Our view on next week’s key events This bundle contains 2 Articles"THINK Outside" is a collection of specially commissioned content from third-party sources, such as economic think-tanks and academic institutions, that ING deems reliable and from non-research departments within ING. ING Bank N.V. ("ING") uses these sources to expand the range of opinions you can find on the THINK website. Some of these sources are not the property of or managed by ING, and therefore ING cannot always guarantee the correctness, completeness, actuality and quality of such sources, nor the availability at any given time of the data and information provided, and ING cannot accept any liability in this respect, insofar as this is permissible pursuant to the applicable laws and regulations.

This publication does not necessarily reflect the ING house view. This publication has been prepared solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved.

ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam).