Asia week ahead: Rate meetings in Japan, Australia, Indonesia, Taiwan, Philippines

- 12 June, 07:09

- Asia week ahead Australia China

Japan, Australia, Indonesia, Taiwan and the Philippines will announce interest rate decisions. Key data releases include inflation updates from China and Japan

Asia Research highlights of the week

Our latest views on the major central banks

Tech and FX: short-term volatility may cloud long-term trend

Asian policy tightening ahead as FX and inflation risks build

Philippine rate hike still on track despite softer inflation print

China’s second-quarter slowdown underway amid soft consumption

China’s reflation trend continues to solidify|

Taiwan’s trade boom prompts another growth upgrade|

China trade outperforms amid tech boom and US rebound

Japan: BOJ to tighten and disclose JGB purchase plans

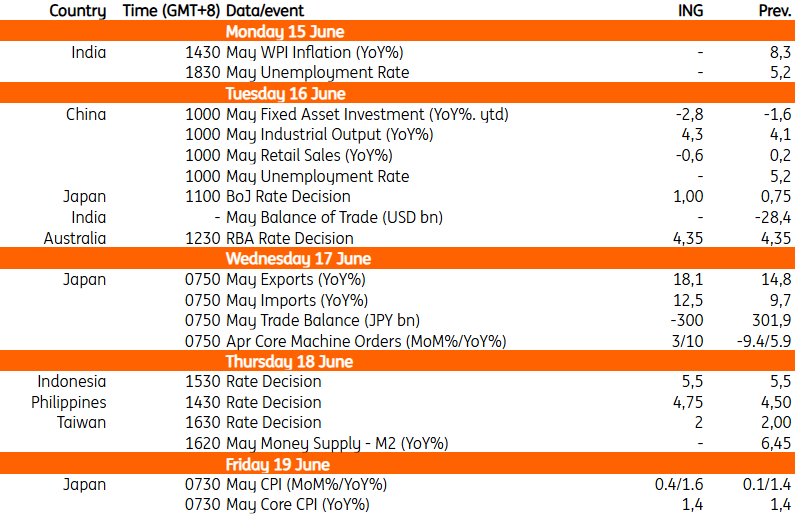

The main event will be the Bank of Japan (BoJ) policy decision on Tuesday. We expect the BoJ to raise its policy rate by 25 bp to 1.0%, in line with market consensus. The BoJ will also announce its latest Japanese government bond (JGB) purchase plan. It’s a close call, but we expect the BoJ to pause JGB tapering from next April, as market functioning has improved over the past year. A pause could help ease market concerns about further sharp rises in JGB yields. This would also reduce government concerns about higher market rates and allow the BoJ to focus more on policy-rate decisions.

Japan’s May consumer price index should remain subdued thanks to government measures, though price pressures are likely to broaden. Chip and car exports should be the main drivers of export growth in May, while higher energy prices are expected to sharply boost imports.

Australia: RBA to hold rates as downside risks increase

We expect the Reserve Bank of Australia to stay on hold on Tuesday, as recent inflation data surprised to the downside. Moreover, the RBA is signalling that policy is in restrictive territory, but not locked into a one‑way tightening path. A noticeable slowdown in growth at recent meetings and a clear upward drift in unemployment suggest the Bank is becoming more alert to downside risks.

Philippines: BSP to hike rates by 25bps amid higher inflation

Headline inflation in the Philippines eased as lower transport costs, driven by recent fuel price rollbacks, pulled the headline number down. Food inflation continues to drive overall price gains; it’s becoming increasingly broad‑based beyond rice. Risks to the inflation outlook remain firmly skewed to the upside. We maintain our forecast for CPI inflation to average 5.8% year-on-year in 2026, well above the 4% Bangko Sentral ng Pilipinas (BSP) target. In this environment, our base case for Thursday’s meeting is that a 25bp rate hike is highly likely.

Indonesia: BI to keep rates steady after off-cycle hike

Following the recent off-cycle rate hike, we expect Bank Indonesia (BI) to keep policy rates unchanged on Thursday. Instead, BI is likely to prioritise alternative measures to attract foreign capital inflows and stabilise the rupiah. This approach reflects a delicate balancing act, as the central bank seeks to support currency stability while mitigating downside risks to economic growth.

China: Continued economic slowdown expected

China releases its key domestic activity data on Tuesday. We expect further confirmation of a second-quarter slowdown underway. We’re likely to see further deterioration of retail sales and fixed asset investments in May to -0.6% YoY and -2.8% YoY ytd, respectively. We expect industrial production to fare better, growing 4.3% YoY, buoyed by external demand. The 70-city property prices will also be released on Tuesday. We will learn whether the recent trend of slower declines and price recovery in tier-1 cities continues.

Taiwan: CBC to hold, but may open door on future hikes

We expect the Central Bank of the Republic of China (CBC) to leave rates steady on Thursday. However, it will be important to monitor the CBC’s press conference to gauge whether there is any significant shift in tone suggesting a potential rate hike at future meetings. With inflation shooting above the 2% target in May and the prospect of inflation moving further above target in the next few months, we’ve pencilled in a rate hike in the third quarter.

Key events in Asia next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more