Asia week ahead: Policy meetings in China and the Philippines

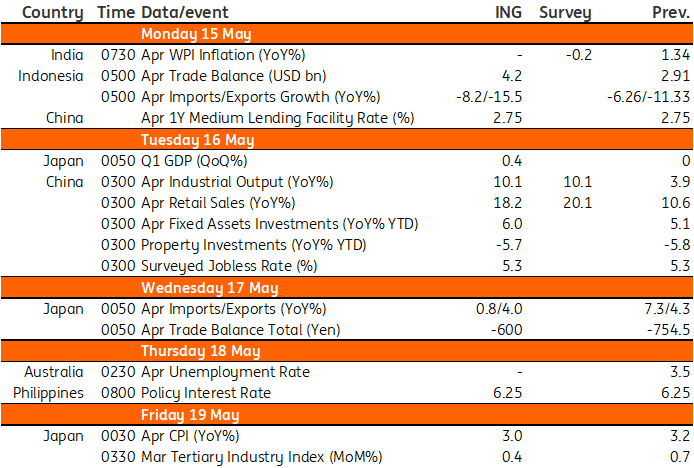

Next week’s data calendar features policy meetings from the People's Bank of China (PBoC) and Banko Sentral ng Pilipinas (BSP), wage and job data from Australia, plus growth and price data from Japan

Wage and job data to be released in Australia

Justifying the recent increase in the cash rate, Reserve Bank of Australia (RBA) Governor Philip Lowe noted that the central bank would continue to “…pay close attention to… the evolution of labour costs”, of which the main indicator is the quarterly wage price index. The next one of these is due out on 17 May. This has been rising very slowly. But with the RBA hiking in May, one wonders if it might have had advanced knowledge that this number is going to come in higher than consistent with its inflation target.

The run rate for this index on a quarterly basis has been about 0.8% quarter-on-quarter, and we would expect something similar this time. If so, that would lift the wage-price inflation rate to 3.5%. If we got a repeat of the third quarter of 2022 quarter-on-quarter result, then we could see the wage inflation rate rise as high as 3.8% year-on-year, and anything at this sort of level or above would probably set off alarm bells at the RBA.

Furthermore, April labour market data that is out on 18 May will add to the story, with the unemployment rate being a key focus. We are expecting a very slight increase to 3.6% from 3.5%, though the risk to this forecast is likely to be on the downside as labour force growth remains strong. The monthly employment change will likely see the very rapid rate of full-time jobs growth in recent months drop back, though this may be offset by a pick-up in part-time jobs, and so the overall total employment growth for April could remain at a buoyant 40,000.

Upcoming GDP and inflation data from Japan

Japan will release several data points next week. The highlight should be first-quarter GDP on Wednesday. We expect a mild improvement and GDP to grow at 0.4% QoQ seasonally adjusted. This is mainly driven by the services sector, while exports and manufacturing remained weak.

We are also expecting CPI and PPI inflation figures, which will confirm that the headline figures are continuing to cool due to falling commodity prices and the base effect. Core inflation however is expected to remain sticky and is likely to stay on the rise.

Activity data from China plus the PBoC meeting

The PBoC will decide whether to change the 1Y Medium Term Facility Rate (MLF) on 15 May. We expect no change at 2.75%. A rate cut would be perceived by the market that the economy was not on the path to recovery. However, the ongoing improvement in consumption, driven by internal tourism during the Golden Week holiday, suggests that recovery is happening. Moreover, the challenge from a weaker external sector cannot be addressed by a rate cut. It is possible that the central bank may add more liquidity to the money market via the MLF operation. But that should not lower the market interest rate significantly unless the scale of liquidity injection is large, which is not our expectation.

Meanwhile, the Statistics Bureau will also release industrial production, retail sales, fixed assets investments and surveyed jobless rate data on 16 May. Interpreting this set of data requires attention to the low base effect last year. The data should show more than 10%YoY growth for industrial production and more than 18%YoY for retail sales, but those should be moderate month-on-month growth. Industrial production reflects the existing picture of the economy, a recovery of the domestic market but a slower external market. Retail sales strength for April should only be moderate as spenders planned leisure trips in May and saved for those trips in April. Our focus for this set of data is fixed assets investments (FAI). This should give us more hints on the speed of the government implementing infrastructure investments. We expect slight improvement on a monthly basis.

BSP set to pause next week

The Philippines' central bank will hold a policy meeting next week with market participants split on whether it will keep its policy rate unchanged at 6.25%. Recent comments from BSP Governor Felipe Medalla suggest that he will end the bank's aggressive tightening cycle now that inflation has shown clear signs of heading back toward the 2-4% inflation target. Medalla also hinted at a potential reduction of the reserve requirement ratio in the coming months. We expect BSP to pause next week with inflation on the downtrend and signal an eventual rate cut by the end of the third quarter should inflation trends persist.

Key events in Asia next week

All time refers to Singapore time

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

11 May 2023

Our view on next week’s key events This bundle contains 3 Articles