Asia week ahead: Inflation reports and the RBA meeting on the calendar

Several Asian economies report inflation next week while the Reserve Bank of Australia meets to discuss policy

Inflation reports from regional players

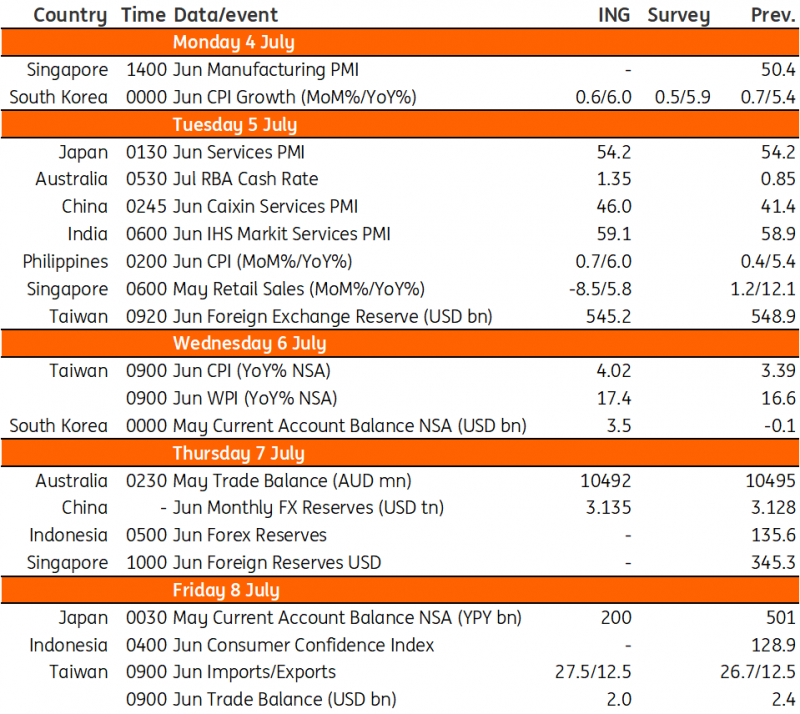

The coming week features several inflation gauges from the region with price pressures generally trending higher. Taiwan’s inflation is expected to rise due to higher energy prices and a low base effect from last year.

Philippine inflation will likewise head higher, accelerating to 6.0% from 5.4% year-on-year last May. Pricier food, transport and utilities are all likely to drive up headline inflation, which should pressure the central bank to double down on rate hikes at the August meeting.

Meanwhile, Korea’s consumer price index for June is also moving higher, likely hitting 6.0% YoY with gasoline and manufactured food prices up sharply. If inflation settles higher than 6.0% in June, the Bank of Korea will take a big step in terms of tightening at the July meeting.

RBA meeting

It is pretty clear that despite being a little slow to pick up the inflation threat, the RBA is now fully on board with its determination to bring inflation down. Rates are going up. The only question is, how fast? Well, we haven’t had any particularly helpful data since the last meeting. We don’t for example have any further inflation data to react to, though Melbourne Institute inflation expectations did move sharply higher. The lack of new hard data is probably why Governor Philip Lowe ruled out a 75bp hike when asked earlier this month. The choice is therefore between 25bp and 50bp.

What may tip the balance in favour of the bigger hike is how far the RBA needs to go in order to get rates even to neutral. That suggests not hanging about. They can step up the pace if needed once they have sight of the 2Q inflation print. So it's 50bp now, and 75bp in September, if the inflation data paints an ugly enough picture. If not, they can ease back a bit and revert to 25bp or 50bp hikes.

China GIR and services PMI

Over in China, Caixin services PMI should settle below 50, suggesting overall activity is in contraction. However, with lockdowns easing gradually, the contraction may show a slight improvement from the previous month.

An additional data report from China in the coming week is the level of foreign reserves, with GIR likely increasing due to capital inflows to the stock market since mid-June.

And the rest..

Meanwhile, Taiwan trade data is also out in the coming days with both imports and exports expected to grow around 20% YoY from demand for semiconductors. Exports may grow slower than imports however with the trade surplus narrowing from the previous month.

Lastly, Singapore retail sales likely expanded but at a more moderate pace, slowing to 8.5% from 12.1% previously as higher prices sap some spending momentum.

Asia Economic Calendar

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

30 June 2022

Our view on next week’s key events This bundle contains 3 Articles