Asia week ahead: Inflation data from Australia plus growth numbers from India

Next week’s calendar features inflation data from Australia and growth from India. Meanwhile, industrial production data will be released in Japan and Korea

Inflation to rise in Australia

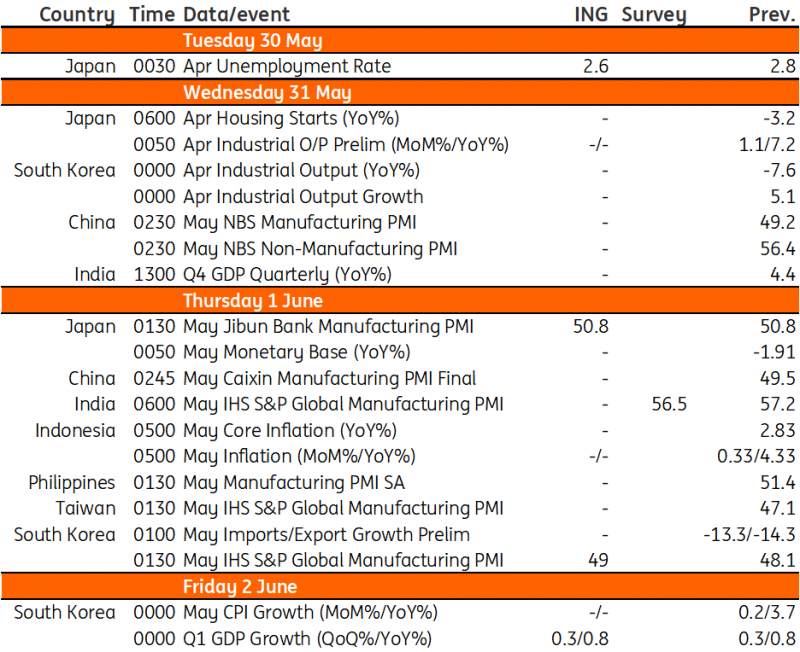

Australia’s April inflation will likely increase from the previous month. This is partly a base effect-driven phenomenon, though not entirely. And we estimate that food prices rose at a similar 0.4% month-on-month pace in April, with larger increases for alcohol and tobacco, and motor fuel, which should offset any further reduction in housing-related inflation over the month. A 0.5% MoM inflation print will deliver a year-on-year inflation rate of 6.6% for April, up from 6.3% in March. We expect inflation will drop back to 6.2% in May, but that still would leave it barely any lower than it is now, creating a headache for the Reserve Bank of Australia.

Looking beyond India’s slowing growth

1Q23 GDP data will come in at about 3.4% YoY, down from 4.4% in 4Q22. This may seem low, but the year-on-year numbers are all still reflecting earlier lockdown and reopening distortions. The 3.4% in the first quarter will still leave the economy on track to deliver growth for the full year of about 6% if our subsequent forecasts turn out to be correct. High-frequency data for India continues to point to relatively robust growth, though there has been a slight slowdown from 2022 growth rates.

Signs of recovery in Japan

April industrial production is expected to rise for the second consecutive month on the back of a solid domestically driven recovery. Auto production will also play a major role in the improvement of IP numbers. Also, ahead of golden week, the jobless rate should have come down a bit with solid service hiring.

Industrial production to fall in Korea

Industrial production in Korea is expected to fall again after a temporary rise in March, as suggested by the weak April export numbers. Although manufacturing and construction activity is expected to be weak, we expect service activity to stay firm as consumer sentiment continues to recover.

The early May exports data has already pointed to a sluggish export trend, which is set to continue through May. We are concerned about the fact that exports to developed markets, especially to the US, are softening. The manufacturing PMI will likely rebound only modestly on the back of an improvement in the global supply chain and China’s reopening, but still stay below the neutral level.

Inflation is expected to decelerate to 3.5% YoY in May despite the recent hike in utility prices as base effects bring down the headline rate.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

26 May 2023

Our view on next week’s key events This bundle contains 2 Articles