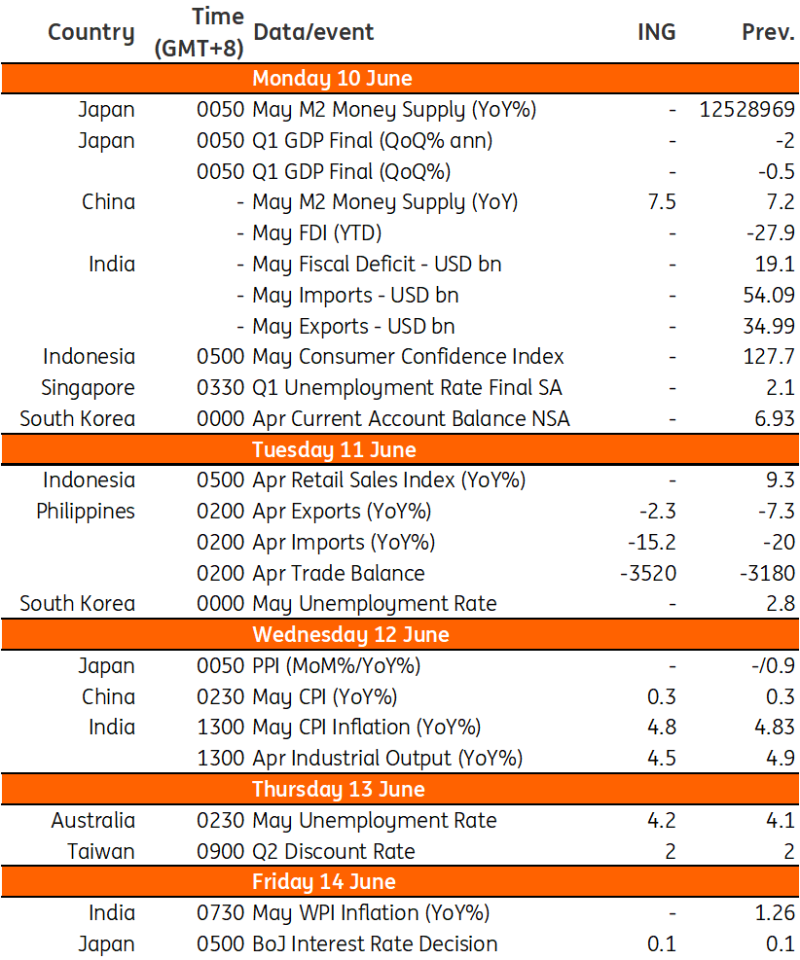

Asia week ahead: India and China to report inflation while the BoJ decides on policy

Next week features inflation reports from China and India plus central bank meetings in Japan and Taiwan. Also on the data calendar is Australia’s unemployment, which could see a slight uptick

India’s inflation to stay flat

As well as following the fallout from the recent Indian elections, where the next few weeks could see horse-trading over important ministerial jobs, we'll also get May inflation data. With no big swings in any of the important food categories in May, it looks quite likely that the May CPI index will rise by a modest 0.5% month-on-month, resulting in an annual inflation rate of around 4.8%, almost unchanged from April. This should have no immediate consequence for the Reserve Bank of India, whose next policy meeting is 8 August.

China inflation likely stable

China will publish its May CPI and PPI inflation numbers on Wednesday. We are expecting headline CPI inflation to remain broadly stable around 0.3% year-on-year. An uptick in the purchasing price subindex of the PMI data indicates that PPI will move a bit higher but will likely remain in deflation. While inflation is likely to remain low in the second quarter, it should begin to pick up in the second half of the year.

Additionally, China’s credit data will be released sometime in the coming week. After very weak data in April, we expect to see a rebound in May amid the supportive policy rollout. Recent indicators point to real interest rates remaining too high for current economic conditions.

BoJ to wait for more data before hiking again

Next week’s highlight should be the Bank of Japan’s policy decision on Friday. Recent data has been supportive of the central bank's policy normalisation. The reacceleration in inflation, the recovery in retail sales and labour earnings all support the view that the BoJ could raise rates earlier than the market consensus of October. We continue to believe that it will wait for a more meaningful pick-up in labour income and private consumption next month, which will lead to a 15 bp hike at the July meeting.

When it comes to the JGB purchase programme, the BoJ may reduce the purchase amount from around six trillion JPY per month currently if the UST continues to trend lower. But even if this is the case, we suspect that the central bank will not set a fixed amount and rather adjust it by adding more flexibility to the purchase.

Australia’s jobs numbers out next week

In the absence of any inflation data this week, the main market-moving release for the week ahead in Australia will be the May labour report. Some of April’s part-time employment strength will likely convert to full-time jobs in May, though not on a one-for-one basis, and we may also see part-time job growth mean revert to a lower level. That could result in a lower increase of only 20,000 new jobs in May. We think that an increase in unemployment of around 25,000 in May, coupled with about the same increase in the labour force, will result in a slight uptick in the unemployment rate from 4.1% to 4.2%.

Taiwan’s central bank expected to hold

Taiwan’s Central Bank of China will set its benchmark rate on Thursday. We are expecting no change in the rate at this meeting. Though inflation could trend a little higher in the coming several months, it is unlikely to rise fast enough to cause significant pressure on the CBC to further hike rates. We expect the next move to be in the direction of a cut, but this is likely to come after the US kicks off its rate cutting cycle.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article