Asia week ahead: Flurry of data from Japan and Korea

Next week's data calendar for Asia features several reports from Japan and Korea. Meanwhile, we will also get inflation data from Singapore and Australia

Inflation in Australia to accelerate?

Next week Australia will release its CPI data and we should see a bounceback in consumer prices. Based on our data, we expect to see a moderate increase in food, alcohol and tobacco prices last month. Rising oil prices add to the mix. The only good news is probably on holidays, where we expect a dip in flight costs and hotel prices. Overall, we expect inflation to rise from 4.9% to 5.2% year-on-year.

Caxin China PMI

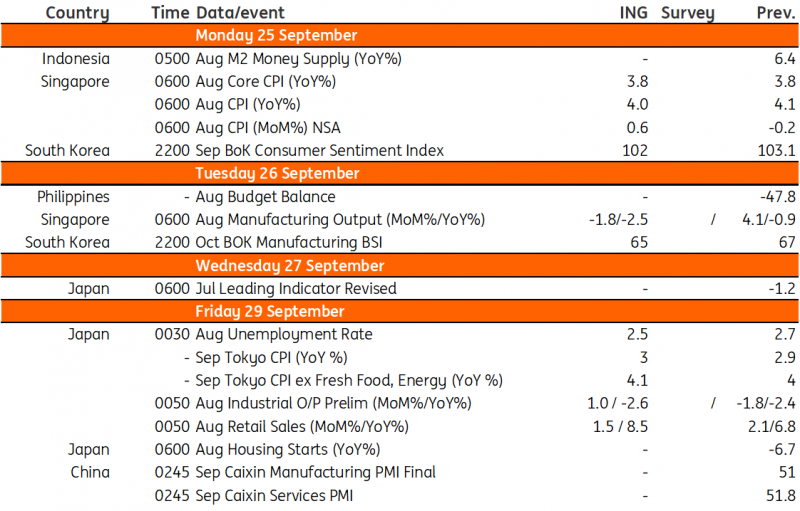

The Caixin Manufacturing PMI for China beat expectations last month and came in at 51.0 – just above the threshold that indicates expansion rather than contraction. This was due to an upturn in overall sales despite a further drop in business abroad. With no concrete fiscal stimulus boosting the economy and the end of the summer holidays, but some slightly better indications from the latest month’s data deluge, it is likely that this number will remain close to, or perhaps creep a little higher from last month’s figure.

Flurry of data out from Japan

In Japan, we think solid consumption and service activity will likely support inflation staying above the 3% range. We believe that core inflation excluding fresh food and energy is expected to accelerate further in September with private service prices rising.

Meanwhile, thanks to strong activity in services, the jobless rate is expected to edge down in August. Industrial production in Japan will also likely rebound from the previous month’s decline mainly due to a pick-up in motor vehicle production.

Sentiment in Korea likely on the downtrend

We think both consumer and business sentiment indices in Korea could deteriorate. Business confidence should weaken on the back of sluggish exports and growing uncertainty over the near-term economic outlook. For consumers, weak domestic equity performance and the recent tightening of mortgage measures might have hurt sentiment.

Singapore inflation to edge lower

Singapore reports August inflation next week. We expect headline inflation to dip to 3.9% year-on-year, down from 4.1%YoY from the previous month. Favourable base effects and softer growth momentum will likely translate to a dip in CPI inflation. Core inflation will likely be flat at 3.8%YoY.

Meanwhile, industrial production will likely still be in the red. We could see the tenth consecutive month of contraction for industrial production, tracking the sustained weakness of non-oil domestic exports (NODX). NODX recently posted another month of contraction as global trade grinds lower. Industrial production should stay challenged for as long as NODX is in contraction, with weaker industrial activity seen to weigh on GDP growth.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

21 September 2023

Our view on next week’s key events This bundle contains 3 Articles