Asia Week Ahead: China’s Two Sessions meeting and Australian GDP numbers out next week

The coming week features China's Two Sessions meeting while also featuring GDP from Australia and South Korea

China to hold its Two Sessions meetings

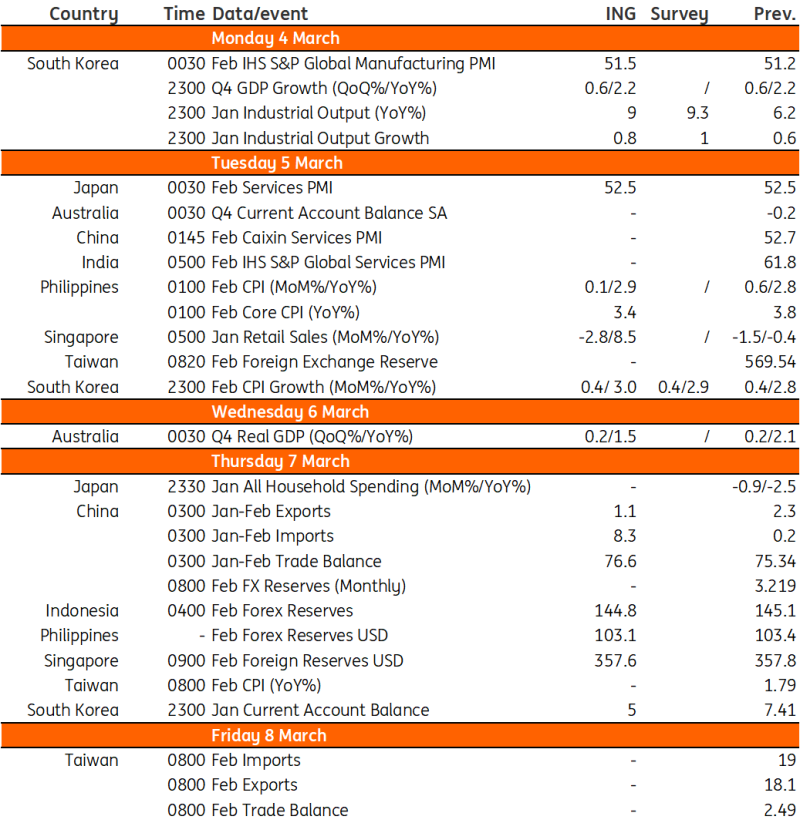

The government will hold its annual Two Sessions meetings next week. The key thing to watch will be the government work report on 5 March, where the annual economic targets will be given, as well as the overall policy direction for the year.

We expect the growth target to be maintained at around 5% and for a more supportive fiscal policy stance to be signalled via a fiscal deficit to GDP target of around 3.5%. Markets will also watch closely to see if there is any adjustment to the “proactive fiscal policy” and “prudent monetary policy” terms which have been in place for the past few years.

In terms of data, we will also have China’s trade and inflation numbers out next week. We expect a strong rebound in imports but relatively slower export growth in January-February. We also expect inflation to trend higher in February. High-frequency data has shown that food prices rose during the Lunar New Year holiday, which should help push CPI inflation back to positive levels.

Australia GDP out next week

We have a 0.2% quarter-on-quarter forecast for 4Q23 GDP, but we have just had a positive private capex figure for the quarter so the risks to this forecast are already skewed to the upside. The contribution to GDP from net exports is released on 5 March, the day before the GDP release, which may also support an upgrade to the forecast, subject to assumptions about inventories, which we think will unwind this quarter after they lifted growth in 3Q23.

South Korea activity data

Manufacturing activity in South Korea should have improved further in January, driven by robust demand for chips and cars. The positive PMI result is expected to boost confidence that manufacturing will continue to drive overall GDP growth this quarter.

Meanwhile, consumer prices are expected to heat up again and temporarily rise to 3% year-on-year. The Lunar New Year holiday should have pushed up fresh food and gasoline prices.

There is no Bank of Korea meeting in March, but sticky inflation should remain the central bank's main concern for the time being.

Tokyo inflation and services data from Japan

Tokyo CPI inflation is expected to rebound sharply, distorted by last year’s government energy support programme. Stripping out base effects, fresh food and energy prices are likely to be the main drivers.

Meanwhile, we expect the services PMI to soften a bit as service activity seems to have lost momentum recently, however, it should remain well above the key 50 threshold. We expect labour cash earnings to improve on the back of a meaningful rise in bonus payments, while contract earnings should rise steadily by about 2.0%.

Taiwan trade could rebound

Inflation and trade data will be published next week. Inflation is likely to rebound in February to 2.7% YoY reflecting the New Year effect, but this is unlikely to affect the monetary policy trajectory as inflation should moderate in future months.

February trade data should continue to look relatively strong on a year-on-year basis given the recovery of export orders to positive levels, and a very weak base from 2023, but will likely moderate from January.

Philippines inflation to remain within target

February inflation is set for release next week and we expect headline inflation to remain well within the central bank’s inflation target. Favourable base effects as well as slower inflation for most food items outside rice will likely keep headline inflation below 3% YoY.

Bangko Sentral ng Pilipinas (BSP) is expected to look past this recent drop in inflation although Governor Eli Remolona has hinted at potential easing in the latter half of the year.

Key events in Asia next week

Download

Download article

29 February 2024

Our view on next week’s key events This bundle contains 3 Articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more