Asia week ahead: Australia reports inflation while China releases latest PMI readings

The week ahead features Australia’s inflation and China’s PMI. Meanwhile, India’s GDP is due for release, alongside industrial production reports from Japan and South Korea

China's PMI and industrial profit reports

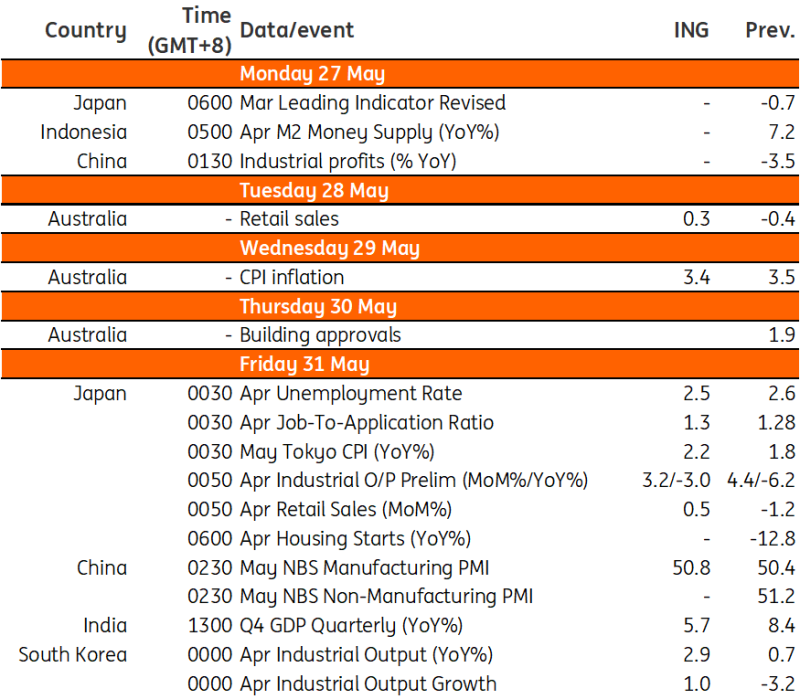

Industrial data will be the focus of the upcoming week in China, starting off with April industrial profits data next Monday. After several consecutive months of stronger-than-expected industrial production, a further decline in profits could be a sign of price competition – though markets will be hoping to see a rebound in profits to indicate that the year-on-year contraction in March’s numbers was a blip.

Later in the week on Friday, China’s May PMI data will be released. Here, we are expecting an uptick in May manufacturing PMI to around 50.8, which would mark the third consecutive month of expansion.

Australia’s inflation could see modest dip

April CPI inflation may decline slightly from the 3.5% year-on-year rate recorded for March in Australia. But any decline is likely to be modest (ING: 3.4%, consensus: 3.3%). Retail gasoline prices peaked in April and will likely add to headline inflation, even if the core rate is better behaved. Any decline is likely to owe more to last year’s outsized 0.7% month-on-month increase than any genuine moderation in the Australian run-rate, and annualised inflation is likely to remain inconsistent with the Reserve Bank of Australia's inflation target.

One more bad inflation report from Australia, and we will consider removing the final cut we have pencilled in by the RBA in the fourth quarter of this year. Two more, and we may consider adding a rate hike.

India’s GDP and PMI out next week

First quarter GDP could slow sharply from the 8.4% YoY rate recorded in the fourth quarter of last year in India. The consensus expects the rate to come down to just 6.4% YoY (ING: 5.7%). India’s GDP contains some erratic historical quarters of growth, and these are driving a lot of volatility in the YoY GDP numbers, while the quarterly sequential figures are also highly seasonal. The PMI data is probably providing a more helpful clue about economic strength, and both manufacturing and service PMIs are still giving very strong readings.

Data deluge from Japan

Monthly activity data should show a normalisation of activity in Japan, which has been distorted by car production. We expect industrial production to rise for a second month on the back of strong gains in the production of chips, machinery and vehicles. Retail sales are also expected to rebound with better sales on consumer goods, but car sales could turn negative after a big surge in March.

With solid demand from manufacturing sector, the labour market should remain tight. Meanwhile, the Tokyo consumer price is expected to reaccelerate after a sudden drop led by the expansion of the free education programme in April.

Korea's industrial production data to show moderation

Korea's industrial production growth should moderate after a big surge in March. April export data suggests that chip production is likely to remain solid, but other heavy industry production could weigh on overall growth. Various survey data suggested weak retail sales and investment activity due to the heavier debt service burden for households and businesses.

Hong Kong releases report on trade

Hong Kong publishes its trade data on Monday, where a favourable base effect should lead to faster YoY growth for both exports and imports despite pressure on re-exports. Hong Kong also releases its retail sales numbers on Friday. Retail sales have been in a slump as the economy faces challenges of reduced per capita spending from tourists, as well as a decline in local consumption due to heavy weekend cross-border traffic.

Measures to boost tourism and local consumption have been met with limited enthusiasm, indicating that a continued YoY contraction in retail sales is likely to continue.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article