Asia week ahead: China inflation and trade data

China's producer and consumer price updates next week may continue to fuel concern about deflation in the world's second-biggest economy. Elsewhere, look for second-quarter GDP releases from Indonesia and the Philippines

China and Taiwan to release trade data and CPI

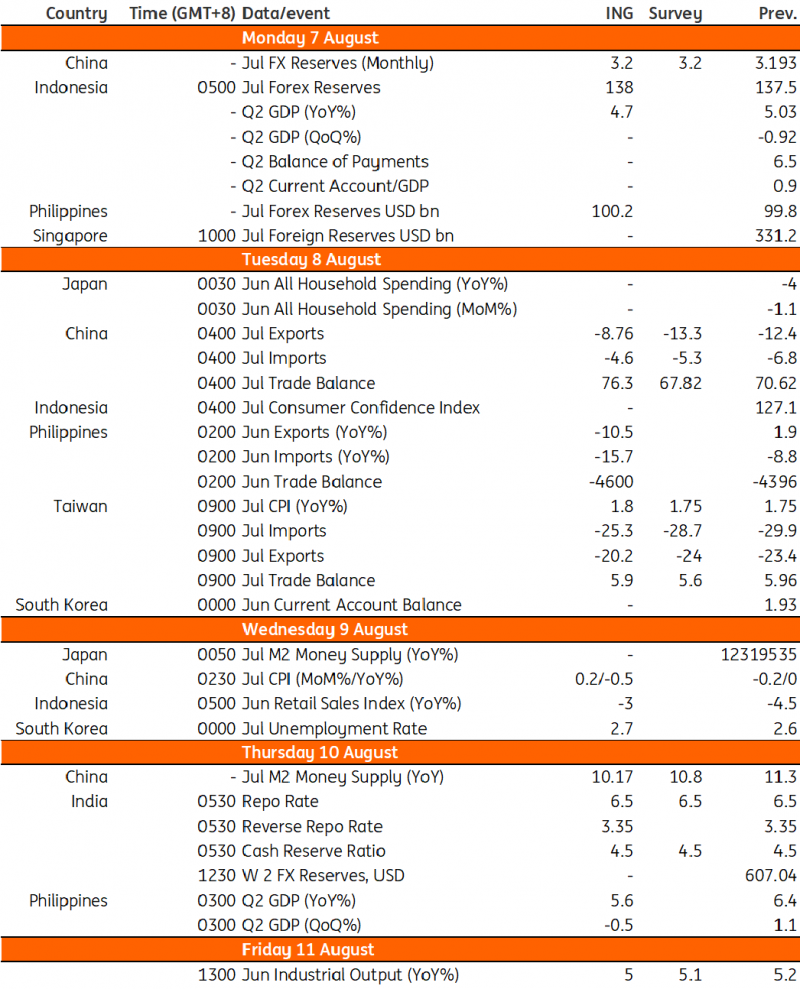

We expect China’s July CPI to be almost unchanged as recently adopted measures by the government have yet to take full effect. While the Politburo reiterated support for the economy, we await further details on the said measures.

Meanwhile, we expect PPI inflation to remain in negative territory. Despite the recent increase in oil prices, the mining and manufacturing prices are likely to drop further as evidenced by data releases this week (Caixin and property prices).

For Taiwan, July CPI inflation is expected to rise only slightly as the price of household amenities remain high amidst robust demand with consumer confidence up for a third consecutive month. The consumer confidence index rose 1.73 points from June to 68.39 points in July, the highest level since last year April.

RBI to extend pause

Food prices are still climbing in India despite government’s effort to keep price increases under control. Tomato prices in July recently spiked due to seasonal factors compounded by the early arrival of monsoon rains. The government announced an export ban on non-basmati rice, resulting in a further tightening of global supply for grain. Given the lagged impact of the ban, headline inflation could still exceed RBI’s target range of 2-6%.

This development however is unlikely to prompt a rate hike by the RBI as food inflation is expected to recede in the coming months.

Indonesia and Philippines to experience moderate growth in 2Q

Next week features 2Q GDP reports from Indonesia and the Philippines. Growth is expected to slow slightly in 2Q for both economies as base effects fade and higher inflation caps purchasing power. Meanwhile, tight financial market conditions are also expected to have weighed on investment activities as bank lending slowed. Despite the slowdown, Indonesia and the Philippines are expected to post respectable year-over-year expansion with Indonesia set to grow by 4.7%YoY while the Philippine economy likely grew by 5.6%YoY.

Trade data to show export in the region struggling amidst weak global demand

Several regional economies will be reporting trade data in the coming week. China and Taiwan will release trade figures that will likely show another period of contraction for both exports and imports. Soft electronic exports due to weak global demand should continue to weigh on exports, which in turn would cap the outlook for the manufacturing sectors of both China and Taiwan.

For the Philippines, June data will showcase both exports and imports likely in contraction given prospects for slowing global trade. Exports, which posted a surprise expansion in May, might revert to a contraction as demand for the mainstay export item, electronics, remains soft. Meanwhile, imports will continue to contract as global commodity prices normalize from the peaks experienced in 2022. All in all, the overall trade balance will likely stay in deficit with the shortfall pegged at roughly $4.5bn for the month.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

3 August 2023

Our view on next week’s key events This bundle contains 3 Articles