Asia week ahead: GDP figures, unemployment data and a Bank Indonesia decision

Next week features China's usual data deluge plus GDP, India's trade data and Australia's unemployment rate. Meanwhile, Japan reports CPI inflation and Bank Indonesia decides on policy

China data deluge plus latest GDP report

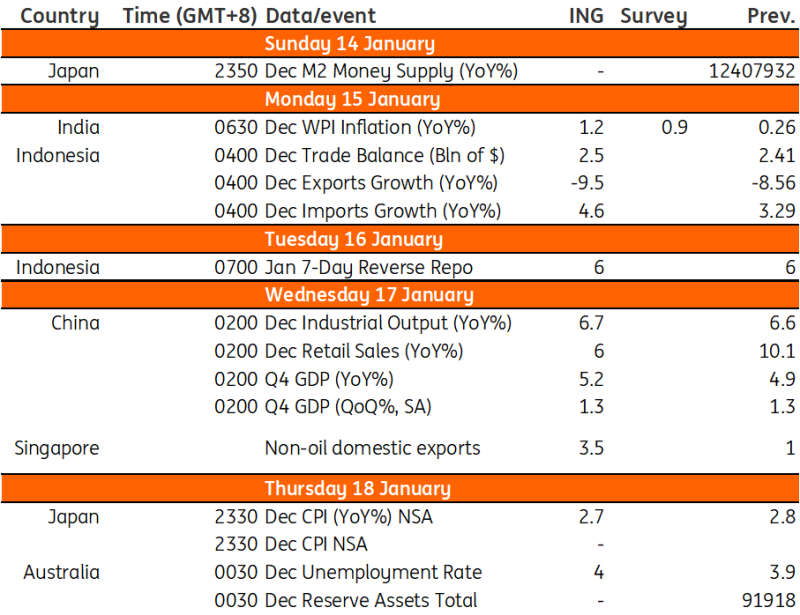

The monthly deluge is accompanied by GDP data for December and the fourth quarter of 2023 this month. We believe that the seasonally adjusted quarter-on-quarter growth rate was similar in the fourth quarter to the third last year, at about 1.3%. We think that this will result in a slight uptick in GDP growth to 5.2% year-on-year in the fourth quarter, and also 5.2% for the full-year figure – slightly in excess of the government’s 5.0% target. Box ticked.

For the rest of the data, we expect no improvement in any of the real estate-related data, though it will be interesting to see whether any of the recent increases in lending volumes of the MLF have any impact at all on infrastructure spending. We may see some very small further improvements in manufacturing and industrial production growth.

The key area to look out for remains the retail spending figures, which have been a pocket of relative resilience – although they have been punching a little bit above their longer-run trend growth in recent months and may not be able to sustain this for long.

Unemployment figures from Australia

While the market seems to have decided that the Reserve Bank of Australia (RBA) has finished hiking and were given an encouraging nod by the recent inflation data, the fact is that monthly inflation increases are not yet low enough for the central bank to hit its inflation target on a 12-month timeframe, and it will need to slow further. For that to look more probable, it would certainly help if indicators such as employment growth slowed.

In November, employment surged, and most of the jobs that were created were full-time. Both the strength of the full-time numbers and the weakness of the part-time figures were at odds with their recent trends. We would not be surprised to see a reversal with about 30,000 part-time jobs, but a dip to only 10,000 full-time jobs for a full employment change of +40,000. Unemployment may push up by about 20,000, and though this will remain slower than trend labour force growth, we may see the unemployment rate push up to 4.0%.

India's trade report

Trade data for December is not likely to diverge substantially from the November figures, which delivered a trade deficit of USD 20.6bn. With the Reserve Bank of India de-facto pegging the INR, this is unlikely to have a material impact on markets.

Japan inflation likely to moderate, core machinery orders to rise

Japan's CPI inflation is expected to decelerate to 2.7% YoY in December from 2.9% YoY in November, with falling utility prices and other energy prices weighing on the overall number. Service sector prices, however, will likely rise on the back of high demand in travel related items such as accommodations and eating out.

Meanwhile, core machinery orders should advance in November, supported by solid vehicle demand and recent recovery of semiconductor sector.

Bank Indonesia to extend their pause

Bank Indonesia (BI) is likely to extend its pause into 2024, with Governor Perry Warjiyo wary over a potential flare up in food inflation. Inflation has been relatively stable, but a looming El Nino episode and an expected acceleration in domestic activity ahead of the national elections in February could stoke price pressures in the near term. Concern over inflation should keep BI on hold, with the central bank also attempting to support the IDR, which is down 0.58% early in 2024.

Singapore NODX to post modest rise again

Singapore’s non-oil domestic exports (NODX) could post another modest expansion in December after recently snapping a string of negative growth for 13 months. A favorable base and a recent pickup in select electronics shipments likely supported NODX in December 2023. We can expect this trend to extend into early 2024.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

11 January 2024

Our view on next week’s key events This bundle contains 2 Articles