Asia week ahead: China data and central bank decisions in focus

Next week features several reports out of China, regional trade data, and central bank decisions

China monthly activity data and PBoC in focus

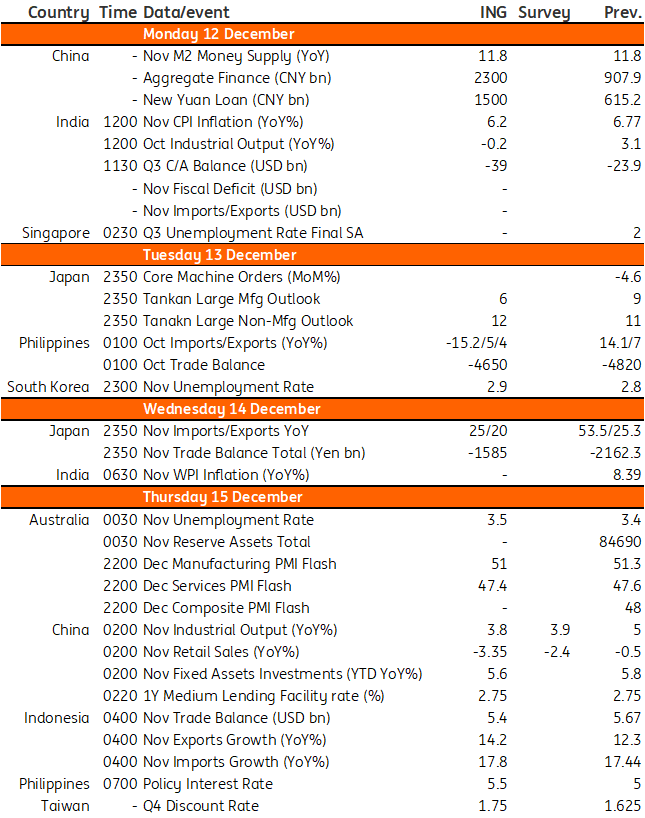

Data reports from China, including industrial production, retail sales and fixed asset investment, are scheduled to be released on 15 December. Industrial production is expected to grow, but at a slower pace, while retail sales look likely to continue to contract. Sluggish property investment will also likely drag down fixed asset investment. The government recently announced the easing of Covid-19 measures, but consumption is not anticipated to pick up immediately. Meanwhile, we expect the People's Bank of China (PBoC) to keep its 1Y Medium-Term Lending Facility Rate at 2.75% as this week's Politburo meeting suggested that there would be no further general easing of monetary policy.

Central bank watch: keeping up with the Fed

The PBoC's likely inaction is the outlier in Asia next week, as other Asian central banks will probably follow the US Federal Reserve's policy direction, though the pace of rate hikes will vary from country to country as well as how much further tightening will occur next year.

We believe that Taiwan's central bank will deliver a 12.5bp increase on Thursday to partially keep pace with the Fed's hikes, and the after-meeting statement will be important to assess whether the central bank will hike further in the first quarter of next year or not.

Bangko Sentral ng Pilipinas (BSP) governor Felipe Medalla indicated that he would be on par with the Fed in terms of policy. With the market expecting a 50bp rise from the Federal Open Market Committee (FOMC), the BSP is also expected to hike by 50bp. Inflation remains elevated (8.0%YoY), so we expect the BSP to also retain its hawkish stance next year.

Meanwhile, the Bank of Korea (BoK) will release its November meeting minutes on Tuesday. The decision of a 25bp increase at the last meeting was unanimous, but it is still worth watching how board members have changed their views on inflation and terminal rates. We think that given tight liquidity conditions in credit markets and rapid deterioration in exports and manufacturing activity, an additional 25bp hike in February may be the final action for the BoK's current tightening cycle.

Trade data from Japan, Indonesia, and the Philippines

Next week we also get trade reports out from Japan, Indonesia and the Philippines.

Japan and Indonesia will likely post double-digit growth in both exports and imports. In the case of Japan, the trade deficit is expected to decrease as import growth decelerates sharply due to stable energy prices and the quite strong recent depreciation of the Japanese yen (before the latest moves). In Indonesia, the overall trade surplus may narrow with export growth moderating.

Meanwhile, the Philippines' exports could slip back into contraction, given the sector’s reliance on electronics exports. This will probably result in the Philippine trade deficit remaining wide, which should put added pressure on the peso to close out the year.

Other data releases next week

Japan's Tankan Survey will suggest that business sentiment for manufacturing is worsening, while optimism about non-manufacturing is likely to lead Japan's economy next year.

In Australia, the labour market report for November will be worth a look. But with the Reserve Bank of Australia seemingly more concerned with over-tightening than under-tightening, it probably won't have too much impact on markets, though it could in time be a factor to consider at what stage the RBA can halt its 25bp per month tightening. Right now, we think this will come with the cash rate at 3.6% in the first quarter of next year, though there is a large degree of uncertainty attached to that forecast.

India's inflation data will be important for judging where the Reserve Bank of India (RBI) calls the peak for rates in this tightening cycle following the 35bp hike to the repo rate on 7 December (now stands at 6.25%). And we think we will continue to see inflation falling, with even some downside risk to the consensus 6.36% forecast (ING forecast for November: 6.2%; October inflation: 6.8%). Lower food prices, especially vegetables, and stable energy/gasoline prices should see India's headline inflation index dropping to a level roughly in line with policy interest rates. It is an argument for the RBI to hike by only 25bp at its first 2023 meeting.

Korea's labour market report will hint at whether the current slump in manufacturing and exports is beginning to have a negative impact on the labour market. We expect some weakness in manufacturing and construction jobs, but for the unemployment rate to remain below 3%.

Asia Economic Calendar

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

8 December 2022

Our view on next week’s key events This bundle contains 3 Articles