Asia week ahead: Australia’s inflation plus regional industrial output

Regional industrial production to show mixed trends while Australia's inflation could decline further

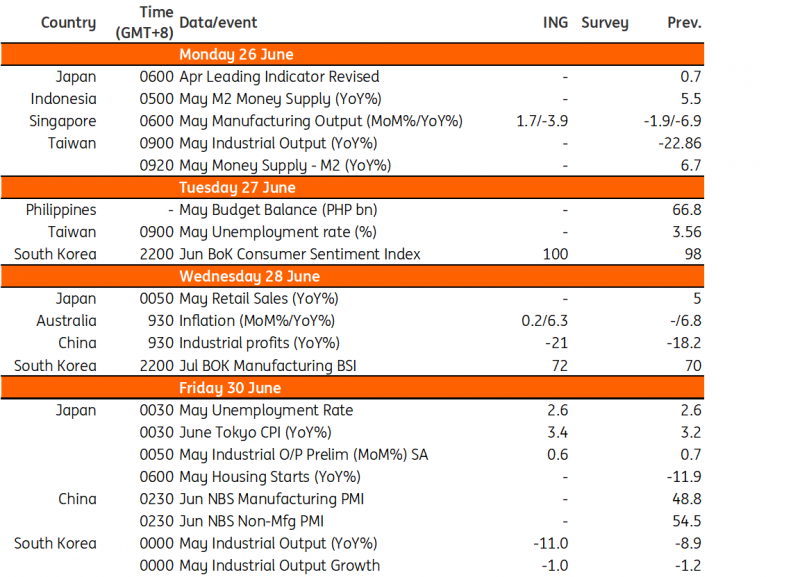

Inflation in Australia to dip further

May inflation should show a further decline after it jumped in April. We estimate the CPI index rose 0.2% month-on-month, which will result in a fall in annual inflation from 6.8% to 6.3%. Following the guidance from the Reserve Bank of Australia's (RBA) minutes from June, where the decision to hike was a very finely balanced one, this improvement in inflation suggests that July could well provide the bank with a chance to pause.

Korean output likely to slip but sentiment to rebound

Industrial production is likely to fall in May mainly due to a reduction in semiconductor production. Two major chipmakers announced plans to cut production in early 2023, a process which generally takes about six months to hit target levels. Thus, weak chip manufacturing activity is expected to have led to a decline in overall IP in May.

Meanwhile, survey results will likely show that consumer and business sentiment has improved. Equity markets rebounded on the back of the AI hype, and interest rates did not change much as the BoK paused for two meetings.

Japan’s manufacturing activity and labour market upbeat while inflation likely to heat up

Based on the recent strong PMI readings, we believe that Japan has continued its gradual recovery. Industrial production should show another monthly gain on the back of solid domestic demand and car production. The golden week holiday in May should probably boost service job hiring, and thus labour market conditions are expected to remain healthy.

On the inflation front, Tokyo consumer prices are the key input to the Bank of Japan's policy decision. We think July Tokyo consumer inflation should reaccelerate with both commodity and services prices rising.

China’s industrial profits to remain in the red

May industrial profits are likely to remain very negative. Following a year-to-date year-on-year decline of 18.2% in April, we look for a 21% decline in May.

Singapore’s industrial production to track soft NODX

Industrial production will likely remain in contraction, mirroring weakness reported in the recent non-oil domestic exports figures. While we could see output increase on a monthly basis (1.7%), the overall YoY reading should stay negative (-3.9% YoY). We expect industrial production to struggle in the near term, given our outlook for NODX.

Asia Economic Calendar

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

22 June 2023

Our view on next week’s key events This bundle contains 2 Articles