Asia week ahead: Japanese rate decision and data from South Korea, China, Taiwan, Australia

The Bank of Japan is likely to leave rates unchanged, but signal hikes are coming in the months ahead. Markets will also focus on South Korean data on monthly activity, trade, and inflation, China's purchasing managers' index and industrial profits and Taiwan’s GDP

Japan: BoJ likely to hold rates, but signal hikes in coming months

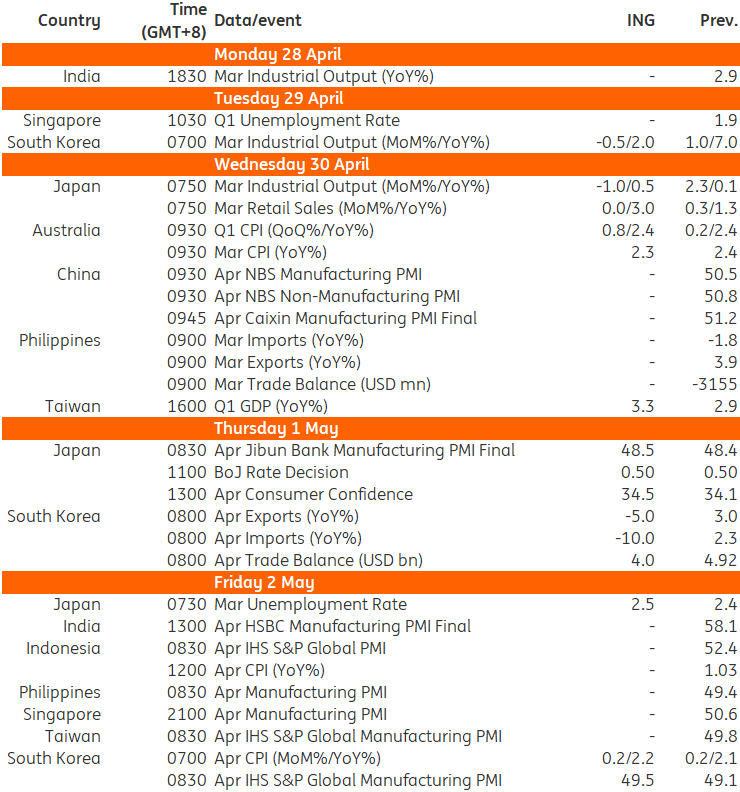

The Bank of Japan will stand pat despite the sizzling inflation amid uncertainty surrounding the US trade policy. However, the BoJ will signal additional interest rate hikes in the coming months.

South Korea: Data on monthly activity, trade, and inflation

South Korea’s monthly activity data is expected to contract based on weaker-than-expected first-quarter GDP and falling construction and equipment investment. Also, early April trade data suggests that full-month exports will drop thanks to direct and indirect US tariff impacts. Imports should drop even faster, keeping trade balance in surplus. Meanwhile, inflation is expected to rise modestly to 2.2% year on year. Gas prices declined, but manufactured food and services costs probably rose.

China: Markets will closely monitor the first PMI data since escalation in tariff conflicts

China releases industrial profits data on Sunday, offering markets a read on whether profits returned to positive territory following a -0.3% YoY contraction in the first two months of the year. China’s official and Caixin PMIs will both be released on Wednesday, providing our first look at how tariff actions impacted the manufacturing sector.

Taiwan: Frontloading fueled by tariffs likely to support Q1 GDP

Taiwan releases its 1Q25 GDP data on Wednesday. We’re looking for growth of around 3.3% YoY. Taiwan’s economy is likely to have been supported by some import frontloading from US customers.

Australia: Mixed inflation data

Australia’s consumer price index could offer a mixed picture on a quarter-on-quarter basis in the first three months of the year. Overall, the CPI is likely to edge higher on rising food and electricity costs, despite some correction in prices for services.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article