Asia week ahead: Korean GDP, Tokyo inflation, Chinese rate decision

Key data on South Korean GDP and Tokyo inflation and a decision on Chinese interest rates are the main events next week. Asia also will pay close attention to trade war zigs and zags

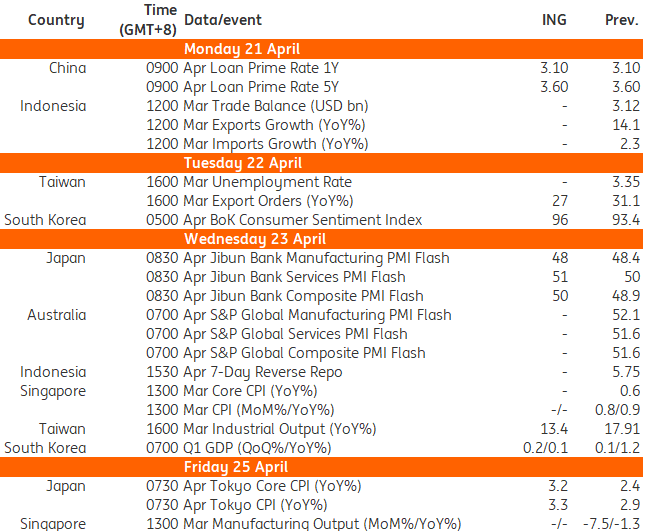

South Korea: GDP offers read on how political turmoil is affecting sluggish domestic demand

South Korea releases first-quarter GDP on Wednesday, giving us a read on how much domestic political turmoil dampened growth and the extent to which trade-war-related frontloading boosted exports. Overall, we expect GDP to rise 0.2% quarter on quarter, seasonally adjusted. The current account surplus for the first two months of 2025 widened quite meaningfully. A similar dynamic is expected for March, suggesting a solid contribution from net exports. Yet, domestic demand is likely to contract again as monthly activity and sentiment data deteriorate sharply. Following President Yoon’s exit, consumer sentiment may have improved compared to last month.

Japan: Tokyo inflation expected to reaccelerate, but BOJ to remain on hold

The highlight of Japan’s week will be Tokyo consumer price inflation data, due out Friday. Despite a cloudy outlook, inflation is likely to accelerate in April. Surveys indicate that companies plan to raise prices this month, while fresh food prices are expected to ease as the government releases reserved rice into the market. Despite a re-acceleration of inflation, the Bank of Japan is likely to maintain its policy rate at the end of the month amid high uncertainty surrounding US trade policy.

China: Central bank to leave key rates unchanged, but strong reasons to ease further remain

China’s loan prime rates (LPR) are expected to remain unchanged on Monday at 3.1% and 3.6% for the 1 and 5-year rates, respectively. The LPR is not seen moving without a cut to the 7-day reverse repo rate first. Low inflation and strong external headwinds amid escalating tariff threats provide a strong case for easing. But currency stabilisation considerations may prompt the People’s Bank of China to wait until the US Federal Reserve cuts borrowing costs.

Taiwan: Export orders and industrial production data

Taiwan’s export orders are likely to remain strong in the first quarter when the government releases the data on Tuesday. Exports have been stronger than expected. Data in March is likely to have remained strong as importers ramped up orders ahead of reciprocal tariffs. We're looking for a slight moderation of export orders to around 27% year on year in March. On Wednesday, Taiwan releases industrial production data. We’re looking for growth to moderate to 13.4% YoY.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article