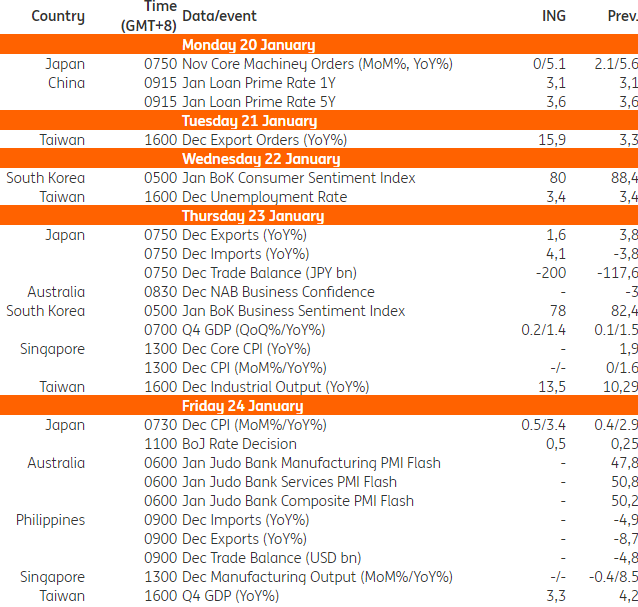

Asia week ahead: BoJ decision and GDP from Korea and Taiwan

The market will pay attention to the Bank of Japan's rate action as the latest comments from the BoJ officials are leaning towards being hawkish. Meanwhile, Taiwan is expected to log a solid growth rate while South Korea's GDP will show how the recent political turmoil dampened the economy

Japan: BoJ rate decision is a close call – but we expect a rate hike

The highlight of the week is the Bank of Japan's meeting on 24 January. Recent inflation and wage data have been encouraging and support the Bank of Japan's decision to raise interest rates at next week’s meeting. Latest comments from Bank of Japan officials have also shown increased confidence in sustainable wage growth. But, we should closely watch Trump’s inauguration which should deliver a negative impact on the global and Japanese economy. Japan will release trade and core machinery orders data early next week, as well as inflation on policy announcement day. Inflation is expected to rise quite sharply in December. The end of the government's energy subsidy programme is likely to temporarily push it well above 3% year-on-year. Exports are expected to pick up, supported by front-loading exports ahead of the implementation of Trump trade policies and robust IT demand.

South Korea: Surveys and GDP are likely to confirm a deteriorating economy

Business and consumer sentiment is likely to have continued to weaken in the wake of the tragic plane crash at the end of December. High frequency data suggest that consumption slowed down quite significantly during the national mourning period. We expect 4Q24 GDP to rise by 0.2% quarter-on-quarter (vs. 0.1% in 3Q24), mainly due to a positive contribution from net exports, while domestic growth deteriorates.

Taiwan: Relatively upbeat GDP and IP outcomes expected

Taiwan has several data releases scheduled in the week ahead, with the main highlight being fourth quarter and 2024 full year GDP, set for release next Friday. We’ve held a more upbeat forecast relative to the market on Taiwan’s growth, and expect the full year GDP to end the year at 4.7% YoY, up from 1.4% YoY in 2023. Aside from the GDP data, Taiwan will also release its export orders data on Tuesday, which are expected to have rebounded to 15.9% YoY to end the year, as well as Taiwan’s industrial production data Thursday, where we are expecting an uptick to 13.4% YoY from 10.3% YoY in November.

China: Quiet after data dump week

After the Friday data dump, China’s data calendar enters the quietest period of the year. The loan prime rates will be announced on Monday, with no change expected after the People's Bank of China kept benchmark rates unchanged. All eyes will be on Trump’s inauguration and whether or not we see any immediate tariff action announced against China.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article