Asia week ahead: China’s economic data, Japan’s GDP and India’s CPI and trade figures

China’s main data for July and rate decisions will dominate the week ahead in Asia, though there are also key inflation reports from India and Japanese activity data

China: Another data dump looming

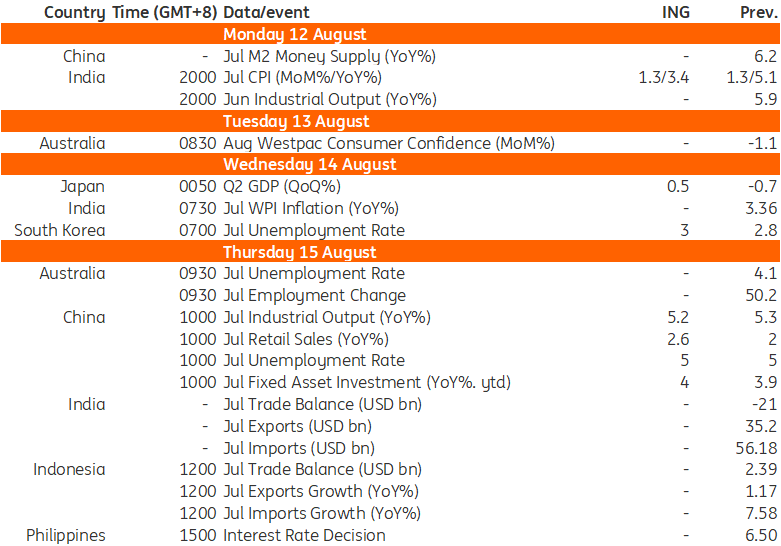

China’s major economic data is scheduled for release in the week ahead. On Thursday, the People's Bank of China will set the Medium-Term Lending Facility (MLF) rate, and we are expecting it to remain unchanged after last month’s rate cuts. It also seems likely that future monetary policy adjustments could start from the 7-day reverse repo rate as in July, making the MLF update less of a significant event for the market than in the past.

China will also publish the 70-city housing price data, and key economic activity data on the same day. We are looking for a smaller decline in property prices, and if more tier-one or two cities see some price stabilisation, this would be another positive step along the road to restoring confidence. Retail sales should see a bit of recovery after hitting a post-pandemic low last month on technical factors, and industrial production and FAI could see some stabilisation as well this month.

Japan: Growth to show signs of recovery

Japan will release its 2Q24 GDP on Thursday. This is expected to rebound to 0.5% quarter-on-quarter seasonally-adjusted (vs the 0.6% market consensus) but is unlikely to fully offset the 0.7% contraction seen in 1Q24. June manufacturing activity was weaker than expected due to another auto safety issue, which should weigh on auto-related activity. However, household spending and facility investment should improve. The net export contribution is also expected to turn positive due mainly to slower imports of commodities in 2Q24.

India: Big fall in inflation likely

Indian inflation for July may show a sharp fall. The monthly food price indications for July point to a smaller rise than in June of about 1.3% month-on-month, and incorporating that into the full CPI index should result in a similar rise of about 1.3% MoM for CPI. That will translate into about a 3.4% YoY inflation rate, down from 5.1% in June. This would be the first time that CPI inflation has been at the lower end of the RBI's 2-6% target range since September 2019, and could encourage further rate cut talk.

India reports trade balance numbers for July too. We are not expecting a significant shift from the $20.9bn deficit reported for June.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article