Asia week ahead: Upbeat data from Japan and China, but coming bite from tariffs keeps markets on edge

Activity in Japan and China should be solid before tariffs start to bite in the second quarter. Frontloading ahead of tariffs could provide a temporary boost to growth. But rising uncertainty is causing headaches for central banks. The Bank of Korea is likely to cut rates

Japanese inflation set to accelerate, but BoJ likely to extend its rate-cut pause

We are expecting upbeat data from Japan. The frontloading of goods being shipped to the US will likely boost core machinery orders and exports. This, however, doesn’t mean the positive tone will be carried over beyond the first quarter amid increasing uncertainty over tariffs. On the inflation front, consumer prices are expected to accelerate in March, driven by higher services costs. Earlier increases in fresh food are likely to be gradually passed on, particularly to eating-out and processed food costs. The Bank of Japan will monitor closely how the US tariff policy impacts the economy, leaving rates unchanged for the time being.

China releases slate of key data including GDP

China will release almost all of its key data sets for March. The main event is first quarter GDP on Thursday. We look for a rather sanguine 5.3% year-on-year growth rate. This reading, of course, comes before tariffs start to bite from the second quarter onward. As of March, domestic activity is expected to remain resilient. We expect retail sales and industrial production to edge up to 4.5% YoY and 6.0% YoY, respectively. Fixed-asset investment is likely to remain broadly stable, down 0.1pp to 4.0% YoY, year to date. Trade is seen moderating a bit further in March as tariffs came into effect. But the bigger hit is likely yet to come.

We will also be watching property prices. The question is whether market volatility translated into further downward pressure on prices. This year’s focus is on supporting domestic demand. But we expect it will be challenging to restore household confidence as long as home prices are still falling. The recent stabilisation of prices in tier 1 and 2 cities is a good start, but prices have yet to confirm a trough countrywide.

Data aside, all eyes will be on the China policy response after Trump imposed 145% tariffs on Asia's biggest economy. Markets will await signs of policy support in the week ahead. Rate and reserve-requirement-ratio (RRR) cuts are possible, along with further announcements of fiscal policy plans to support domestic demand.

Bank of Korea likely to cut rates as downward pressure on KRW eases

It’s a close call, but we expect the Bank of Korea to cut its policy rate by 25 bp at Thursday’s meeting. The market consensus is still leaning towards no BoK action in April. The difference between April and May depends on how the BOK interprets recent won weakness. While the BoK acknowledges the negative impact of tariffs on the economy, it’s cautious about whether rate cuts may weaken the KRW further from current levels. Our argument is that despite President Trump’s 90-day tariff pause, downside risks to growth have increased more than expected and the KRW has moved to the 1,450 level. As such, the Bok’s priority is likely to be on supporting growth.

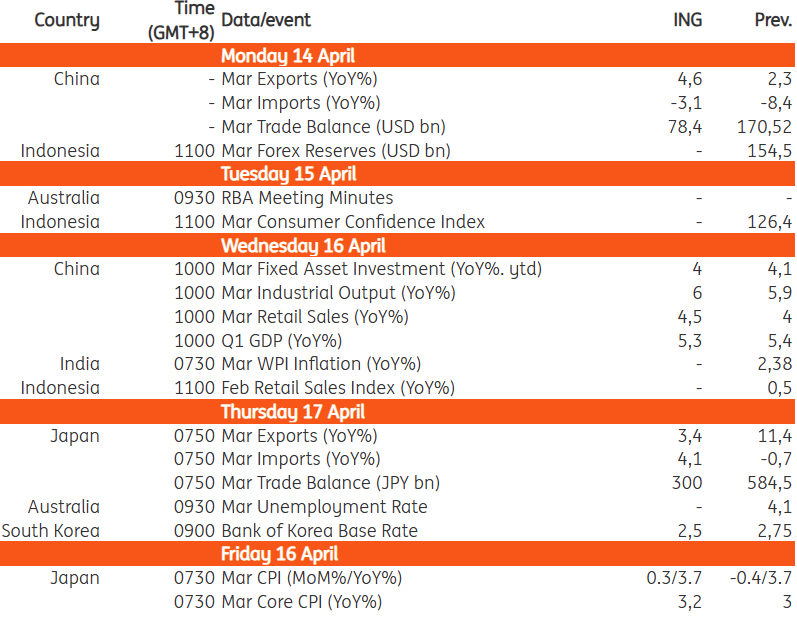

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article