Asia Morning Bites

Korea introduces a new business sentiment index and Beijing delivers property support. BSP rate policy decision later as well as China’s industrial profits numbers

Global Macro and Markets

- Global Markets:. After a couple of days of inaction, US Treasury yields headed higher on Wednesday. However, it is far from clear what the driver for this was. There was little macro data to speak of, no notable Fed comments (though there were some dovish comments from the ECB’s Olli Rehn), and a moribund equity market. Perhaps this is just a bit of profit-taking ahead of Friday’s core PCE release? Maybe the successful Fed bank stress test was a factor? Whatever the cause, 2Y yields rose 5 basis points and the yield on 10Y Treasuries rose 8.2bp to 4.329%. This increase in yields has given the USD some support. EURUSD has dropped to 1.0680, and the AUD has given back all of yesterday’s CPI-induced gains to sit at 0.6644 currently. Cable has also dropped to 1.26622 and the JPY has broken back above 160. All of the other Asian currencies were weaker against the USD yesterday. The THB, TWD and SGD were the weakest of the bunch, while the VND, CNY and KRW held up better, but still lost a little ground. US stocks moved higher again, but not substantially. The S&P rose just 0.16%, though the NASDAQ was a little stronger, rising 0.49%. Chinese stocks managed to make gains too, though the 0.09% rise for the Hang Seng was negligible. The CSI 300 rose 0.65%.

-

G-7 Macro: US data was uninteresting yesterday. Some revisions to home sales figures won’t have been responsible for the markets’ moves yesterday. Today we have the third revision of 1Q24 US GDP – which is one for the history books and not very exciting. Preliminary May US durable goods orders are worth a closer watch, though they are always very choppy. The Eurozone publishes a set of confidence figures for June.

-

China: Property market support continued yesterday, as Beijing joined other tier 1 cities in easing housing purchase requirements. The minimum downpayment ratio was cut to 20% for first-time buyers, and to 35% for second homes, and the mortgage rate floor was lowered. Similar measures in Shanghai appeared to bolster buying activity and led to Shanghai seeing 0.6% new home price growth in May, the fastest growth of any city. If Beijing’s market shows a similar trend after these measures, it will send an encouraging signal of stabilisation in the core Chinese cities.

China’s industrial profits data will be released this morning. Profits have grown at 4.3% YoY through the first four months of the year, and in general, profits are expected to maintain a gradual recovery trend this year amid a rebound in industrial activity. With that said, high price competition will likely keep profits growth near mid-single-digit growth for most of the year.

-

Philippines: No change to the overnight borrowing rate is the unanimous view of the Bloomberg consensus for today’s meeting. Month-to-date and quarter-to-date, the PHP has been one of Asia’s weakest currencies. We haven’t heard much more commentary from the BSP Governor about front-running the Fed recently. And for the sake of the PHP, it is probably better if it stays that way.

-

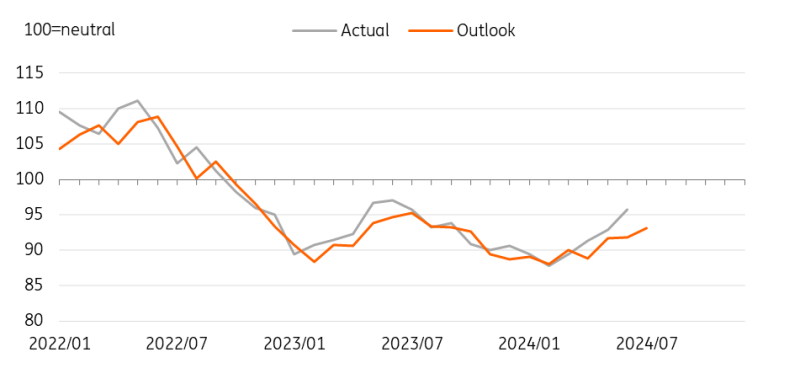

South Korea: From this month, the Bank of Korea began compiling a new Composite Business Survey Index (CBSI), which is a comprehensive measure of business sentiment. The CBSI is composed of major business survey indices (5 for manufacturing and 4 for non-manufacturing), with 100 set as neutral. Business sentiment appears to have improved for the past three months but remains below the neutral level. The CBSI outlook for all industries rose to 93.1 for July from the previous month’s 91.8 with both manufacturing (+1.4 pt) and non-manufacturing (+1.3 pt) up. In the sub-indices, the strongest growth came from export-oriented businesses (+4 points), while domestic-oriented businesses declined for a second month. Today’s data suggests that export-led growth will continue, while concerns about sluggish domestic growth are growing. Another interesting observation is that the actual index has been higher than the outlook index for the past three to four months. We suspect that the actual performance is better than businesses fear, but the still weak outlook should be negative for business activity as they tend to be more cautious about future investment or hiring.

South Korea: The Composite Business Survey Index gained for three months in a row

What to look out for : BSP meeting, US durable goods orders

- South Korea June Business Confidence Index (June 27)

- Philippines BSP meeting (June 27)

- US 1Q24 GDP, Initial Jobless Claims (June 27)

- US May Durable Goods Orders (June 27)

- Japan May Unemployment rate, June Tokyo CPI inflation, May Industrial Production (June 28)

- South Korea May Industrial Production (June 28)

- India Fiscal Deficit (YTD) (June 28)

- US May PCE deflator (June 28)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article