Asia Morning Bites

South Korean inflation slips below consensus. Australia reports net exports ahead of Wednesday’s GDP data

Global Macro and Markets

- Global Markets: US Treasury yields continued to slide on Monday. 2Y yields fell 6.5 basis points and 10Y yields dropped 11bp taking them all the way down to 4.388%. The catalyst for this appears to have been the much weaker-than-expected manufacturing ISM survey which adds to the list of recent weak activity data points (see more below). This sharp drop in yields has pulled EURUSD up above 1.09, and in the process has taken AUD to within a whisker of 67 cents. Cable is back above 1.28, and even the JPY has appreciated. USDJPY is down to 156.22 as of writing. The Asian FX pack has mostly not yet had a chance to respond to USD weakness and should rally this morning. Equities have weighed up the weaker growth environment and have concluded that it is less worrying than the positive prospects for rate cuts. The S&P 500 managed a small increase and the NASDAQ rose 0.56% yesterday.

- G-7 Macro: On a quiet day for macro and with no Fed speakers due to the blackout period before next week’s (13 June) FOMC meeting, the manufacturing ISM was the cause of most of the market action on Monday. The headline ISM index dropped further into contraction territory, dropping from 49.2 to 48.7. New orders data was even weaker. However, the employment index rose back above the breakeven level and although the prices paid index declined, it remained high (57.0). So, this was more of a mixed survey than the market reaction suggests and provides a clear clue as to how the market is thinking ahead of Friday’s payrolls. James Knightley in New York has more on this and the separate construction release in this note. Today is a quiet day for macro. Final April durable goods orders and the JOLTS labour data for April should not have much impact, though the JOLTS numbers are watched more these days than historically, so worth a quick look when they come out.

-

Australia: The net export contribution to GDP is due at 0930 HKT/SGT. This precedes tomorrow’s 1Q24 GDP release. A 0.7pp drag is forecast for the net export numbers and a 0.2% QoQ gain (1.2% YoY) for tomorrow’s GDP figures. A weak GDP release complicates things for the Reserve Bank of Australia, as it has to balance the apparent weakness of the economy with continued price stickiness. However, we would not read too much into today’s data as net exports can be strongly negatively correlated with other parts of the GDP release, such as inventories. So a surprise in today’s numbers may get offset by swings elsewhere.

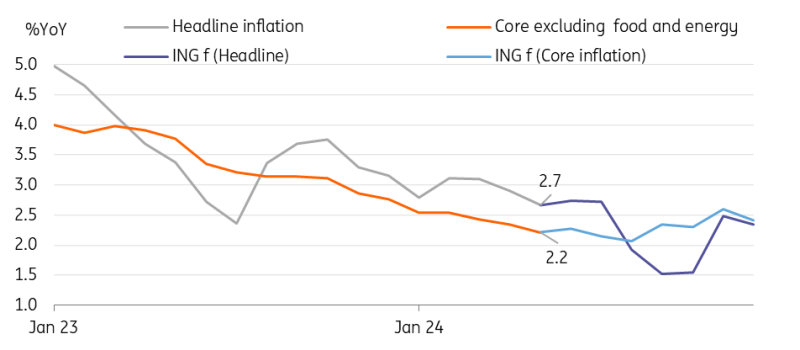

- South Korea: Consumer prices rose 2.7% YoY in May, moderating more than expected from the previous month (2.9% in April, 2.8% market consensus). The downside surprise mainly came from a larger-than-expected drop in fresh food. Core inflation excluding food and energy rose 2.2% (vs 2.3% in April), in line with the market consensus. Falling fresh food prices were the main reason for the easing month-on-month inflationary pressure, although other items are still adding to pressure. On a monthly basis, consumer prices rose 0.1% MoM nsa (vs 0.0% in April, 0.2% market consensus). Harvest conditions have improved, but also government efforts such as lowering tariffs on imported food and increasing quotas on fresh food, have taken some pressure off.

As we expect inflation to remain at current levels for a few more months, the Bank of Korea's (BoK) pause is likely to be extended. In our projection, we assume that the government is likely to continue its price stabilization measures until the third quarter, thus inflation is expected to fall meaningfully to the 1% level from August/September - mainly due to last year’s high base. We believe that the BoK's policy stance will gradually turn dovish in the third quarter as inflation starts to cool and we expect a 25bp rate cut in October.

-

India: Exit polls point to another large majority for PM Modi in the recent elections. Official results should begin to emerge today to confirm these polls.

South Korea: We expect CPI inflation to decelerate from August

What to look out for:

-

South Korea CPI inflation (4 June)

-

US JOLTS, factory and durable goods orders (4 June)

-

South Korea GDP (5 June)

-

Philippines CPI inflation (5 June)

-

Australia GDP (5 June)

-

China Caixin PMI services (5 June)

-

Singapore retail sales (5 June)

-

US ADP employment and ISM services (5 June)

-

Australia trade balance (6 June)

-

Taiwan CPI inflation (6 June)

-

ECB policy meeting (6 June)

-

US initial jobless claims (6 June)

-

India RBI policy meeting (7 June)

-

Taiwan trade (7 June)

-

US non-farm payrolls (7 June)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article