Asia Morning BitesSouth Korea

Asia Morning Bites

Korean unemployment rate decline masks domestic weakness. Asian FX gains as market confidence on US rate cuts is boosted by PPI data

Source: shutterstock

Global Macro and Markets

- Global Markets: The market mood has shifted back towards rate cuts again in the last 24 hours with US PPI data coming in on the soft side ahead of today’s CPI numbers. 2Y US Treasury yields fell 8.8 basis points, and the 10Y yield fell 6.1bp taking it to 3.843%. EURUSD has climbed steeply and is eyeing 1.10. Other G-10 currencies have been pushed stronger by the USD weakness. The AUD is up to 0.6639, Cable is up at 1.2866, and the JPY has declined to just below 147. Asian FX also had a strong day yesterday. The PHP and IDR gained about 0.6-0.8% respectively, and USDCNY has dropped to 7.1550. US equities were in a happier frame of mind on Tuesday. The S&P 500 rose 1.68% while the NASDAQ gained 2.43%. Chinese stocks made smaller gains of about 0.3-0.4%.

- G-7 Macro: Yesterday’s PPI can’t be relied on to give too accurate a steer on today’s CPI numbers, but the direction has at least encouraged thoughts of a softer CPI print. The headline July PPI inflation rate dropped more than expected to 2.2% YoY, down from 2.7%, though there was a more mixed story from the core figures. There is plenty of scope for CPI and other data releases to inject further market volatility over the coming weeks ahead of September’s FOMC meeting, and our Chief US economist and FX strategists consider a number of scenarios in the linked note. Along with the PPI data, there were also more encouraging signs from the small firm US NFIB business survey. The same cannot be said for the German ZEW business survey, which continued to head lower. Other G-7 data releases today include July CPI for the United Kingdom and preliminary 2Q24 GDP for the Eurozone. An increase of 0.3% QoQ is the consensus forecast for the Eurozone GDP result, which would leave year-on-year growth unchanged at 0.6%.

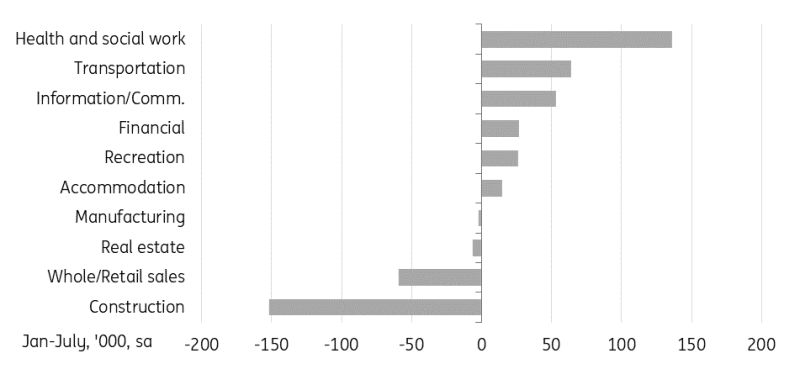

- South Korea: The jobless rate unexpectedly dropped to 2.5% in July (vs 2.8% in June, 2.9% market consensus), the lowest since November 2023. The labour participation rate edged down to 64.2 %, the third consecutive monthly decline from the recent peak of 64.7% in April. The increase in employment for the month was mainly driven by the service sector, while manufacturing (-23k) and construction (-19) shed jobs. Construction recorded its sixth consecutive monthly decline, reflecting sluggish construction activity. Among services, transportation (21k), education (40k), and health & social work (8k) added jobs, but wholesale/retail sales (-26k), real estate (-14k), and recreation-related (-10k) sectors lost jobs. On a YTD basis, health and social work added the most jobs (136k), largely driven by government social welfare policies. Meanwhile, private-sector hiring has been sluggish, including manufacturing (-2k), construction (-152k) and whole/retail sales (-59k). These declines are contributing to weak household consumption. We are concerned that private-sector hiring will remain sluggish, weakening household income and consumption.

South Korea: Private-sector hiring has been sluggish

What to look out for: India trade balance

August 14th

S Korea: July unemployment rate

India: July wholesale prices

August 15th

Japan: 2Q preliminary GDP, June industrial production

Australia: July employment change, unemployment rate

China: July industrial production, retail sales, fixed assets Ex rural

Indonesia: July imports, exports, trade balance

Philippines: BSP overnight borrowing rate, June Overseas cash remittance

August 16th

Singapore: July non-oil domestic exports

Japan: June tertiary industry index

Taiwan: 2Q preliminary GDP

US: U. of Mich. sentiment

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article