Asia Morning Bites

Apparent Korean labour market tightness may not be all it seems

Global Macro and Markets

- Global Markets: US Treasury yields dropped yesterday as small-firm business sentiment fell sharply ahead of today's CPI release. 2Y yields fell 7.5 basis points and 10Y yields fell 5.8bp to 3.642%. EURUSD edged slightly lower to 1.1021. Other G-10 currencies were steady to slightly weaker against the USD, but the JPY made small gains to 142.26. Asian FX was quite mixed yesterday. The MYR made some further decent gains, along with the THB. But USDCNY moved up to 7.1208, and the KRW was also softer against the USD, with USDKRW rising to 1344. US stocks rose modestly yesterday, and there were also small gains from Chinese stock markets.

-

G7 Macro: The US small firm NFIB business survey fell to 91.2 in August. Although the month-on-month decline was one of the largest in some time, the level of business sentiment remains above the year’s lows. Today, the main event will be the US August CPI release. Consensus forecasters expect CPI to rise 0.2% MoM, leading to a reduction in annual inflation from 2.9% to 2.5% YoY. However, the same increase in the core series will leave core CPI inflation unchanged at 3.2%. The UK also releases a barrage of activity data including monthly GDP numbers for July.

-

South Korea: The jobless rate unexpectedly fell to a record-low 2.4% in August (vs 2.5% in July, market consensus 2.6%), trending down from the recent peak of 3.2% in December. The labour participation rate remained at 64.2% for a second month. Despite weak domestic growth conditions, the labour market appears to have tightened, but we don’t think this is necessarily a sign of recovery in domestic activity. Most of the job gains are in service industries, where wages are typically lower than in manufacturing. Also, in terms of contract type, temporary and daily work increased, while regular work decreased. Therefore, we believe that household income conditions may not have improved as much as the solid headline figure suggests. We believe that the BoK will pay attention to these details, and concerns about weak domestic demand are likely to lead to its first rate cut in October.

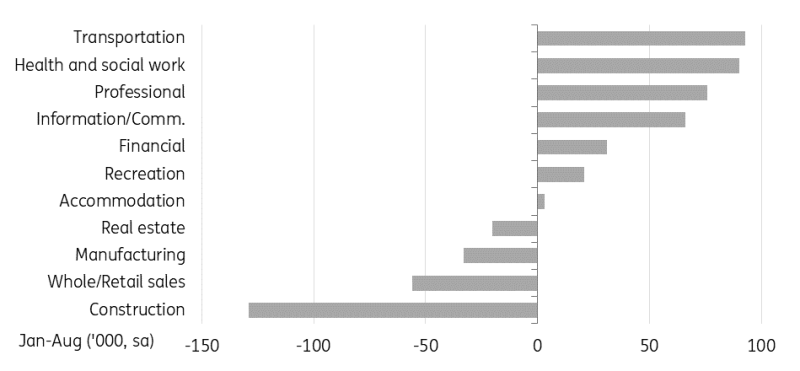

By industry, manufacturing shed jobs (-31k) partially due to summer labour strikes. Construction added jobs (23k) for the first time in seven months. Among the service sectors, the most notable gain came from professional/scientific and technical activities which added 44k jobs, mostly related to the IT sector (not manufacturing, but platform services and software engineering types of employment) and business facility management & support services (26k) also added jobs. Meanwhile, health and social work (-46k) shed jobs for the first time in five months, which is probably related to the on-going strike by doctors. Real estate lost jobs (-14k) for the third month in a row, reflecting weak property market conditions and accommodation/eating out (-12K) and recreation (-5K) jobs also fell, suggesting household leisure-related activity softened.

By status of worker, wage-earned employment rebounded for the first time in four months. Yet, regular employment fell (-65k) while temporary (contracts less than 1 year) and daily (contracts less than 1 month) rose 56k and 18k respectively.

Despite record low unemployment rate, employment in major sectors softened

What to look out for: South Korea unemployment rate, US CPI

September 11th

S Korea: August unemployment rate

US: September 6th MDA mortgage applications, August CPI

September 12th

Japan: August PPI

India: August CPI, September industrial production

US: August PPI final demand

US: August ADP employment change, ISM services index

September 13th

US: August monthly budget statement, import, export, trade balance

Japan: July industrial production

Thailand: September 6th gross international reserve

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article