Asia and the great reflation trade in charts

How Asia compares to the rest of the world in its battle against Covid-19 and its race to recovery

Pandemic in Asia vs Rest of the World

When it comes to the Covid-19 pandemic, Asia is not doing quite as well as it was, with India seeing a new surge in cases, and Indonesia and the Philippines both struggling to keep case numbers low. But on the whole, the Asia-Pacific region has managed far better than its Western peers, with far fewer cases in total, and many fewer casualties.

However, the hurdle for restrictive measures on movement in Asia is a LOT lower than it is in Europe or the US. And as a result, the impact in terms of the GDP outcome in Asia has not been much better.

How Asia's worst affected by Covid-19 compare internationally

We may never know why Asia dodged a bullet

We may never have a complete picture of why the Asia experience (with some glaring exceptions) has been better than that in the West. The graphic below is not intended to be definitive. Scientists do think that for example, mask-wearing, as well as reducing the likelihood of infection, can reduce the severity of cases. But there is still disagreement over the mechanism. The only point we wish to make here is to note that Asia has largely seen far fewer cases of Covid-19 as a proportion of the population. The suggestions below may or may not have contributed to that outcome.

Why has Asia seen fewer cases of Covid? Here are 7 suggestions

Following the Covid crash, now the bounce

Despite limited cases in most Asia Pacific countries, strict social distancing measures and border closures dealt considerable damage to Asian economic activity in 2020. To a large extent, economic growth in 2021 in Asia is an inverse function of growth in 2020.

So for example, the Philippines contracted the most of any economy in Asia in 2020, more than 9.5%. But it will show the second-highest growth rate in the region in 2021, according to our own in house forecasts. This is mainly a mark of how bad the economy was in 2020, not how good it will be in 2021. And GDP will still be lower than it was pre-Covid.

That economic activity in 2021 will still lag pre-Covid levels will be true for most Asia-Pacific economies, with the exception of Australia, New Zealand, Korea, Taiwan and of course, China.

2020 GDP and 2021 ING Forecasts

Vaccine rollout is slow

One reason why 2021 growth will not be even higher is that vaccine rollout in the region is proving quite slow. Many countries in Asia only got their first physical vaccines in March. Authorities have not always been quick to authorise vaccines for use. Local aversion to vaccinations is often high, mixed with a sense that with low case numbers, vaccination might not be so urgent. And a mixed history with previous vaccines has meant a slow rollout and slow uptake. As a result, social and movement restrictions have not been relaxed as much as they might otherwise have been. Border controls remain tightly controlled. All of this may have led to weaker growth, though the counterfactual is hard to pin down.

Vaccine rollout in Asia has been super slow

Asia Vaccine Update

Global vaccination update - Asia lags the rest of the world

Daily case numbers are low, but in terms of vaccines and opening up economies, Asia lags a long way behind. Singapore is ahead of the Asian pack but broadly in line with the EU. Most other economies in Asia are barely on the scoreboard yet (measures only to one decimal place).

Vaccine rollout

2021 will see "tighter" fiscal policy

Even as governments try to remain accommodative to support stricken economies, there is no way that the fiscal generosity of 2020 can be repeated in 2021 or beyond. There's no Biden plan for Asia. Fiscal deficits are going to be large but smaller than in 2020. The Philippines is the one exception to this rule.

Fortunately, not all of this represents a cyclically adjusted primary balance shift- or fiscal drag- to put it another way. But some of it is, and this may eat a little into the 2021 bounce.

Put it another way, there is a penalty for trying to kickstart an economy, which is that this needs endlessly repeating if it is not to turn into a drag.

Deficits and fiscal "thrust"

IIF net EM inflow chart resumed outflows in latest published data

The IIF says that capital inflows to emerging markets (EM) were only about $10bn in March- their latest published data on net flows go to February (show increased outflows).

Outflows would be consistent with recent USD strength, but this is more a flight to the US and USD than a flight out of EM. So far at least, financial markets are remaining circumspect about global reflation, even if they are convinced about the US story.

EM net capital flows and EUR/USD

APAC bonds and FX since 1 Jan

Bond markets in Asia have not been particularly hard hit as US Treasuries have sold off (yields have risen).

- Yields on local currency bonds in the Philippines have risen the most, partly because the inflation figures there have been disappointingly high (resulting in a very negative "real rate") exceeding the central bank's (BSP) target despite weak growth. But this is mainly a food price effect caused by African Swine Fever. It will not persist, and as inflation dissipates, bond yields should converge to reflect the regional pattern. We do not expect BSP to respond, though it perhaps hampers its ability to ease further (not that there was much expectation for this).

- Again, there is no strong evidence of an emerging market effect at work - increases in Indonesian yields are not much higher than those for the regions' developed markets.

- North Asian (China, Korea, Taiwan) bonds have seen yields rise far less than those of South East and South Asia.

- In the foreign exchange space, the same absence of EM angst is evident, with the Philippine peso outperforming even the Singapore dollar and Korean won.

- The Indian rupee was outperforming in the FX and bond space until the Reserve Bank of India recently introduced a quantitative easing programme.

APAC 10Y yields (left) and APAC FX since 01/01/2021 (right)

Nominal Effective Exchange rates (NEERs) spreading out

Though most effective (or trade-weighted) exchange rates are bunched in the middle of the pack, there are a few outliers at both ends that could hint at a future correction.

At the stronger end, the Taiwan dollar benefits from equity inflows given the positive semiconductor cycle. That looks set to persist.

The Thai baht is the victim of its huge current account surplus - mainly a reflection of very weak domestic demand. That also looks set to persist.

The Indonesian rupiah, Indian rupee and Philippine peso are all on the weaker side. PHP has held up well in recent weeks with external imbalances contained by weak domestic demand. INR strength has been undermined recently by RBI policy.

Trade-weighted exchange rates

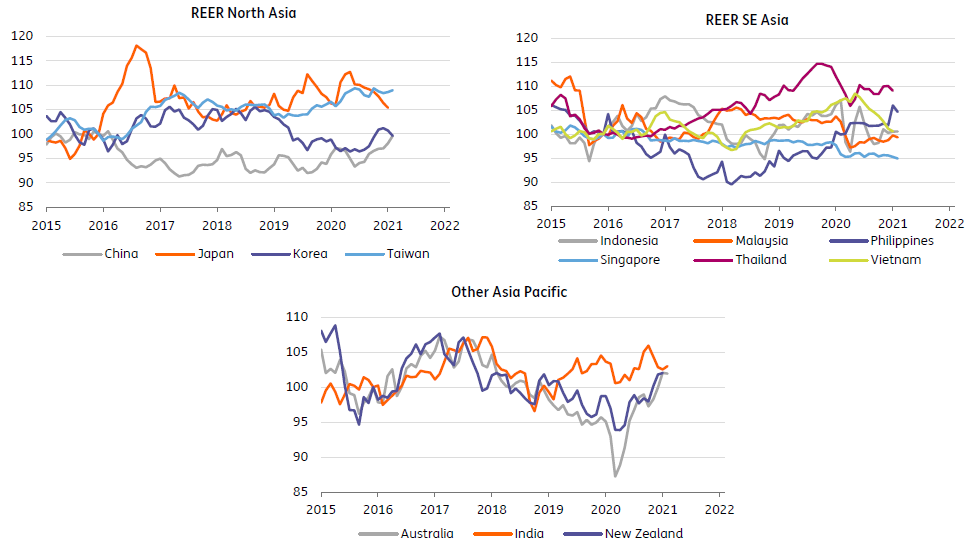

Real currency rates

Real effective exchange rates - one measure of the competitiveness of a currency - are all quite close to "neutral" levels after the Australian and New Zealand dollars appreciated substantially in recent months.

The Japanese yen and Taiwan dollar are both quite strong relative to neutral REER levels. That could weigh on future export strength, though more likely, it reflects export strength from these two tech-heavy economies.

In South-East Asia, the Thai baht is on the strong side, the Singapore dollar a bit weak, and the rest are unremarkable.

Real effective exchange rates

Trade competitiveness

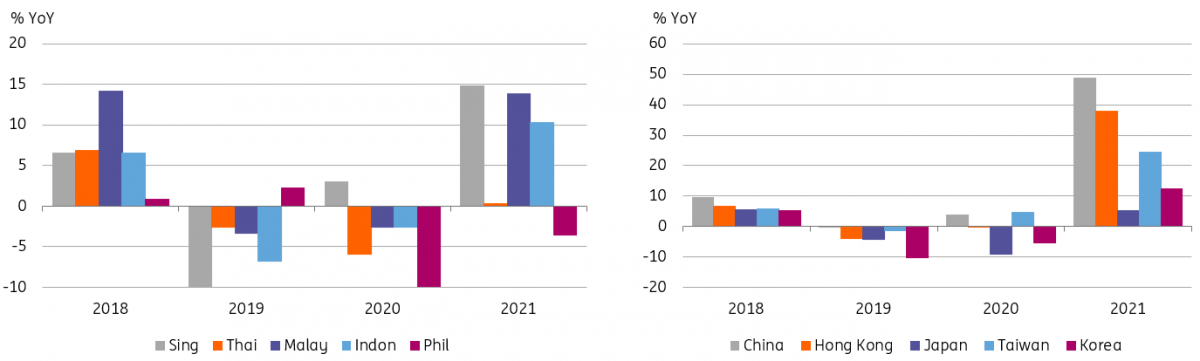

The export picture looks to be rebounding well, particularly for North Asia, home of the world's biggest electronics manufacturers, though Japan is lagging behind a bit - perhaps reflecting its broader goods export basket. In SE Asia, exports have also recovered well from their 2020 declines, though for Thailand, this remains anaemic, and the Philippines has not yet joined the export party.

Most of the trade pick-up in Asia is intra-regional. Extra-regional exports are still weak due to Covid in Europe, the US and elsewhere. Strong global demand for semiconductors and other electronics is likely to be driving much of this Asian strength.

ASEAN export growth (left) North Asia export growth (right)

Asian trade and oil

Although correlation is not the same as causation, and both series may represent a broader pick-up in global demand, there could also be a terms-of-trade impact from oil producers to Asian exporters.

Currently, the momentum is strongly positive, and peaks in Asian exports can be extended as we saw in 2017/18.

Asian exports and crude oil price

Asian Inflation- mainly low, but mostly picking up

Inflation was battered in North Asia by the pandemic. But the next few months will see a combination of base effects and real acceleration in monthly "run-rates" push inflation higher in year-on-year terms before it eases back again.

Some South Asian economies (especially emerging market ones - e.g. India, the Philippines) experienced rising prices during the initial stages of the pandemic as supply chains were disrupted. Coupled with natural supply shocks (African Swine Fever, typhoons, flooding etc.) this has pushed up inflation, mainly through food prices.

Such disruptions are temporary, and these will moderate in the coming months.

North Asia (left) South East Asia (right)

Conclusion

Generalising about a region as diverse as Asia is never a good idea, but with a number of caveats, we feel we can safely make the following observations:

- Asia's pandemic has so far been less widespread than in many other economies around the world.

- But due to aggressive social distancing measures, 2020 GDP growth was still badly hit, though this does set up 2021 for a bounce-back.

- That bounce would be stronger if accompanied by broader reopening measures, but the slow speed of the vaccine rollout has limited this.

- For most North Asian economies, inflation will pick up in the coming weeks and months as base effects from last year start to kick in. But for some South East and South Asian economies, inflation was already running quite high due to the disruptive impact of the pandemic on supply chains as well as food price shocks. These countries will see inflation moderate.

- Central banks will largely ignore inflation spikes.

- The US Treasury sell-off has had a more pronounced impact on bond yields of SE Asian economies and reflects how low real short-term yields have fallen.

- But there is little evidence of a broader emerging market issue arising in either bond or FX markets.

- Asian currencies have lost some ground to the US dollar since the beginning of the year, but strong external positions sometimes reflecting still very weak domestic demand means that such moves have been limited for most.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

15 April 2021

Hot in the city This bundle contains 9 Articles