Aluminium smelter shutdowns threaten Europe’s green transition

Another aluminium smelter in Europe is shutting down amid the ongoing threat posed by high energy prices. Since the start of the energy crisis, European aluminium output has fallen by more than half. These closures could also prove to be an obstacle to Europe’s green transition

High energy prices remain a threat to supply

Aluminium producer Speira said it will shut down its German plant Rheinwerk this year due to the challenging energy market. Last September, the producer reduced capacity by 50% at the plant amid surging power prices. Speira said it will now focus solely on recycling and processing aluminium into value-added products.

Soaring energy costs following Russia’s invasion of Ukraine have squeezed producers’ margins, with energy-intensive metals being particularly affected.

Several output cuts have taken place since December 2021 at key European smelters. Europe had suspended about 1.4 million tonnes of capacity by the end of 2022, accounting for 2% of the global total.

Aluminium, often referred to as “congealed electricity”, is the most energy-intensive base metal to produce, requiring about 40 times more energy to make than copper. One tonne of aluminium requires about 15 megawatt-hours of electricity.

Falling energy costs in Europe have recently eased fears of a deep recession. TTF prices broke below EUR50/MWh in February, the lowest level seen since August 2021 after reaching an all-time high of EUR345/MWh in August 2022.

So far, only Aluminium Dunkerque has announced a restart of its curtailed capacity of 60kt/y in France. The plant is expected to be operating at full capacity by the end of May, following support from the French government.

But in the aluminium industry, restarting a smelter is a long and costly process, meaning some of the production halts we have seen since 2021, could be permanent.

According to the latest data from the International Aluminium Institute (IAI), Western European aluminium output was at an annualised 2.73 million tonnes in December, down by 540,000 tonnes from December 2021 and the lowest production rate this century.

Aluminium requires about 40 times more energy to make than copper

Production costs still too high for many smelters

While LME aluminium prices have fallen by 40% since reaching historic highs a year ago, production costs remain too high for many aluminium smelters in Europe.

Electricity is the largest single expense for producers, typically accounting for about 40% of production costs.

LME aluminium prices reached a high of $3,849/t in March but have now declined from their post-invasion peaks, battered by fears of weakening global demand, as well as a stronger dollar. Growing recession risks in the US and Europe and an uncertain recovery in China is likely to continue to pose downside risks to the demand outlook.

We still believe, with the war with Russia raging on and given the uncertainty over the gas market in 2023, smelters will be reluctant to bring back production too quickly. Further smelter closures and curtailments in production cannot be ruled out given the uncertainty over energy prices throughout this year.

Any announcement of further closures could see aluminium prices spike but any potential rallies are likely to be unsustainable. We don’t anticipate European smelters restarting before 2024.

Last month, Norsk Hydro warned that the market remained challenging for aluminium smelters despite a recent drop in power prices and that a further 600,000 tonnes of aluminium capacity would still be at risk if energy prices spiked again.

European aluminium smelters hit by margin squeeze

Primary Aluminium Production in Western and Central Europe (mt)

Aluminium smelting cost components

Smelter shutdowns threaten Europe’s climate target path

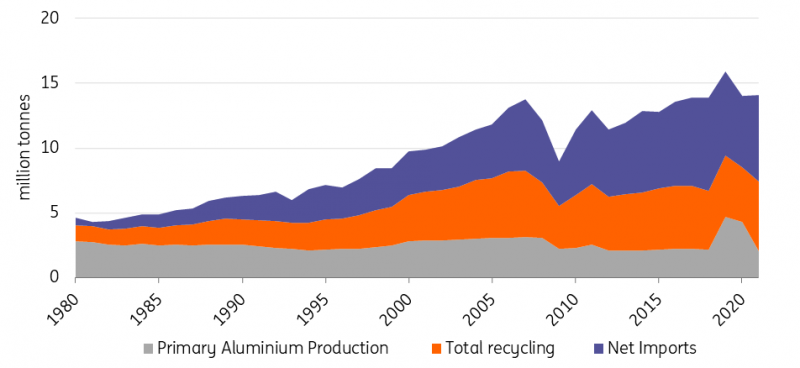

The most recent aluminium smelter shutdown comes at a time when Europe is trying to become more self-sufficient following Russia’s war in Ukraine. The more smelters shut down, the more reliant the region becomes on more expensive imports from more carbon-intensive suppliers, including China and Russia.

European smelters generate three times less CO2 than those in China, where coal is most often used to generate electricity.

Under the European climate target path, EU countries must cut greenhouse gas emissions by at least 55% by 2030, setting Europe on a path to becoming climate neutral by 2050.

Aluminium is a key component in mobility and transport, buildings, construction, packaging, aerospace, and defence. It is also used in almost all energy generation, transmission, and storage technologies, particularly those that will deliver the energy transition, such as wind and solar power, alternative fuel cells, hydrogen production, high-voltage cables, and batteries.

As a result, Europe’s 2030 energy transition will require four million tonnes of additional aluminium per year, rising to almost five million tonnes in 2040, equivalent to 30% of Europe’s aluminium consumption today, according to European Aluminium.

The highest growth in terms of absolute demand is expected to come from the transportation sector amid a shift to electric vehicles (EVs). By 2026, aluminium content per vehicle will rise by 12% to meet the needs of future hybrid vehicles and EVs, according to the Aluminium Association.

Aluminium’s usage in batteries and other EV components will double automobile manufacturers’ consumption of aluminium by 2050, according to forecasts from IAI.

Satisfying the increased demand via imports instead of producing in Europe would generate at least an additional 40 million tonnes of CO2 yearly, according to European Aluminium, equivalent to the yearly CO2 emissions of a country like Finland.

Earlier this year, Eurometaux, the European metals industry’s main lobbying group, representing major European producers, including Glencore, Boliden and Aurubis, warned that further long-term financial support is needed to help Europe keep control of raw materials that are crucial to the green-energy transition.

The European Commission is due to publish this week the Critical Raw Materials Act, which will attempt to lessen the dependence on non-democratic states and boost European autonomy to ensure the EU has access to materials needed to meet the bloc’s target of moving to net zero greenhouse gas emissions by 2050.

The regulation is part of Europe’s answer to the US Inflation Reduction Act (IRA), which offers $369bn of subsidies to green-tech manufacturers and has prompted several multibillion-dollar investments into US battery manufacturing.

Europe relies on aluminium imports

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article