AI Monthly: As competition intensifies, Europe falls behind

The competition to write the dominant large language model (LLM) is intensifying. Elon Musk’s Grok has raised billions over the last few months in an effort to beat rivals Gemini, Claude, ChatGPT and Llama. This competition means an increased risk of building too much infrastructure but also underlines the dominant position of the US

Competition to build the dominant model intensifies further

The competition to become the leading generative AI company is ramping up. There are currently five cutting-edge LLMs according to LMSYS:

- OpenAI’s GPT-4o

- Anthropic’s Claude 3.5

- Google’s Gemini 1.5

- Meta’s Llama 3.1

- xAI’s Grok-2

All five models have required billions of dollars in investment to get to this level of sophistication. Grok recently raised $6 billion based on a company valuation of $18 billion and is looking to raise an additional $5 billion, according to the Financial Times. Rival OpenAI is in talks to raise billions of dollars after a $13 billion commitment from Microsoft while Anthropic has attracted about $8 billion, including significant funding from Amazon and Google, according to news reports.

These large investments are not the end of the road for investments in LLMs but rather a shot across the bow. Notably, OpenAI’s Sam Altman has said there is a $7 trillion investment gap to overcome for generative AI to reach its potential. Although $7 trillion seems excessive to us, it is highly likely that LLMs will continue to attract billions in investment over the coming years.

It is no wonder then that Alphabet, Amazon, Meta and Microsoft have committed to invest close to $200 billion this year (up from $130 billion last year). This investment is mostly meant for the construction of data centres and the purchase of ultrafast chips, which are necessary to train and deploy LLMs.

As investments increase, so does overbuild risk

While these investments show that generative AI has serious potential, more investment also yields more financial exposure. Particularly because, as Mark Zuckerberg stated recently, it may be years before these investments generate returns. Should these investments result in overcapacity (i.e. an oversupply of computing power), then this bears significant risks for these companies.

On the flipside, big investments in computing power are good news for AI startups. Whereas big tech produces compute (the processing power and storage capacity needed to run applications, process data, and perform complex calculations) startups merely consume compute, as they do not have the resources to develop their own computing infrastructure. More capacity generally means a price decrease, and therefore an advantage for AI startups in countries where computing capacity is substantial.

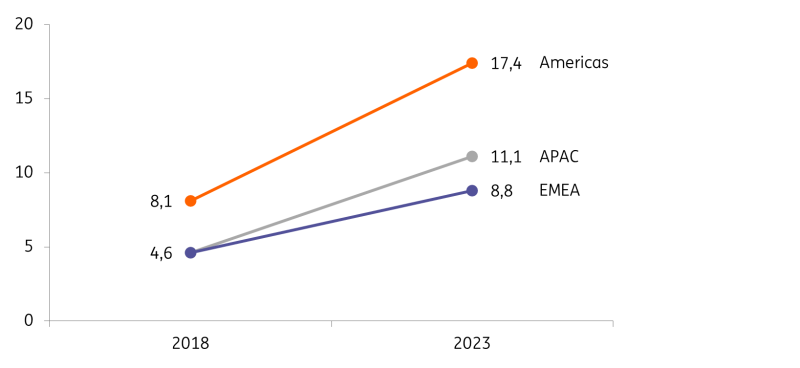

Availability of computing power increases greatly

Another consequence of increased investment in AI is the increase in IT power. In 2023, the Americas had a live supply of 17.4 GigaWatt (GW), which is considerably more than that of APAC and EMEA. As investments in the US are higher than elsewhere in the world, this gap is likely to widen in the coming years.

However, this spectacular increase in computing power raises questions about the sustainability of AI in the long term. As mentioned, investments will remain high in the coming years and additional computing power will be constructed. Smaller models might offer a solution here, as will the greening of energy mixes. But it is necessary for the technology sector to show a credible pathway towards greening AI, otherwise additional regulation is likely.

Global live supply has increased dramatically

IT power that is operational in GW per geographic region

The US is likely to dominate the AI market, while Europe is falling behind

The US currently has the five best LLMs. In addition, the country’s investment volumes are larger than anywhere else, and the same goes for the availability of computing power. This means that the US will likely dominate the AI market for the foreseeable future.

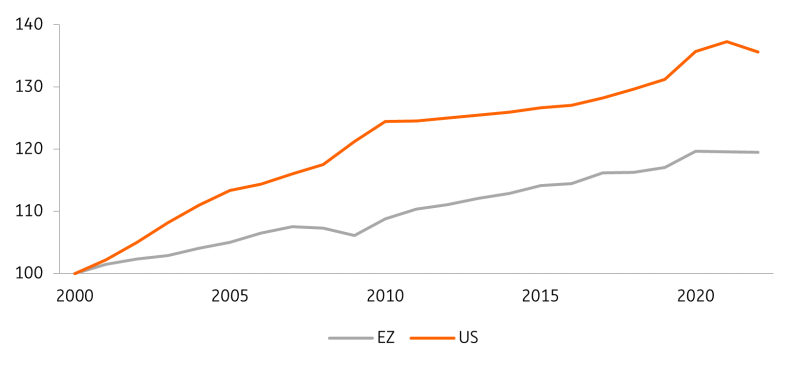

As AI will result in productivity gains, the US is better positioned than Europe to reap those benefits. This likely means that the divergence in labour productivity between the US and Europe is likely to increase over the coming years as AI productivity gains will be realised. This gap has already been widening. US labour productivity grew faster than Europe’s, particularly between 2000 and 2010, and again from 2020 onwards. AI might thus exacerbate this development.

For European competitiveness and strategic autonomy, this is undesirable. To this end, Daniel Ek and Mark Zuckerberg have argued that unharmonised legislation is the reason why Europe has not been able to produce a lot of leading tech companies. If Europe can harmonise legislation then it is better placed to quickly gain from AI, as it has more open-source developers than the US, for example.

However, we believe that overlapping regulation is not the only important difference between the US and Europe.

- First, the American labour market is less rigid. This means it is easier for American companies to reduce their workforce and less costly to invest in labour-saving technology.

- Second, there is more private capital invested in nascent technologies in the US, which incentivises the development of those new technologies. In contrast, it is more difficult to invest across borders in the EU.

- Third, the US government spends a lot more on AI through the CHIPS act ($280 billion over 10 years), whereas national European subsidy schemes are considerably smaller. These American policies also have drawbacks and risks, of course, but they do explain why the US is better positioned to profit from AI than Europe.

Difference in labour productivity between US and Europe has widened since 2000

Real GDP per hour worked, 2000 = 100

Gaps between companies and countries likely to widen

In sum, the AI arms race affects companies and countries alike. In the coming months, it is likely that the gap in AI advancements will widen between both countries and companies. For companies, it is not yet clear who will become the dominant LLM. For countries, however, the US has a commanding lead. Yet only time will tell who will win out.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article