A toxic cocktail for Italian bonds

- 16 May 2022

- FX Rates Italy

ECB tightening and weakening macroeconomic conditions globally are a toxic cocktail for Italian bonds. Debt sustainability is not yet a concern but we expect wider spreads until the ECB’s fragmentation facility is officially announced. The EUR/CHF reaction to a widening BTP-Bund spread may prove less pronounced than in previous instances

Bonds are having a rough ride this year. In the case of Italian sovereign debt, the volatility has been compounded by the disproportionate influence that European Central Bank purchases have played in setting market prices. These purchases are on track to end by early July and have already declined a fair amount. With this reality now widely acknowledged, and with markets having been given time to prepare for a world of tighter monetary policy, are Italian bonds out of the woods?

No debt sustainability concerns in the near-term

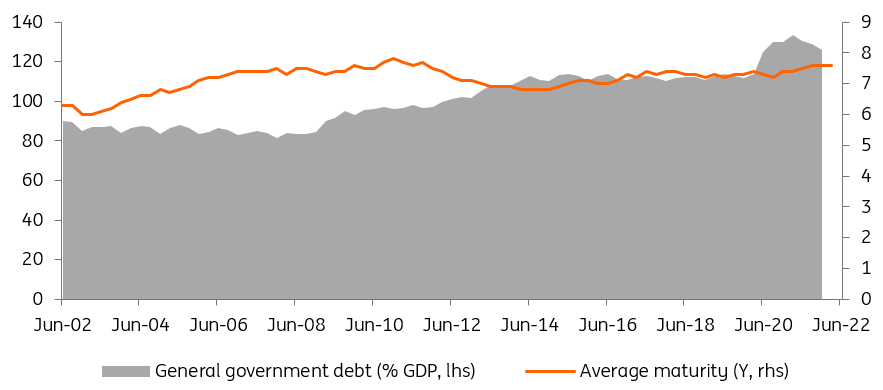

Italy, burdened by a long-standing high public debt issue, remains vulnerable to interest rate increases. When these materialise, as is the case now, the issue of debt sustainability arises. While we see reasons for concern in the medium term (the spring 2023 general election raises uncertainty and there are questions about what the ECB will do with its BTP QE portfolios) we believe that in the short run, the debt sustainability risk remains contained for two reasons. The first relates to the maturity structure of Italian debt. With an average maturity slightly above seven years, the transmission of higher interest rates to the whole stock of Italian public debt takes time. A sustained 100bp upward shift of the curve is estimated to add some €3bn to interest rate costs for the first year, and slightly less than €6bn in the second year. These are manageable amounts in a non-emergency environment.

High average maturity means higher interest rates will take a while to affect public finances

In a normalising world, Italy will tread a narrow path in its public finances

The second reason relates to the prudent attitude of Prime Minister Mario Draghi and Finance Minister Daniele Franco on fiscal policy matters. They seem well aware that in a normalising world, Italy will tread a narrow path in its public finances, and so far they have resisted pressure from some parties within the ruling coalition to frontload a deficit that deviates from targets, even when faced with recent dramatic events. The last decree, which prolonged measures to help businesses and households weather the energy price storm, is a case in point, as the extra spending is funded by an increase in a windfall tax on energy producers. We expect Draghi to try hard not to give in, well aware that if the EU Commission were to extend the suspension of the European SGP rules to 2023, this might revive the spirits of some deficit prone members of government, particularly in a pre-election year.

The ECB is no longer the buyer of last resort...

We tend to divide the ECB’s influence on financial markets between direct and indirect effects. In the case of Italian bonds, the direct effect of purchases is to remove a large amount of assets from private markets, engineering an artificial scarcity of sorts. Even when the ECB stops buying bonds, the direct impact of past purchases should remain to an extent. As a percentage of the amount of Italian debt available for private investors to buy, the ECB’s share will only reduce progressively by the amount of new debt sold by the sovereign to finance deficits.

Italian bonds are one of the most affected assets by monetary tightening

Those talking of an ECB put weren’t far off reality

Indirect effects are harder, but not impossible, to quantify. In the case of Italian bonds, the ECB has played the role of a buyer of last resort. This means that, in the eyes of private investors, the central bank was perceived as being there to come to the rescue in case of financial trouble. Those talking of an ECB put weren’t far off reality. In short, ECB purchases were seen as removing the tail risk of investing in Italian bonds. As a result, they were perceived as being less risky, and investors felt justified in chasing yields lower.

...but it could step back in soon to stop speads widening

We interpret talk of a hypothetical facility aimed at preventing fragmentation (ECB parlance for spread widening) as an attempt to restore the ECB put. The strategy seems to deliberately give as little detail as possible to investors. If the strategy is to avoid the market testing specific levels in spreads or in yields, it has its merits, but we think it will fail. In essence, it acknowledges that Italian bonds cannot trade without central bank support. The aim to make this support as light as possible is commendable, but markets have a well-defined track record of testing the extent of ECB support.

Absent ECB intervention, spreads will continue widening as core yields rise

We have no fundamental concerns about Italy, per se. Debt sustainability is not yet a concern, tentative steps to remedy the eurozone’s fiscal architecture have been taken in the NextGeneration EU recovery plan, and there is a more constructive stance on public investment. For now, the current market environment of worsening risk appetite and tightening monetary conditions is a toxic one for sovereign bonds, Italy included. We expect markets to test the ECB’s plan in the near-term, pushing 10Y spreads to Germany to 250bp. Long-term, helped by more concrete ECB support, and as market volatility eases, we fully expect investors to look more kindly towards Italy as an issuer.

| 250bp |

Italy-Germany spreadsuntil the ECB steps in |

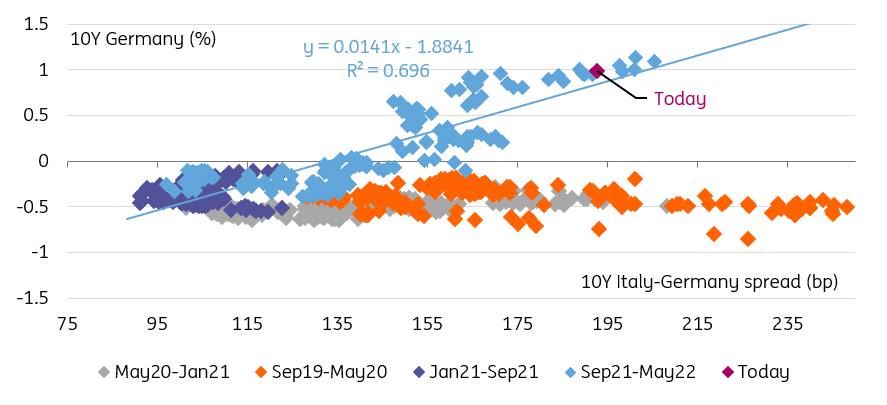

EUR/CHF: Correlation with BTP-Bund spread is weaker than on other occasions

EUR/CHF is more likely to show the highest sensitivity to swings in peripheral spreads than EUR/USD, given the franc’s role as a quintessential hedge against eurozone-related downside risks. The correlation between the pair and the 10Y BTP-Bund has historically been quite inconsistent: very strong in periods of distress for the Italian bond market and bond market and very weak during quieter periods.

The chart below shows how breaks above (and also below) the 200bp mark in the BTP-Bund spread have historically been the level around which the negative correlation between EUR/CHF and the spread tended to reach its peak. This suggests how the 200bp mark has often represented a key benchmark level, above which the market’s concerns about Italy’s debt effectively triggered an increase in defensive short EUR/CHF positions.

Is 200bp the key level for a EUR/CHF reaction?

As we can see in the correlation chart above, the EUR/CHF-BTP correlation has strengthened recently but remains weaker than it was in previous instances when the BTP-Bund spread was around the 200bp mark.

We think this partly boils down to the fact that the euro is already embedding a good deal of negative sentiment due to high energy prices and the EU-Russia standoff, which raises the bar for an adverse impact from peripheral spreads on the currency. At the same time, the Swiss franc has followed a path somewhat out of the ordinary, having first been allowed to strengthen significantly by the Swiss National Bank (which welcomed a strong CHF to curb inflation) in March and April, but then having seemingly reconnected with the wide ECB-SNB policy divergence and returned to the 1.04-1.05 area against the euro, despite the risk-off environment.

Incidentally, markets may feel less concerned about Italian spreads as the weakness in the BTP market is now more “imported” by ECB policy rather than related to any political or economic turmoil in Italy.

As long as Italian spreads (and other eurozone peripheral spreads) do not widen to a level that triggers a re-pricing of the ECB’s tightening expectations or serious concerns emerge around debt sustainability, the correlation with EUR/CHF may not pick up much more from the current levels. This doesn’t mean that the FX impact of widening spreads will be small, but simply less pronounced than in previous instances (like 2011 or 2018). Indeed, EUR/CHF downside risks remain non-negligible, especially given the SNB’s apparently higher tolerance for a strong franc. We only expect a recovery above 1.05 in EUR/CHF in the last quarter of 2022.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more