A pleasant surprise from US inflation, but it won’t last long

US inflation surprisingly undershot pretty much everyone's expectations in March, but higher prices from tariffs and supply chain disruptions are on their way

| 0.1% |

MoM increase in US prices ex food & energy |

A pleasant surprise for once

After all the volatility and back-and-forth on tariffs we are back watching the macro data and have been treated to a remarkably benign US CPI report for March. Headline prices fell -0.1% month-on-month and core (excluding food and energy prices) rose just 0.1%. In fact it was just 0.057% when measured to to 3 decimal places. Consensus was for +0.1% and +0.3% respectively, with some in the market fearing a 0.4% or even a 0.5% print on the assumption some companies were looking to pre-emptively hike prices in advance of the introduction of tariffs.

Price falls in key areas won't last as tariffs bite

The details show energy prices fell 2.4% MoM thanks primarily to a 6.1% drop in gasoline prices. Airline fares fell another 5.3% MoM after dropping 4% in February, which supports the story that airlines are responding to weakness in bookings. Recreation prices fell 0.1%, which is highly unusual and suggests discretionary spending is cooling and leisure and entertainment venues are starting to respond. Medical care commodities plunged 1.1% (prescription drugs prices fell 2%), which I am struggling to explain and would imagine gets reversed again soon, but the 0.7% MoM drop in used car prices is easier to understand after chunky increases over the past five months.

That won't be sustainable though given 25% foreign auto tariffs, which we suspect will deter potential buyers from purchasing a new vehicle. Instead they are likely to hold onto their current vehicle for longer, limiting the supply of used vehicles. Higher new vehicle prices will also inevitably mean higher repair and insurance costs that will also show up in CPI. Moreover, tariffs and supply chain issues caused by tariffs – China’s 125% tariff means US importers are desperately going to be looking at alternatives from other parts of the world, which will give those foreign companies greater pricing power – and will lead to higher prices from here.

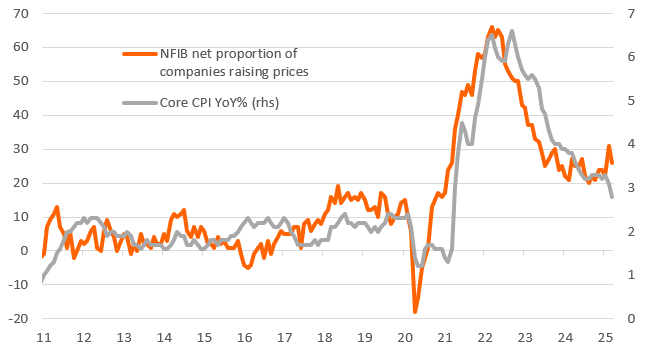

Companies still looking to hike prices

Volatility in Fed rate cut expectations to remain a key theme

Overall, today’s report is a very pleasant surprise, which on the face of it gives the Fed room for manoeuver if growth continues to soften. Nonetheless, the Fed will be wary of tariff-induced price hikes and supply chain disruption that we think will still push inflation back to 4% in the second half of the year. Federal Reserve interest rate cut expectations are all over the place right now – yesterday we had 107bp priced for 2025, only to drop to 75bp on President Trump's backtracking on some tariffs. Right now we are back to 89bp. Somewhere between three and four cuts this year looks about right to us given the deteriorating growth outlook and prospect of softer inflation prints in 2026.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article