A perfect storm for UK gilts and FX

Price action in UK gilts is going from bad to worse. A daunting list of challenges has arisen for sterling-denominated bond investors, and the Treasury’s mini-budget has done little to shore up confidence. Widening rate differentials are no consolation for the pound, with FX remaining the main vehicle to price UK country risk

2022 mini-budget: blank cheques

It was largely expected that the bill for the government’s energy price guarantee would run in the 12-digits (over £100bn) over its life and that most of this would be financed with extra issuance from the Debt Management Office (DMO). And yet, the mini-budget unveiled by the new chancellor added fuel to the fire already burning on the gilt market. The updated DMO remit for FY2022-23 includes an extra £72bn of borrowing, £10bn in T-bills and the balance in gilts. In our view, this is well within expectations but the current environment isn’t favourable to gilt sales.

Investors are worried the Treasury has effectively committed to open-ended borrowing

Alongside the confirmation of additional borrowing this year, the raft of tax cuts unveiled today clearly implies that it will not be contained to just this fiscal year. The cost of the newly-announced measures is reported to be £160bn over five years but, with the cost of the energy price guarantee highly dependent on wholesale energy prices, investors are worried the Treasury has effectively committed to open-ended borrowing.

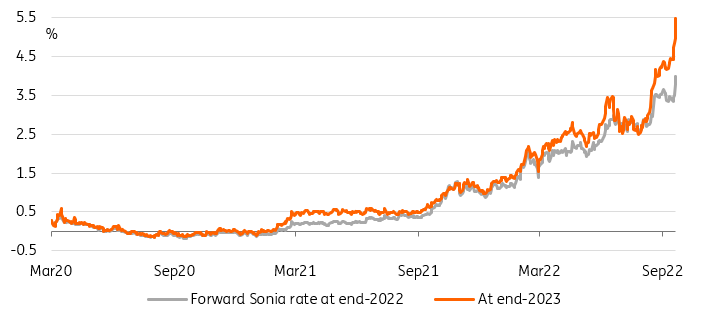

Markets are expecting a forceful BoE response to the new announced fiscal package

(Monetary) context matters

Of course, the additional borrowing comes at an inopportune time for gilts. Bond holders are already rattled by inflation and by the prospect of more Bank of England (BoE) hikes. Even if the central bank hiked only 50bp yesterday, compared to market pricing of 75bp, markets are betting that the pace of hikes will have to accelerate. The recent jump in yields implies that Bank Rate will peak next year well above 5%. That in itself is not a great backdrop for bonds but what has rattled investors is the prospect of the BoE hiking more in response to generous fiscal policy.

Markets are jumping to the conclusion that the BoE will have to respond in kind with even higher rates

Effectively, the BoE has reserved judgement on the inflationary implications of the energy price guarantee until its November monetary policy report but noted that the net effect will likely be to boost inflation over the medium term. Given the extra tax cuts announced, markets are jumping to the conclusion that the BoE will have to respond in kind with even higher rates. The prospect of the BoE and the Treasury competing with each other is a particularly unnerving one for bond investors.

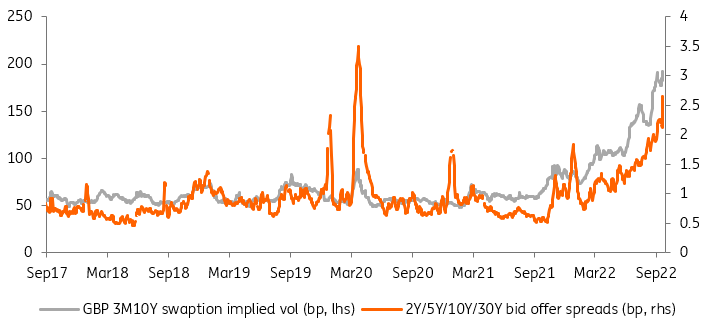

The already impaired gilt market is no longer able to accommodate more supply and quantitative tightening

Financial stability in question

To us, the magnitude of the jump in gilt yields has more to do with a market that has become dysfunctional. If a sell-off in gilts is rational in response to more fiscal spending, tax cuts, and higher inflation, the magnitude of the move should give policymakers pause for thought. This is particularly true of the BoE which is about to ramp up its quantitative tightening (QT) programme with outright gilt sales at £10bn per quarter.

We have written at length before that trading conditions in the gilt market call for the BoE to tread very cautiously when it comes to adding to the selling pressure already evident in gilt markets. A number of indicators, from implied volatility to widening bid-offer spreads, suggest that liquidity is drying up and market functioning is impaired. A signal from the BoE that it is willing to suspend gilt sales would go a long way to restoring market confidence, especially if it wants to maximise its chances of fighting inflation with conventional tools like interest rate hikes. The QT battle, in short, is not one worth fighting for the BoE.

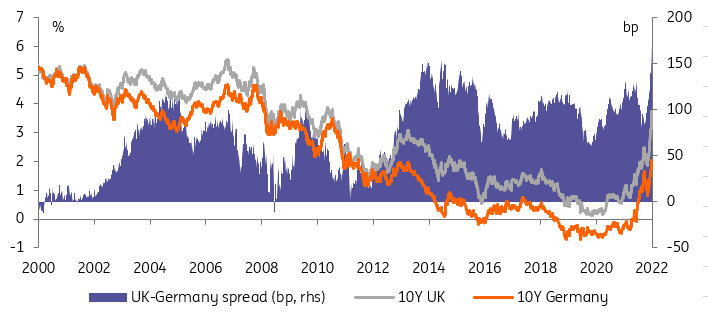

The spread between UK gilt and German bund yields widest in over two decades

Barring a change of direction on QT, we expect 10Y gilt yields to cross 4% and for the spread to German bunds to widen 200bp. The fact that the DMO’s additional borrowing is skewed to the front end of the curve, the sector most affected by expected BoE hikes, has added to the curve flattening dynamics.

GBP: The glass is half empty

Sterling has had another wild ride on today’s fiscal event – initially rallying on the biggest tax cut since the 1980s, but subsequently falling hard as the UK gilt market reacted to the prospect of a heavy new supply slate.

Sterling has been trading off fiscal concerns since early August. Expect this to remain the dominant theme as international investors again consider the right price, both in terms of sterling and gilt yields, to fund the UK’s widening budget deficit.

FX is probably the easiest vehicle to trade UK country risk

We have to remember that FX is probably the easiest vehicle to trade UK country risk – given that there is not much liquidity in sovereign credit default swaps for the UK. On this subject, investors will take great interest in what the rating agencies have to say about UK fiscal plans. The UK's long-term sovereign outlook is currently stable at all three of the rating agencies, S&P (AA), Fitch (AA-) and Moody’s (Aa3). The risk of a possible shift to a negative outlook will come when the ratings are reviewed on 21 October (S&P and Moody’s) and 9 December (Fitch).

Notably as well has been sterling’s disregard for interest rate differentials, where the very aggressive re-pricing of the BoE tightening cycle has provided no support to the pound. This leaves the BoE in a quandary but presumably would have to be even more hawkish if the weaker exchange rate were to damage the UK inflation profile still further.

Unless something can be done to address these fiscal concerns, or the economy shows some surprisingly strong growth data, it looks like investors will continue to shun sterling. For reference, the FX options now prices the chances of GBP/USD hitting 1.00 by year-end at 17%. That is up from 6% in late June. Given our bias for the dollar rally going into over-drive as well, we think the market may be underpricing the chances of parity.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article