A perfect storm for the Canadian dollar

USD/CAD is trading at the pandemic highs as the loonie is rapidly losing its low-volatility, safer commodity currency status due to Trump’s threat of 25% tariffs on Canadian goods. A fully-fledged North American trade war can take the pair to the 1.50 mark on the back of more Bank of Canada rate cuts. Political developments in Canada will be key next year

The floor seems to be shifting under the Canadian dollar as risks of a US-Canada trade war, large Bank of Canada cuts, a soft outlook for oil prices, and now political turmoil have seriously dented the loonie’s long-held status as the safer option in the high-beta commodity currency space.

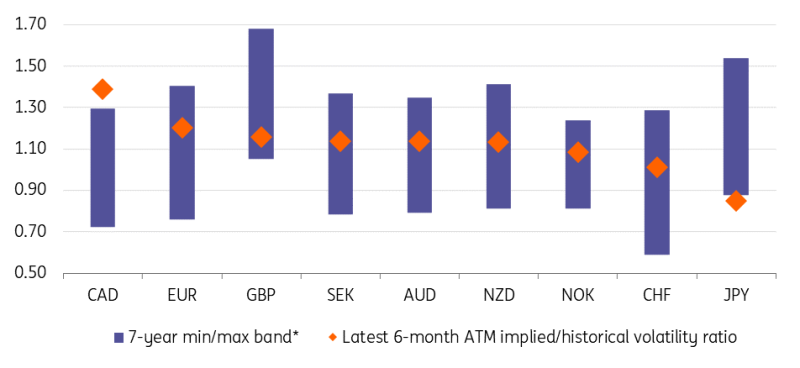

The clearest symptom of this change in sentiment is the rise in CAD’s implied volatility relative to historical volatility, a measure of the market-perceived risk of wider FX moves in the future. As shown below, that ratio is higher for CAD (1.39) than for any other G10 currency now when taking the six-month tenor. This is in sharp contrast to the generally low volatility character of CAD. If we exclude the February-March Covid shock, we have to go back 10 years (October 2014) to see CAD implied /historical volatility ratio at or above 1.40.

Cost of hedging CAD has spiked

2% worth of risk premium priced into CAD

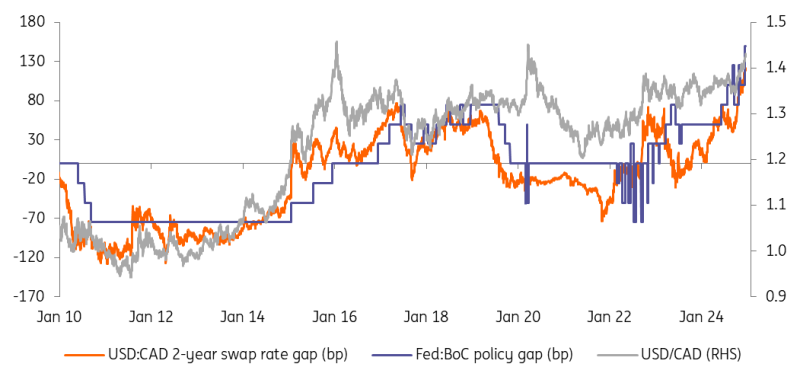

USD/CAD has appreciated 7.5% since the start of 2024. This has been primarily a consequence of the exceptional widening in the short-term USD:CAD rate differential driven by Fed-BoC policy divergence. This was – until November - entirely macro-justified: lower inflation and softer growth in Canada relative to the US had led to earlier and faster BoC cuts.

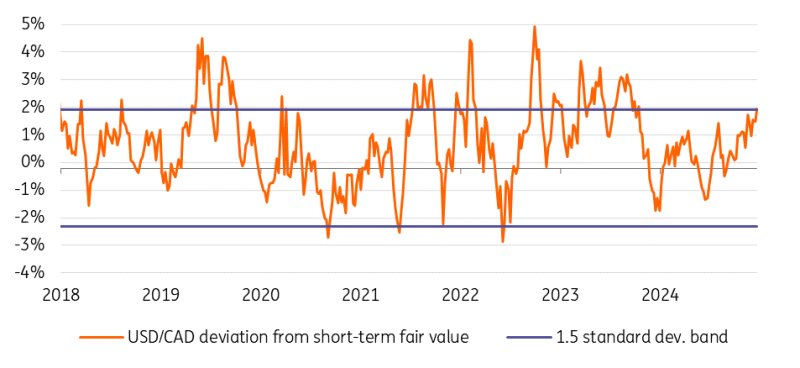

The election of Donald Trump and his hawkish rhetoric on hitting Canada with 25% tariffs have added a whole new level of uncertainty for CAD. This has generated a risk premium that we estimate to be worth approximately 2% at current USD/CAD levels (1.43). That is the excess USD/CAD appreciation that is not justified by market factors like rates, equities or commodities, but related to an additional bearish force acting on CAD – in this case, tariff risk.

USD/CAD moving into stretched overvaluation

We have to put this 2% risk premium into historical context. It is currently at the upper bound of the 1.5 standard deviation level, meaning that from a technical perspective, there is a case for a pause in the USD/CAD rally in the very near term – i.e. waiting for Trump to come into office.

When US-Canada trade tensions rose around mid-2018 ahead of the renegotiation of NAFTA (then renamed USMCA), that risk premium peaked at around 2.5%. That time though, US tariffs only hit Canadian steel and aluminium.

BoC cuts leave CAD in vulnerable position

The risks for CAD are materially larger this time compared to 2018. Trump is sounding more aggressive on protectionism and the explicit threat of 25% tariffs on all Canadian exports is a very serious risk to Canada’s economy, which is heavily dependent on exports to the US. The consensus view is that US tariffs would send Canada into recession, and the reaction by an increasingly growth-oriented Bank of Canada could be cutting rates further.

Indeed, the latest efforts by the BoC have been oriented toward giving breathing space to a highly rate-sensitive economy before any potential protectionism impact. No G10 central bank has cut rates more than the BoC this year (175bp in total), and the OIS market is pricing in another two cuts in 2025 to 2.75%. The BoC’s flexibility on the dovish side based on growth concerns could easily trigger a new dovish run in the CAD curve and more CAD depreciation should protectionist fears materialise.

Very wide Fed:BoC policy divergence

Based on the latest swap rate-FX correlation, a further 25bp widening in the USD:CAD two-year swap differential is worth around three big figures higher in USD/CAD. From current levels, that would propel USD/CAD above 1.45, and a 50bp swap-gap rewidening would send it close to 1.50. At this stage, we definitely cannot exclude a move to 1.50 in the coming months if that Fed-BoC policy differential widens further, especially in a fully-fledged US-Canada trade war scenario.

However, another 4-5% worth of USD/CAD appreciation would send the pair into overvaluation that exceeds the 1.5 standard deviation upper bound, according to our latest real medium-term BEER model estimates. A sudden leap into stretched mis-valuation from a historically low-volatility currency like the loonie carries a greater risk of a rapid correction unless it is matched by a sharp deterioration in economic fundamentals (the long-term drivers of a currency).

Canadian politics is the wild card

In December, political risk was also added to the potential bearish factors impacting CAD. The surprise resignation of Finance Minister Chrystia Freeland this week over friction with Prime Minister Justin Trudeau over budget measures in light of tariff risks likely raises the probability of a snap election before the October 2025 legislative deadline. Clearly, the US-Canada trade relationships will be central to the campaign.

Our best guess at this stage is that Trudeau will want to minimise the risk of an escalation with the US on trade before the vote, as that could hinder his already slim chances of forming a new minority government, according to the latest polls. The appointment of Dominic LeBlanc as new finance minister seems to support this strategy as he was part of the delegation that flew to Mar-a-Lago to meet Trump in November.

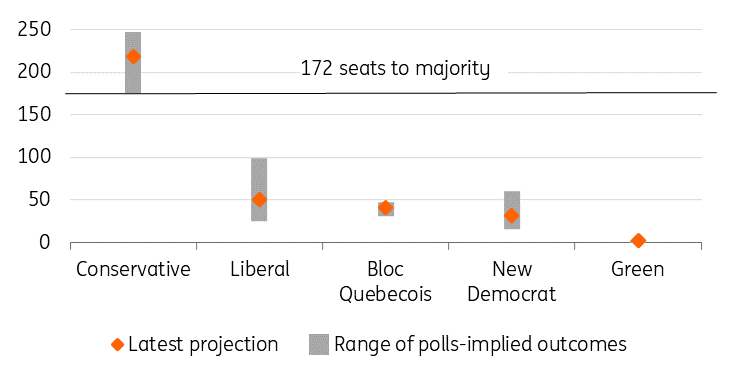

House projections place Conservatives comfortably in the lead

The latest polls strongly hint that the next government will be Conservative, with the leader of the opposition Pierre Polievre as prime minister. Polievre is politically closer to Trump, which in the long run could bode well for the Canada-US relationship, although he recently addressed Trump’s tariff threat as “unjustified” and said trade retaliation is a possibility.

His political agenda is focused on looser fiscal policy and increasing energy resource production, which are both positive for the Canadian dollar in the medium term. But, his ability to renegotiate the USMCA and de-escalate trade tensions with the US would inevitably be the primary channel for FX impact.

Watch the snowball effect

The question now is how far CAD can depreciate. As discussed above, we would leap into stretched mis-valuation territory around the 1.50 mark. However, that level would be, in our view, consistent with a scenario of a fully-fledged trade war – i.e. where the US imposes 25% tariffs and Canada retaliates.

In such a scenario, we could see a “snowball effect” where the Bank of Canada slashes rates further to support a tariff-hit economy, effectively adding depreciating pressure on the loonie. Trump may protest CAD’s weakness as a competitive advantage like he did with the yuan and China in 2019. If that results in more US tariffs, CAD would continue to depreciate, potentially past the 1.50 mark.

Should we see a de-escalation in the Trump-Canada trade spat, we expect USD/CAD to slip back to the 1.40 area, and even below if the Bank of Canada halts easing earlier than expected. At this stage, we are in front of very binary outcomes for the loonie: the first few weeks and months of Trump's presidency will tell us more.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article