A market’s guide to Italy’s upcoming presidential election

Italy's parliament will vote for a new president on 24 January. We look in detail at the debt and FX implications of different scenarios

24 January: the day presidential election polling begins

On Monday 24 January the process for the election of the new Italian president will begin. The voting process involves all MPs from both branches of the Italian parliament and representatives from regional administrations, with a total of 1008 “great electors”. The electoral process, with a secret ballot every day, will end once a candidate manages to reach the required majority. In the first three ballots, a qualified majority of at least two-thirds of potential votes (673 votes) will be needed to win, from the fourth ballot onwards the absolute majority (505 votes) will be enough.

Typically, the outcome of presidential elections has been the result of cross-party agreements, which do not necessarily materialise at the very start of the voting process. Only twice in the Italian republican history has a winner come out in the first ballot, and one of them was the election of Carlo Azeglio Ciampi, former governor of the Bank of Italy and prime minister.

To give some context, the president of the Republic in Italy has no political decision-making power, although it is a role that can become increasingly important in periods of political instability (like in the past few years) as it is ultimately the president that gives the mandate to a specific political leader to form a government. The president also has a say on the choice of ministers.

Berlusconi option met with prompt opposition from all other parties

As we write, no agreement has been reached yet on a shared name acceptable to an ample spectrum of parties. On the centre-left front, party leaders have so far kept their cards close to their chests, at least publicly, claiming that the right candidate should be non-divisive and not a party leader (an active party leader has never been elected in previous presidential elections).

The Five Star Movement (5SM) has also been vague, failing to supply a clear identikit of its ideal candidate. On the centre-right front, instead, an agreement of sorts has been reached within the coalition to propose Silvio Berlusconi as the candidate, pending his final decision whether to run or not.

The Berlusconi option met with prompt opposition from all other parties, which deem it extremely divisive and would not support it in the polls. A Berlusconi victory in the first three rounds, therefore, seems out of the question. In order to win after the third round, Berlusconi would need complete support from the centre-right delegates and an additional 50+ votes. Reaching that number could prove a very tall order, particularly in Covid times. The voting rules require a vote in presence, and chances are that some great electors might be forcibly absent on polling days due to quarantine (as we write some 35 MPs are reportedly Covid-positive).

As the requirement of 505 votes is unaffected by the actual number of voters, Covid-related absences might further complicate things for Berlusconi. So far, no decision has been taken on whether to amend the rule and allow a remote vote or not, and we believe it will remain at the heart of political discussions over the rest of the week. Should Berlusconi realise that he will not get enough support, in order to avoid a defeat in the polls he could well renounce his run before the end of this week. This would open the door to negotiations on alternative candidates.

A non-divisive candidate a more likely solution, with Draghi as our base case

We believe that the most likely outcome will be the choice of a non-divisive candidate, with a strong institutional background, and, possibly, with strong credibility capital to be spent internationally. Such a candidate could get sufficiently ample parliamentary support.

Mario Draghi would probably best fit very well these requirements, but other names could eventually emerge as alternatives. Over the next five years, it is crucial that Italy overcomes a fundamental challenge: the proper implementation of the recovery plan and, crucially, of the ambitious set of reforms that go with it. This is a long-term call, overarching the next legislature, under a government that might reflect a different majority. As this transition might not be flawless, having an internationally credible president would turn out to be extremely valuable in the process. The cross-parliamentary debate which will accompany fundamental reforms, will also likely frequently call for mediation abilities: which is more easily done by a non-divisive candidate.

Here, we look at the possible scenarios ahead of the presidential election, along with the implications for debt and FX markets.

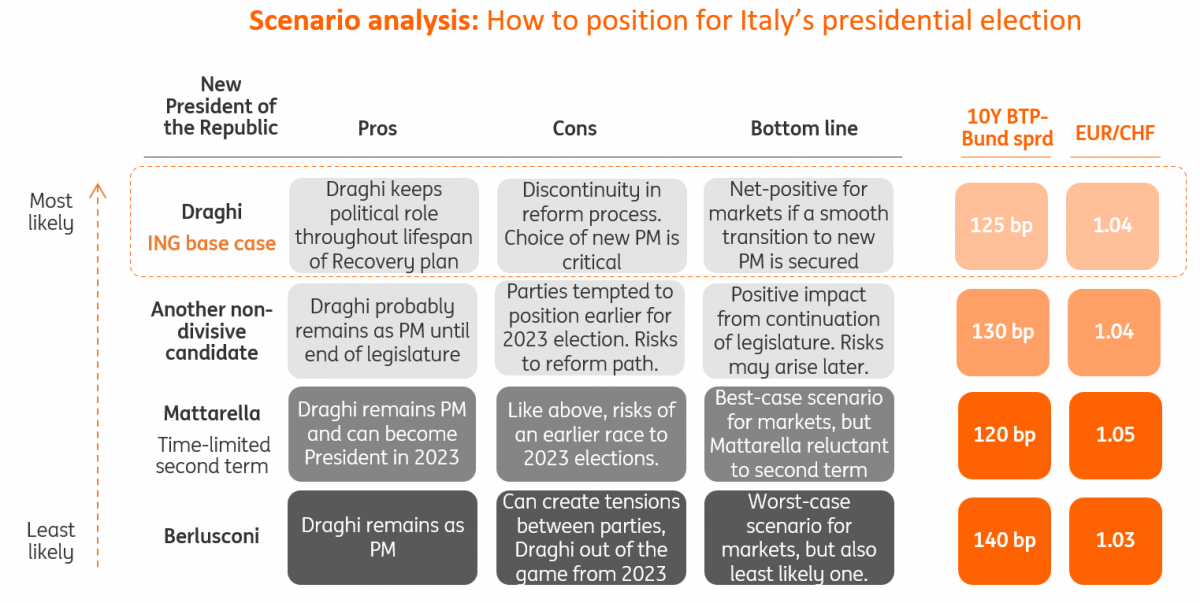

Draghi becomes president

- Pros: He would be in power for the entire duration of the Recovery and Resilience Plan (PNRR), and his credibility capital would not be dispersed. While no longer in an executive position, in his new role he could still exert his influence in the choice of relevant ministers when a new government is installed after the next national elections, due in Spring 2023.

- Cons: The implementation of the PNRR is still at an early stage. The risk of a discontinuity in the implementation process due to a change of government at a time when so many targets and milestones have to be met is real. His substitution in the prime minister role could be critical, at a time when discussions on the reform of the Stability and Growth Pact will intensify.

- Bottom line: A Draghi option would likely call for some form of legislature agreement among the current government coalition members to secure a smooth completion of the legislature and avoid substantial discontinuities in the implementation of the PNRR.

Another non-divisive candidate president

- Pros: Draghi would probably remain as prime minister until the end of the legislature, continuing his action with a special focus on the implementation of the recovery plan with limited risks of short-term setbacks.

- Cons: Knowing that Draghi would likely be ending his government experience in spring 2023 with no obvious way of interfering thereafter, the leaders of the national unity alliance could be tempted to position earlier for the race to the spring 2023 elections, with possible negative consequences on the implementation of the recovery plan.

- Bottom line: Continuation of the current legislature is likely smoother due to the lack of discontinuity in the government activity, but some form of legislature agreement among members of the current government coalition would be needed nonetheless.

Mattarella re-elected for a time-limited second term

- Pros: Draghi would remain as a prime minister until the end of the legislature, continuing his action with a special focus on the implementation of the recovery plan with limited risks of short-term setbacks. Continuity would be the name of the game, in the short run. Spring 2023 political elections would be managed by a president who already proved able to effectively supervise the formation of a new government with populistic and anti-European twists.

- Cons: As in the previous case, the risk would be that of an earlier race to the 2023 elections, with possible negative influence on the implementation of the recovery plan.

- Bottom line: Possibly the outcome which would best guarantee continuity and focus on priorities. However, on several occasions the outgoing president Sergio Mattarella signalled his unwillingness to go for a second mandate. We see this only as a choice of last resort, should all other viable alternatives fail to materialise.

Berlusconi elected

Pros: Again, Draghi would likely remain as prime minister until the end of the legislature

Cons: The choice of a divisive candidature would likely increase tensions within the governing alliance, possibly slowing down government activity. Mediation on the reform programme part of the recovery plan might prove more difficult. As in the previous case, the risk would be that of an earlier race to the 2023 elections, with possible negative influence on the implementation of the recovery plan.

Bottom line: This is the outcome with more uncertainty attached and a low probability event, in our view. The divisive nature of this choice would likely increase conflict within the government alliance, raising the risk of delays in the implementation of the recovery plan, without a strong international credibility capital to spend with partners and markets.

Italian debt: a relief, but not for long

Italian sovereign debt started the year on a strong note, considering the multitude of risks it faces. In decreasing order of importance; central bank tightening, political risk, and supply. As much as we are aiming to focus on political risk here, it is important to note the other factors when making a call on the trajectory of Italian yields.

ECB purchases are being tapered this year

If we are right in expecting Draghi to become president and that government stability will be maintained until the next parliamentary elections, his nomination would bring relief to Italian debt markets. How long that relief lasts is subject to discussion. Two questions would arise. First, how long can the current coalition be kept together? We are implicitly assuming this question away in our base case, but the soundbites from major parties in the weeks and months following Draghi’s nomination will be key for investors’ confidence. The second question is to what extent will investors be willing to buy riskier fixed-income debt when support from the European Central Bank (ECB) is withdrawn?

Draghi’s nomination would bring relief to Italian debt markets

With more than a year until the likely election date, one would forgive investors for wanting to benefit from the additional carry and roll-down offered by Italian debt compared to safer alternatives (roughly 5 basis points per quarter over 10Y Germany). Over a year, this is a non-negligible additional income to one’s portfolio. We note also that this strategy has been successful over the past two years, and so is likely to still be popular.

Investors braced for a volatile 2022 might balk at buying Italian bonds

Historically, volatility has led to limited appetite to buy riskier debt

This brings us back to ECB tapering. We attribute the success of carry-focused strategies to the ECB steamrolling yields. As purchases are tapered progressively into year-end, one wonders if assuming low rates volatility this year is wise. We doubt it. Swaption implied volatility seems to send a similar signal: investors are braced for a volatile 2022 and, historically, this has led to limited appetite to buy riskier debt. As a result, we forecast the 10Y spread with Germany to widen to 150bp in 1Q22, from just over 130bp currently. Like any other volatility-related product, predicting when spreads will spike is tricky. In our view, they will when the reality of ECB tightening dawns on investors

FX: Mostly downside risks for EUR/CHF

The ECB's massive bond buying, EU’s stimulus package and Draghi’s pledge to push forward with structural reforms have minimised risk premiums associated with Italy in the euro. The presidential elections first, and then the unwinding of ECB stimulus and general elections (in spring 2023), both bear the risk of revamping market concerns about Italian political and economic stability and its implications for the eurozone as a whole.

In FX, EUR/CHF is historically the pair that has the highest sensitivity to swings in the BTP-Bund spread, as the Swiss franc is normally the quintessential hedge to eurozone-related risks. As shown in the chart below, the correlation between the BTP-Bund spread and EUR/CHF tends to pick up whenever the spread widens significantly.

Looking at this presidential election, our base case of Draghi moving from prime minister to president of the Republic should prove to be a rather benign one for markets as investors should welcome the fact that he will still overlook the reform process (albeit from a non decision-making role) even after next year’s elections. There is, however, not much political risk currently embeded into EUR/CHF, and we therefore see some rather contained positive implications from the best-case scenario for markets.

We think, instead, that if Berlusconi becomes the new president and tensions within the ruling alliance flare up, we can definitely see some fresh pressure on EUR/CHF. Despite evidence that the SNB has scaled up FX interventions at the start of the year, we doubt there is a clear line in the sand around the current 1.04 level, and a significant rise in Italian political risk can cause EUR/CHF to explore the 1.02/1.03 range. As highlighted in this article, however, this is not our base case.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article