US: Industrial activity slow to gain traction

This morning retail sales report was fantastic, but the industrial production report highlights the fact that not every part of the economy will respond in the same way to the re-opening programs

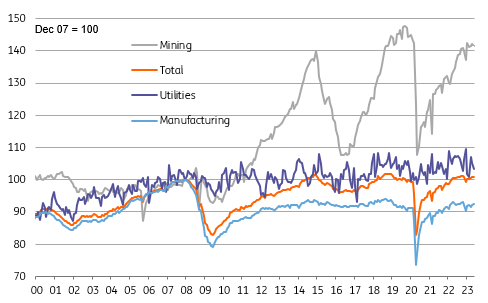

US industrial production continues to struggle despite the re-opening process getting underway across the country. Output rose just 1.4% versus expectations of a 3% increase, while April’s decline was revised to show a much steeper contraction of 12.5% versus -11.2% originally reported. This means the level of output remains 16% below the November 2019 peak and 15.4% below the pre-pandemic level in February.

Level of industrial output

While new orders remain weak, firms are also having to deal with supply chain bottlenecks due to the uneven nature of the re-opening process. As such, the manufacturing rebound of 3.8% was less than the 5% figure hoped despite strong numbers from the auto makers – output up 120.8%! Mining continues to struggle given the plunge of oil prices into negative territory earlier in the year. The Baker Hughes rig count report suggests the number of new wells being drilled is the lowest since the 1970s, implying further falls in oil and gas output in coming months. Meanwhile utilities fell 2.3%, which was weather-related and should quickly rebound.

As supply bottlenecks ease and demand gradually recovers in the re-opening phase the manufacturing sectors should strengthen further. However, we have to be aware of the risk that with capacity utilisation still down at just 64.8%, employment and investment in the sector remains vulnerable to further cuts.

Download

Download snap