UK retail sales fall as consumer confidence plunges close to record lows

It's getting increasingly difficult to see how UK consumer spending avoids a downturn over coming months, even if it's modest by historic standards. Despite repeated upside inflation surprises, we think the Bank of England is likely to tread more carefully on rate rises than markets expect

It’s not been a great morning for UK consumer news. Retail sales fell by 1.4% in March, the second consecutive monthly decline, driven largely by a sharp fall in online spending. This follows news earlier today that consumer confidence has fallen to just one point above its all-time low. Personal finance and economic expectations for the next year are about as bad as they were during the financial crisis.

All of this means it’s increasingly difficult to see consumer spending avoiding a downturn this summer, even if only modest by some historic standards. Fuel prices are up 11% since the start of the year, and household energy bills have increased by an average of 54% this month, with another 30% increase looking likely in October. Inflation is set to peak close to 9% in April and probably won’t fall below 7% this year.

The fall in March retail sales was driven by online spending

Admittedly, the cost of living squeeze probably doesn’t explain all of the recent downtrend in retail sales. We think at least some of the recent weakness is linked to consumers rediscovering services again after the Omicron wave (and the pandemic more generally). According to the monthly GDP numbers, the balance between retail and hospitality/recreation spending is now back to pre-virus levels, after a long period of above-average goods demand.

Indeed, assuming consumers remain more enthusiastic about services rather than goods spending in the near term, we suspect the impact of the cost of living shock will be more acutely felt in the retail numbers over the next few months.

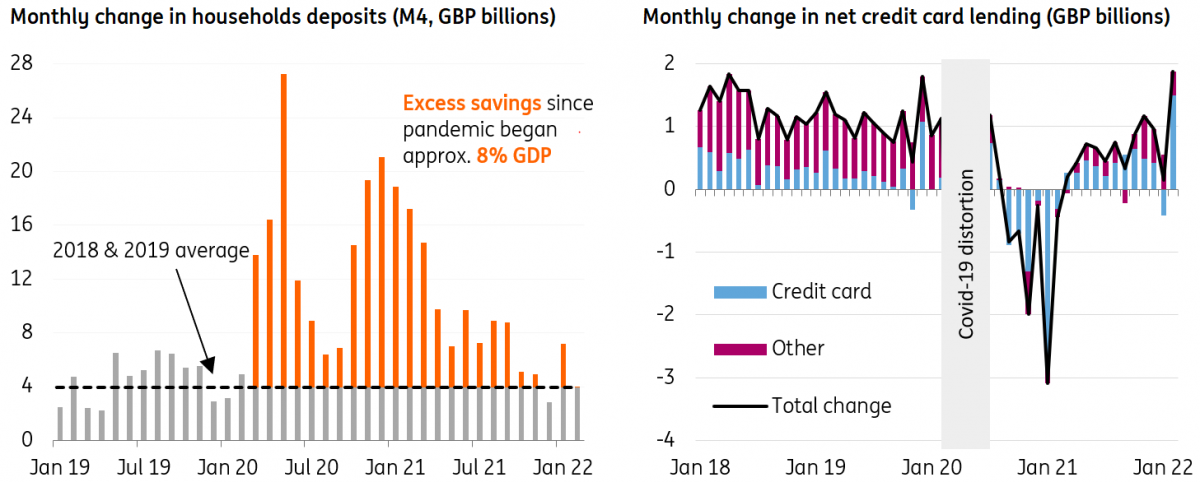

Whether the UK heads into a recession is still an open question. This crisis is unusual as around 8% of GDP worth of ‘excess’ household savings has been built up during the pandemic, though as is often highlighted, most of this is concentrated in higher-income earners who are less likely to be as hard-hit by higher energy prices. Credit card borrowing has shown – admittedly very early – signs of picking up to help cover the shortfall.

Payroll data also shows that higher income groups have seen a more noticeable acceleration in wage growth over the past two years, relative to the two years preceding the pandemic, compared to those in lower-income percentiles.

Consumers might use 'excess savings' and credit cards to offset income shock

A speech by Bank of England committee member Catherine Mann yesterday suggested that the near-term outlook for rate hikes heavily depends on whether the consumer story turns rapidly over the next few weeks, or whether any fall in spending is more gradual. In her view, a sharp deterioration in growth conditions could help to ‘short-circuit’ the ratchet higher in prices being set by companies.

The jury’s out, but we think the Bank of England is more likely to hike interest rates once or twice more, before pressing the pause button over the summer. That suggests market expectations of six more rate hikes this year are likely to be undershot.

Download

Download snap