- Opinion by Padhraic Garvey, CFA

Assessing rate cut potential for Brazil and Mexico

- 15 July 2025

- Rates Brazil Mexico

Brazil has opened a 3.5% buffer, which can expand to 5% should the Fed cut. That paves the way for 200bp of cuts, but that can be under or over shot depending on how the fiscal deficit is dealt with. Mexico can cut without the Fed, but by no more than 50bp. But that's a stretch as spreads are tight; far better for the cuts to happen under the cover of Fed cuts

Mapping out a technical rationale for setting the Banxico rate

Banco de México (Banxico) has cut its key rate from 10% to 8% so far in 2025. Yet, Mexican consumer price inflation has risen from 3.6% to 4.3% over the same period. The effect of both has cut our calculation of Banxico’s interest rate buffer to zero (see how it's calculated here). That interest rate buffer was at around 3% before Banxico kicked off its latest rate cutting sequence, and we noted at that time ample room for Banxico cuts. Following a sequence of cuts, the question is, what’s next?

Auspiciously, the cuts delivered in 2025 have coincided with material appreciation of the peso (vs US dollar). This is a tick in favour of cutting some more, as least for as long as the peso holds on to reasonable firmness. It does not have to necessarily strengthen. But it would need to show some degree of stability, or for any weakening to be moderate and contained.

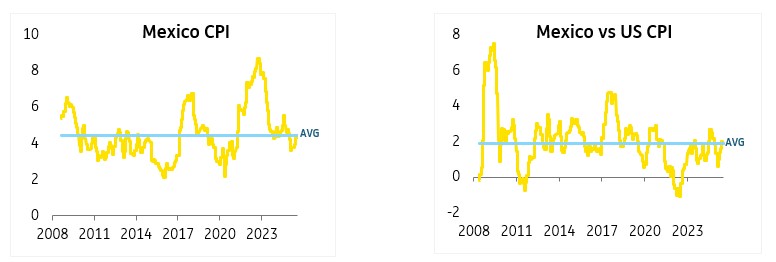

Another important ingredient is inflation, which today (at 4.3%) is pretty much bang on equal to the average Mexican inflation rate seen over the past decade and a half. It’s a little high for comfort of course, as it’s 'above 4%', but not a drama should it remain around here. And if it falls (as we expect it will), then all the better. In addition, the Mexican inflation differential to the US is also broadly flat to its 15yr average (1.9%). That at least minimises any tension that can come from this metric.

Mexican inflation is in tune with the average experience in recent times

The charts below show Mexican consumer price inflation (left) and the spread above US inflation (right). Both in (%)

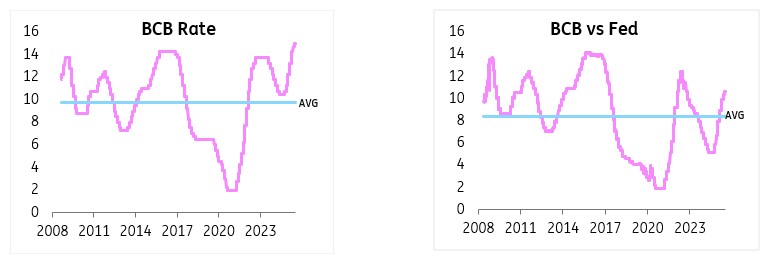

And what about the Banxico rate itself. At 8%, it’s still some 200bp above the average seen in the past 15 years (6%). That’s still optically tight, at least from a domestic perspective. However, from an international perspective, we need to acknowledge that the average Fed funds rate was just 1.3% over the same period. That’s some 200bp below what we consider to be neutral for the funds rate. When adjusted, that places the Banxico rate at 8%, at about neutral.

The Banxico differential versus the Fed funds rate is 3.7%. That’s some 100bp below the 15yr average. The all-time low was 2.9%, back in 2024 when Mexican fundamentals had been making strides towards becoming more like a developed than an emerging market. The current differential to that low is just 70bp!

So, if Banxico were to, for example, cut by another 50bp and the Fed were to remain on hold, that spread would be practically back to its historical tights.

Banxico has room to cut from a domestic perspective, but has very little from an international one

The charts below show the Banxico rate (left) and the spread above the Fed funds rate (right). Both in (%)

So what does all this mean for the Banxico rate?

It seems to us that Banxico is at a bottom right now for rates, and really needs the Fed to cut rates in order for room to open up for similar from Banxico. At a maximum, Banxico can deliver another 50bp cut without the Fed, but that is then down to the bare bone. Realistically, the Fed would need to deliver some 100bp of cuts to provide Banxico with the required degree of comfort, facilitating an end game for Banxico at 7.5%. And we still think the ultimate low if all stars align would be c.7%. Getting down there would require the Fed getting lower still.

Mapping out a technical rationale for setting the BCB rate

For Brazil, inflation is a tad elevated at 5.4% currently. However, that’s actually below the 15yr average inflation. Also, the inflation differential to the US is a tad lower than average (by about 30bp). So while objectively it would be better to have Brazilian inflation lower (and it likely does ease lower), this metric, in itself, does not require an elevated Banco Central do Brasil (BCB) official rate. But it’s still important when it comes to relative value metrics.

Brazilian inflation is in tune with the average experience in recent times

The charts below show Brazil consumer price inflation (left) and the spread above US inflation (right). Both in (%)

The fiscal metrics in Brazil, and the political unwillingness to address them remain the most troubling issue. That said, the crescendo in terms of market impact was over the turn of the year when the real broke towards and above 6 vs the US dollar, necessitating a reversion to a rate hiking process from 10.5% to 15%. The question is now what?

At 15%, the BCB rate is at its highest since the early 2000’s. History shows it has been far higher, but still, it’s high today, and 5% above the 15yr average. Versus the Fed funds rate, the BCB rate is not as stretched. It’s currently at a little over 2% above the 15yr average (8.5%). Our overall calculation of the rate buffer to neutrality is now at 3.5%. That’s the buffer that BCB has built through rate hikes.

For the BCB rate, there's a 5% spread on the domestic average and a 2% spread on the spread to funds rate average

The charts below show the BCB rate (left) and the spread above the Fed funds rate (right). Both in (%)

A buffer like that is typically built through periods of macro vulnerability and / or currency instability. That said, when its deemed high enough, it then morphs to act as a protective factor. It seems that’s where we are now. This acts as a support for the Brazilian real for example, which indeed has been back below 6 since April.

So what does all this mean for the BCB rate?

The 5.5 area is where BRL/USD needs to track at for the BCB to cut rates, and we’d need a run of time in that area, and ideally the beginning of a Fed cutting phase to allow room for BCB cuts. If the Fed were to cut by 125bp and Brazilian inflation falls to 4.5%, then the 3.5% buffer gets close to 5%. That would mean that there could be some 200bp of cuts from BCB, while maintaining a residual 3% buffer (bad fiscal noise protection). That’s doable as a 2026 outcome. But it does in part depend on the fiscal noise quietening some more. In the end that will determine whether BCB cuts by more or less than the 200bp suggested, and by how much.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more