Bundles29 March 2018

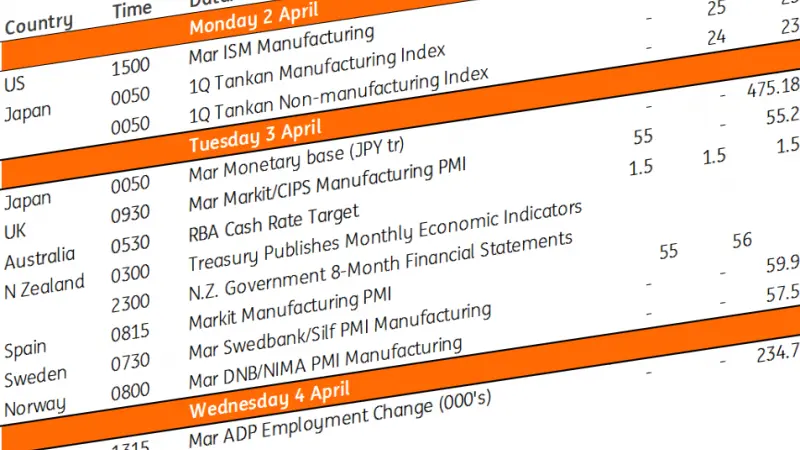

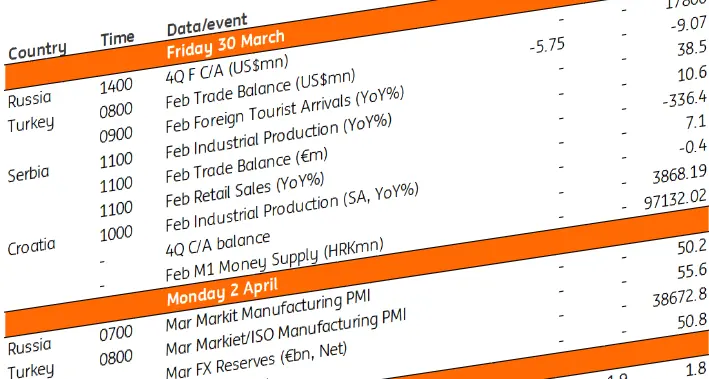

Our view on next week’s key events

Discover what ING analysts are looking for next week in our global economic calendars

Our view on next week’s key events

Discover what ING analysts are looking for next week in our global economic calendars